Question: 6. Discuss whose optimal portfolio performs better (John or Mary), and explain why. Also discuss potential reason(s) that causes the difference. (A half to one

6. Discuss whose optimal portfolio performs better (John or Mary), and explain why. Also discuss potential reason(s) that causes the difference. (A half to one page discussion, double space)

6. Discuss whose optimal portfolio performs better (John or Mary), and explain why. Also discuss potential reason(s) that causes the difference. (A half to one page discussion, double space)

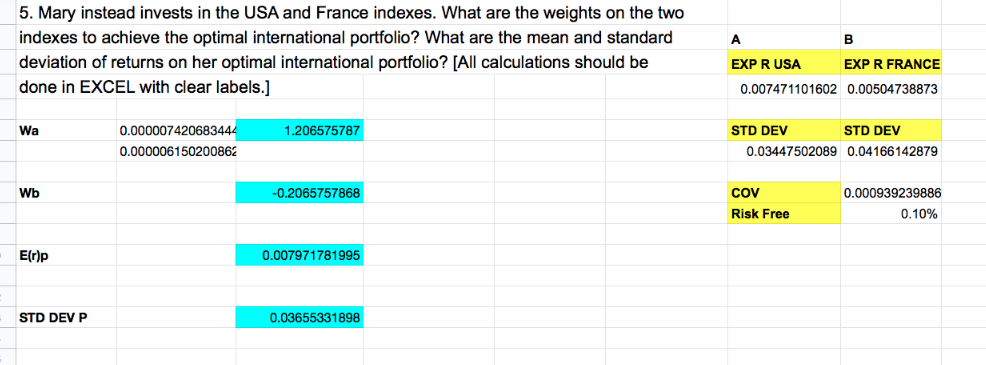

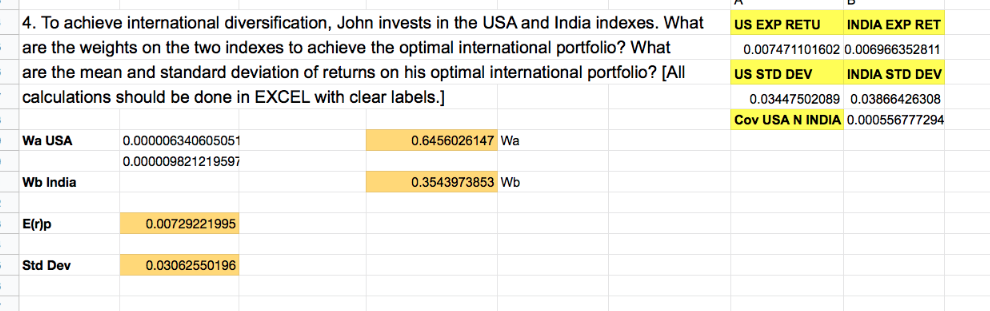

5. Mary instead invests in the USA and France indexes. What are the weights on the two indexes to achieve the optimal international portfolio? What are the mean and standard deviation of returns on her optimal international portfolio? [All calculations should be done in EXCEL with clear labels.] EXP R USA EXP R FRANCE 0.007471101602 0.00504738873 Wa 1.206575787 0.00000742068344 0.000006150200862 STD DEV STD DEV 0.03447502089 0.04166142879 Wb -0.2065757868 COV 0.000939239886 0.10% Risk Free Erp 0.007971781995 STD DEVP 0.03655331898 4. To achieve international diversification, John invests in the USA and India indexes. What are the weights on the two indexes to achieve the optimal international portfolio? What are the mean and standard deviation of returns on his optimal international portfolio? [All calculations should be done in EXCEL with clear labels.] US EXP RETU INDIA EXP RET 0.007471101602 0.006966352811 US STD DEV INDIA STD DEV 0.03447502089 0.03866426308 Cov USA N INDIA 0.000556777294 Wa USA 0.6456026147 Wa 0.000006340605051 0.000009821219597 Wb India 0.3543973853 Wb E()p 0.00729221995 Std Dev 0.03062550196

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts