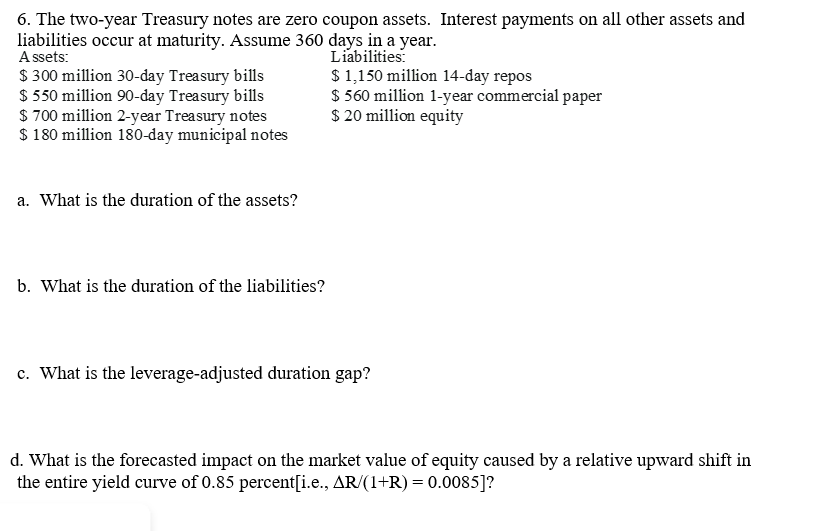

Question: 6. The two-year Treasury notes are zero coupon assets. Interest payments on all other assets and liabilities occur at maturity. Assume 360 days in a

6. The two-year Treasury notes are zero coupon assets. Interest payments on all other assets and liabilities occur at maturity. Assume 360 days in a year. a. What is the duration of the assets? b. What is the duration of the liabilities? c. What is the leverage-adjusted duration gap? d. What is the forecasted impact on the market value of equity caused by a relative upward shift in the entire yield curve of 0.85 percent[i.e., R/(1+R)=0.0085] ? 6. The two-year Treasury notes are zero coupon assets. Interest payments on all other assets and liabilities occur at maturity. Assume 360 days in a year. a. What is the duration of the assets? b. What is the duration of the liabilities? c. What is the leverage-adjusted duration gap? d. What is the forecasted impact on the market value of equity caused by a relative upward shift in the entire yield curve of 0.85 percent[i.e., R/(1+R)=0.0085]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts