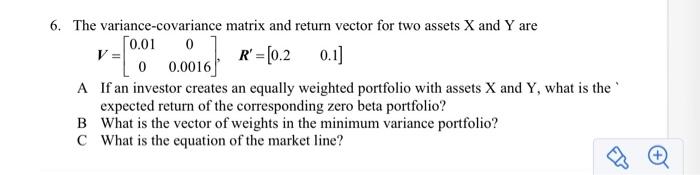

Question: 6. The variance-covariance matrix and return vector for two assets X and Y are [0.01 0 V = R' = [0.2 0.1] 0 0.0016] A

6. The variance-covariance matrix and return vector for two assets X and Y are [0.01 0 V = R' = [0.2 0.1] 0 0.0016] A If an investor creates an equally weighted portfolio with assets X and Y, what is the expected return of the corresponding zero beta portfolio? B What is the vector of weights in the minimum variance portfolio? C What is the equation of the market line

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock