Question: 6. Using interest rate swaps to reduce interest rate risk Suppose that Phoenix bank seeks to reduce its interest rate risk in regards to its

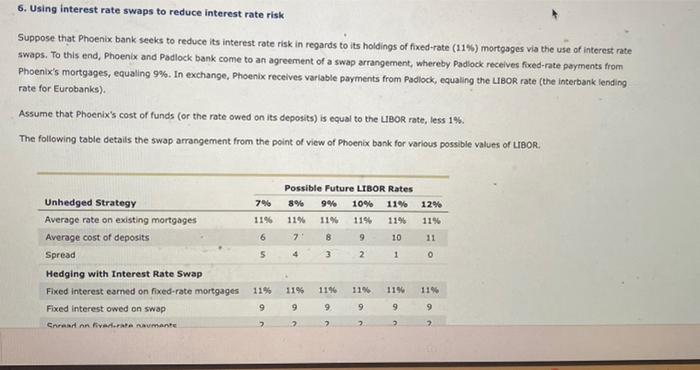

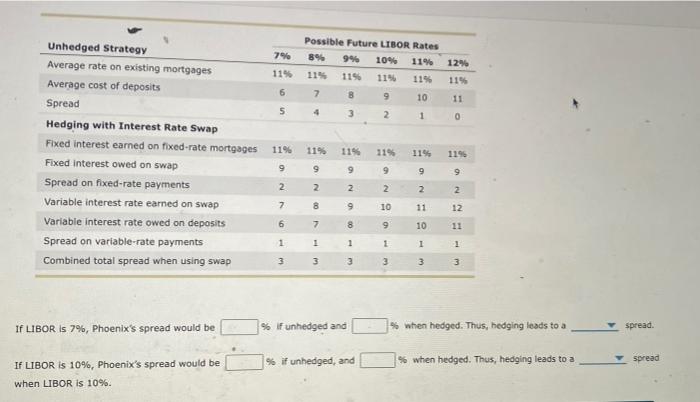

6. Using interest rate swaps to reduce interest rate risk Suppose that Phoenix bank seeks to reduce its interest rate risk in regards to its holdings of fixed-rate (11\%) mortgages via the use of interest rate swaps. To this end, Phoenix and Padlock bank come to an agreement of a swap arrangement, whereby Padiock recelves fixed-rate payments from Phoenix's mortgages, equaling 9%. In exchange, Phoenix receives varlable payments from Padlock, equaling the UBOR rate (the interbank lending rate for Eurobanks). Assume that Phoenix's cost of funds (or the rate owed on its deposits) is equal to the UBOR rate, less 1%. The following toble details the swap arrangement from the point of view of Phoenix bank for various possible values of LBOR. If LIBOR is 7%, Phoenix's spread would be \%h if unhedged and \% when hedged. Thus, hedging lesds to a spread. If LIBOR is 10%, Phoenix's spread would be % if unhedged, and %6 when hedged. Thus, hedging leads to a spread when LIBOR is 10%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts