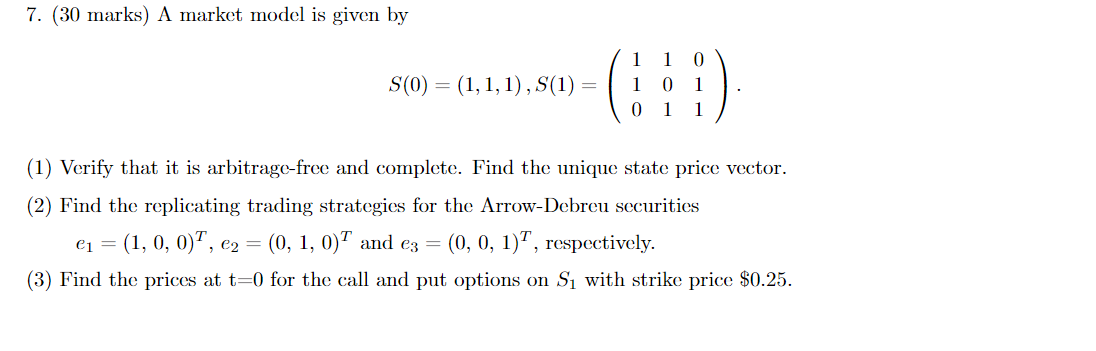

Question: 7. (30 marks) A market model is given by S(0) = (1,1,1), S(1) = 1 1 0 1 0 1 0 1 1 (1) Verify

7. (30 marks) A market model is given by S(0) = (1,1,1), S(1) = 1 1 0 1 0 1 0 1 1 (1) Verify that it is arbitrage-free and complete. Find the unique state price vector. (2) Find the replicating trading strategies for the Arrow-Debreu securities C1 = (1, 0, 0)*, C2 = (0, 1, 0)T and c3 = (0, 0, 1)", respectively. (3) Find the prices at t=0 for the call and put options on Sy with strike price $0.25. 7. (30 marks) A market model is given by S(0) = (1,1,1), S(1) = 1 1 0 1 0 1 0 1 1 (1) Verify that it is arbitrage-free and complete. Find the unique state price vector. (2) Find the replicating trading strategies for the Arrow-Debreu securities C1 = (1, 0, 0)*, C2 = (0, 1, 0)T and c3 = (0, 0, 1)", respectively. (3) Find the prices at t=0 for the call and put options on Sy with strike price $0.25

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts