Question: 7) Consider the following Matlab outputs. Summarize the model, write its equation(s) and comment on the model: AR-Stationary 2-Dimensional VAR(1) Model Effective Sample Size:

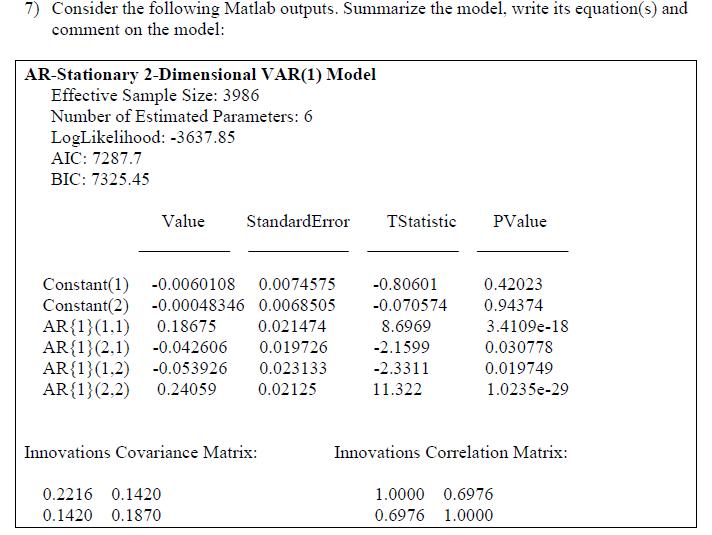

7) Consider the following Matlab outputs. Summarize the model, write its equation(s) and comment on the model: AR-Stationary 2-Dimensional VAR(1) Model Effective Sample Size: 3986 Number of Estimated Parameters: 6 LogLikelihood: -3637.85 AIC: 7287.7 BIC: 7325.45 Value StandardError TStatistic Constant(1) -0.0060108 0.0074575 -0.80601 Constant(2) -0.00048346 0.0068505 -0.070574 8.6969 -2.1599 -2.3311 11.322 AR{1}(1,1) 0.18675 0.021474 AR{1}(2.1) -0.042606 0.019726 AR{1}(1.2) -0.053926 0.023133 AR{1}(2.2) 0.24059 0.02125 Innovations Covariance Matrix: 0.2216 0.1420 0.1420 0.1870 PValue 0.42023 0.94374 3.4109e-18 0.030778 0.019749 1.0235e-29 Innovations Correlation Matrix: 1.0000 0.6976 0.6976 1.0000

Step by Step Solution

3.49 Rating (162 Votes )

There are 3 Steps involved in it

This is an ARStationary 2Dimensional VAR1 Model which means that it is a vector autoregression model ... View full answer

Get step-by-step solutions from verified subject matter experts