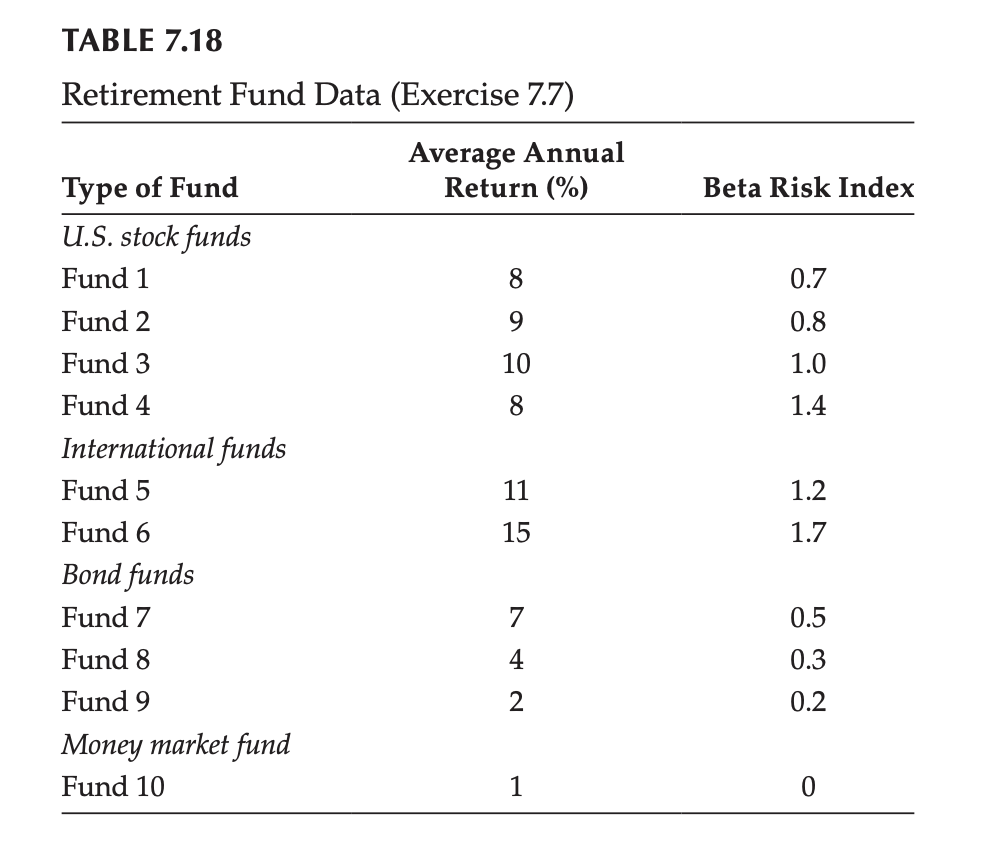

Question: 7.7 Jill is interested in determining her asset allocation for her 401-K retirement plan. Her company has 10 mutual funds for investment. Their past performance

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock