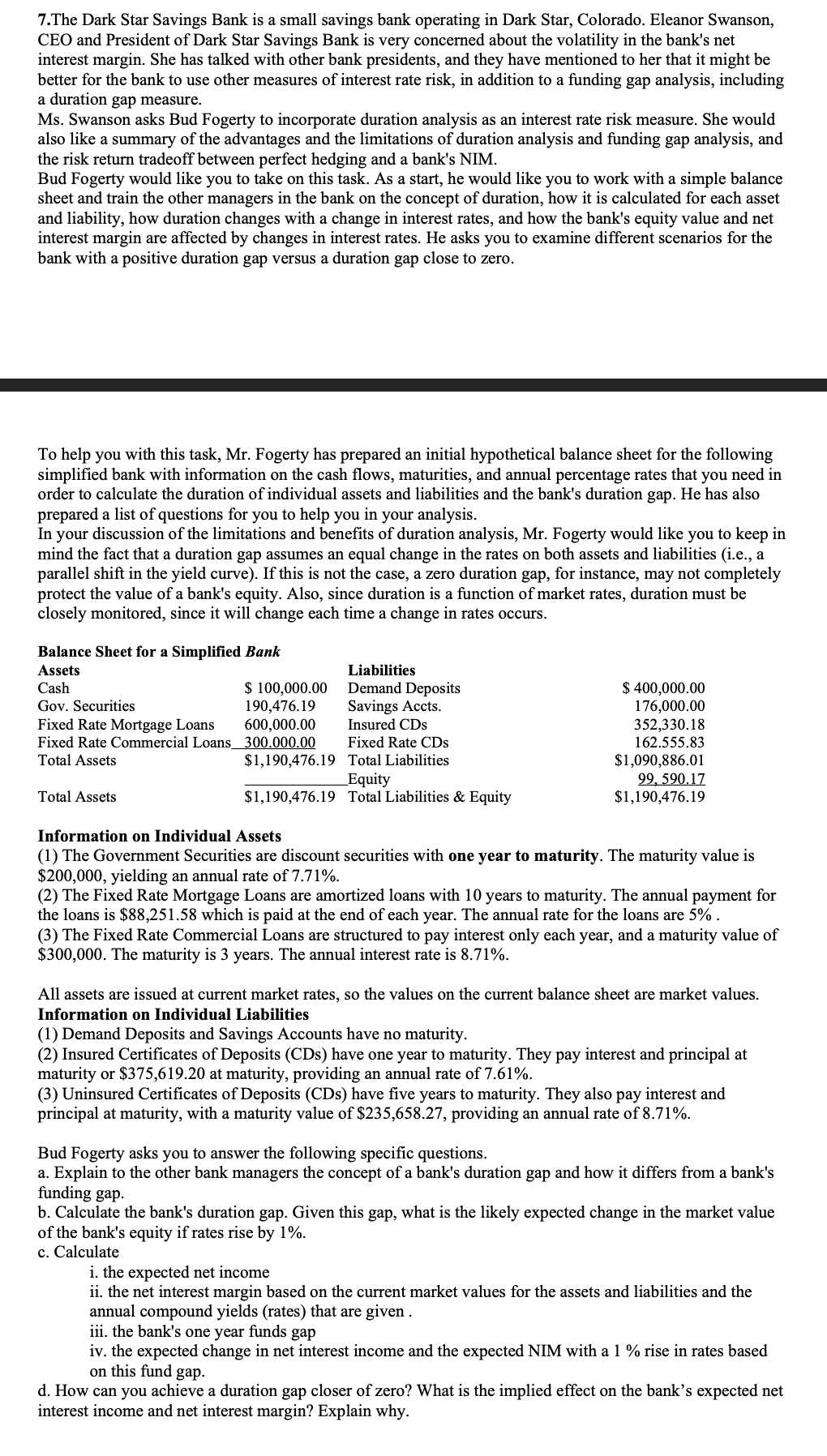

7.The Dark Star Savings Bank is a small savings bank operating in Dark Star, Colorado. Eleanor...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

7.The Dark Star Savings Bank is a small savings bank operating in Dark Star, Colorado. Eleanor Swanson, CEO and President of Dark Star Savings Bank is very concerned about the volatility in the bank's net interest margin. She has talked with other bank presidents, and they have mentioned to her that it might be better for the bank to use other measures of interest rate risk, in addition to a funding gap analysis, including a duration gap measure. Ms. Swanson asks Bud Fogerty to incorporate duration analysis as an interest rate risk measure. She would also like a summary of the advantages and the limitations of duration analysis and funding gap analysis, and the risk return tradeoff between perfect hedging and a bank's NIM. Bud Fogerty would like you to take on this task. As a start, he would like you to work with a simple balance sheet and train the other managers in the bank on the concept of duration, how it is calculated for each asset and liability, how duration changes with a change in interest rates, and how the bank's equity value and net interest margin are affected by changes in interest rates. He asks you to examine different scenarios for the bank with a positive duration gap versus a duration gap close to zero. To help you with this task, Mr. Fogerty has prepared an initial hypothetical balance sheet for the following simplified bank with information on the cash flows, maturities, and annual percentage rates that you need in order to calculate the duration of individual assets and liabilities and the bank's duration gap. He has also prepared a list of questions for you to help you in your analysis. In your discussion of the limitations and benefits of duration analysis, Mr. Fogerty would like you to keep in mind the fact that a duration gap assumes an equal change in the rates on both assets and liabilities (i.e., a parallel shift in the yield curve). If this is not the case, a zero duration gap, for instance, may not completely protect the value of a bank's equity. Also, since duration is a function of market rates, duration must be closely monitored, since it will change each time a change in rates occurs. Balance Sheet for a Simplified Bank Assets Cash Gov. Securities $ 100,000.00 190,476.19 Fixed Rate Mortgage Loans 600,000.00 Liabilities Demand Deposits Savings Accts. Insured CDs Fixed Rate Commercial Loans 300.000.00 Fixed Rate CDs Total Assets $1,190,476.19 Total Liabilities Equity Total Assets $1,190,476.19 Total Liabilities & Equity Information on Individual Assets $ 400,000.00 176,000.00 352,330.18 162.555.83 $1,090,886.01 99,590.17 $1,190,476.19 (1) The Government Securities are discount securities with one year to maturity. The maturity value is $200,000, yielding an annual rate of 7.71%. (2) The Fixed Rate Mortgage Loans are amortized loans with 10 years to maturity. The annual payment for the loans is $88,251.58 which is paid at the end of each year. The annual rate for the loans are 5%. (3) The Fixed Rate Commercial Loans are structured to pay interest only each year, and a maturity value of $300,000. The maturity is 3 years. The annual interest rate is 8.71%. All assets are issued at current market rates, so the values on the current balance sheet are market values. Information on Individual Liabilities (1) Demand Deposits and Savings Accounts have no maturity. (2) Insured Certificates of Deposits (CDs) have one year to maturity. They pay interest and principal at maturity or $375,619.20 at maturity, providing an annual rate of 7.61%. (3) Uninsured Certificates of Deposits (CDs) have five years to maturity. They also pay interest and principal at maturity, with a maturity value of $235,658.27, providing an annual rate of 8.71%. Bud Fogerty asks you to answer the following specific questions. a. Explain to the other bank managers the concept of a bank's duration gap and how it differs from a bank's funding gap. b. Calculate the bank's duration gap. Given this gap, what is the likely expected change in the market value of the bank's equity if rates rise by 1%. c. Calculate i. the expected net income ii. the net interest margin based on the current market values for the assets and liabilities and the annual compound yields (rates) that are given. iii. the bank's one year funds gap iv. the expected change in net interest income and the expected NIM with a 1% rise in rates based on this fund gap. d. How can you achieve a duration gap closer of zero? What is the implied effect on the bank's expected net interest income and net interest margin? Explain why. 7.The Dark Star Savings Bank is a small savings bank operating in Dark Star, Colorado. Eleanor Swanson, CEO and President of Dark Star Savings Bank is very concerned about the volatility in the bank's net interest margin. She has talked with other bank presidents, and they have mentioned to her that it might be better for the bank to use other measures of interest rate risk, in addition to a funding gap analysis, including a duration gap measure. Ms. Swanson asks Bud Fogerty to incorporate duration analysis as an interest rate risk measure. She would also like a summary of the advantages and the limitations of duration analysis and funding gap analysis, and the risk return tradeoff between perfect hedging and a bank's NIM. Bud Fogerty would like you to take on this task. As a start, he would like you to work with a simple balance sheet and train the other managers in the bank on the concept of duration, how it is calculated for each asset and liability, how duration changes with a change in interest rates, and how the bank's equity value and net interest margin are affected by changes in interest rates. He asks you to examine different scenarios for the bank with a positive duration gap versus a duration gap close to zero. To help you with this task, Mr. Fogerty has prepared an initial hypothetical balance sheet for the following simplified bank with information on the cash flows, maturities, and annual percentage rates that you need in order to calculate the duration of individual assets and liabilities and the bank's duration gap. He has also prepared a list of questions for you to help you in your analysis. In your discussion of the limitations and benefits of duration analysis, Mr. Fogerty would like you to keep in mind the fact that a duration gap assumes an equal change in the rates on both assets and liabilities (i.e., a parallel shift in the yield curve). If this is not the case, a zero duration gap, for instance, may not completely protect the value of a bank's equity. Also, since duration is a function of market rates, duration must be closely monitored, since it will change each time a change in rates occurs. Balance Sheet for a Simplified Bank Assets Cash Gov. Securities $ 100,000.00 190,476.19 Fixed Rate Mortgage Loans 600,000.00 Liabilities Demand Deposits Savings Accts. Insured CDs Fixed Rate Commercial Loans 300.000.00 Fixed Rate CDs Total Assets $1,190,476.19 Total Liabilities Equity Total Assets $1,190,476.19 Total Liabilities & Equity Information on Individual Assets $ 400,000.00 176,000.00 352,330.18 162.555.83 $1,090,886.01 99,590.17 $1,190,476.19 (1) The Government Securities are discount securities with one year to maturity. The maturity value is $200,000, yielding an annual rate of 7.71%. (2) The Fixed Rate Mortgage Loans are amortized loans with 10 years to maturity. The annual payment for the loans is $88,251.58 which is paid at the end of each year. The annual rate for the loans are 5%. (3) The Fixed Rate Commercial Loans are structured to pay interest only each year, and a maturity value of $300,000. The maturity is 3 years. The annual interest rate is 8.71%. All assets are issued at current market rates, so the values on the current balance sheet are market values. Information on Individual Liabilities (1) Demand Deposits and Savings Accounts have no maturity. (2) Insured Certificates of Deposits (CDs) have one year to maturity. They pay interest and principal at maturity or $375,619.20 at maturity, providing an annual rate of 7.61%. (3) Uninsured Certificates of Deposits (CDs) have five years to maturity. They also pay interest and principal at maturity, with a maturity value of $235,658.27, providing an annual rate of 8.71%. Bud Fogerty asks you to answer the following specific questions. a. Explain to the other bank managers the concept of a bank's duration gap and how it differs from a bank's funding gap. b. Calculate the bank's duration gap. Given this gap, what is the likely expected change in the market value of the bank's equity if rates rise by 1%. c. Calculate i. the expected net income ii. the net interest margin based on the current market values for the assets and liabilities and the annual compound yields (rates) that are given. iii. the bank's one year funds gap iv. the expected change in net interest income and the expected NIM with a 1% rise in rates based on this fund gap. d. How can you achieve a duration gap closer of zero? What is the implied effect on the bank's expected net interest income and net interest margin? Explain why.

Expert Answer:

Related Book For

Accounting for Decision Making and Control

ISBN: 978-1259564550

9th edition

Authors: Jerold Zimmerman

Posted Date:

Students also viewed these finance questions

-

An analysis of the Halperts' savings for Cece's future education goal. You will also need to refer to the FP Canada Guidelines 2023. For any TVM calculations, show work in the format of N=, I/Y=,...

-

It is July 1, 2023, Jim and Pam Halpert have just left your office after their first interview with you. In preparation for the interview, you had sent them a list of the various documents that they...

-

A problem in Statistics is given to three students A, B, and C whose chances of solving it are 1/4 and 1/5 respectively. Find the probability that the problem will be solved if they all try...

-

If the number of leftmost ones is less than the number of variables and the system is consistent, then the system has infinitely many solutions.

-

Two years ago you sold a call option on stock ZYX, with a strike price of $30, which expires today. At that time you also bought a share of stock ZYX. Today the share price of ZYX is $34. What is the...

-

What is the role of domain analysis in designing a product?

-

Refer to the North Valley Real Estate data and prepare a report on the sales prices of the homes. Be sure to answer the following questions in your report. a. Around what values of price do the data...

-

Joe and Sophie, a fictional couple, are undergoing a divorce. The parties have been married for ten ( 1 0 ) years. They have accumulated assets during their marriage and now they are seeking a fair...

-

Explain the process of preparing a bank reconciliation statement and its importance in financial accounting. How do discrepancies between the cash book and bank statement get resolved?

-

Which of the following statements about a 3-for-1 share split is true? a. It will triple the market price of the share. b. It will triple the amount of total equity. c. It will have no effect on...

-

The return on ordinary shareholders equity is defined as: a. net income divided by total assets. b. cash dividends divided by average ordinary shareholders equity. c. income available to ordinary...

-

The ledger of JFK, plc shows share capitalordinary, treasury sharesordinary, and no preference shares. For this company, the formula for computing book value per share is: a. total equity divided by...

-

Raptor NV has retained earnings of 500,000 and total equity of 2,000,000. It has 100,000 shares of 8 par value ordinary shares outstanding, which is currently selling for 30 per share. If Raptor...

-

In the equity section, Ordinary Share Dividends Distributable is reported as a(n): a. deduction from share capital and retained earnings. b. addition to share premium. c. deduction from retained...

-

What is the discount rate for a stock whose beta is 1.5. Currently, the expected market return is 10%, and the risk-free rate is 3%.

-

Smiths Family Fashions implemented a balanced scorecard performance measurement system several years ago. Smiths is a locally owned clothing retailer with fashions for men, women, teens, and...

-

What is the formula to calculate an individuals taxable income?

-

Explain why a taxpayer with higher income does not have as large of a behavioral response to an increase in the tax rate as a lower-income taxpayer.

-

Describe the goal of tax planning.

Study smarter with the SolutionInn App