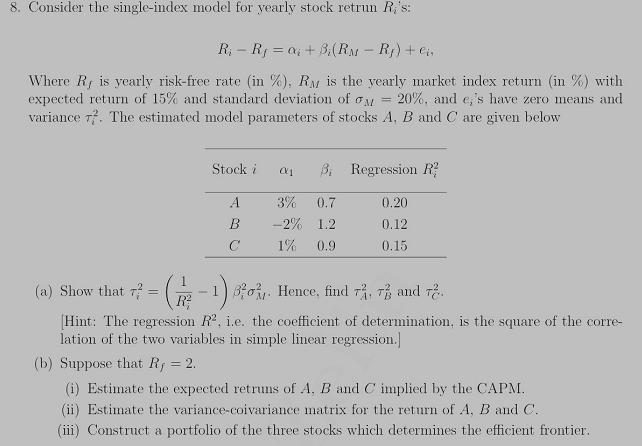

Question: 8. Consider the single-index model for yearly stock retrun Ri's: R; - Rj = 0; + 3:(RM - Rj) + eis Where R, is yearly

8. Consider the single-index model for yearly stock retrun Ri's: R; - Rj = 0; + 3:(RM - Rj) + eis Where R, is yearly risk-free rate (in %), RN is the vearly market index return (in %) with expected return of 15% and standard deviation of on = 20%, and e;'s have zero means and variance T. The estimated model parameters of stocks A, B and C are given below Stock i 01 B: Regression R B 3% 0.7 -2% 1.2 1% 0.9 0.20 0.12 0.15 T Hint: The regression R, i.e. the coefficient of determination, is the square of the corre- lation of the two variables in simple linear regression.) (b) Suppose that R, = 2. (i) Estimate the expected retruns of A, B and C implied by the CAPM. (ii) Estimate the variance-coivariance matrix for the return of A, B and C. (iii) Construct a portfolio of the three stocks which determines the efficient frontier. 8. Consider the single-index model for yearly stock retrun Ri's: R; - Rj = 0; + 3:(RM - Rj) + eis Where R, is yearly risk-free rate (in %), RN is the vearly market index return (in %) with expected return of 15% and standard deviation of on = 20%, and e;'s have zero means and variance T. The estimated model parameters of stocks A, B and C are given below Stock i 01 B: Regression R B 3% 0.7 -2% 1.2 1% 0.9 0.20 0.12 0.15 T Hint: The regression R, i.e. the coefficient of determination, is the square of the corre- lation of the two variables in simple linear regression.) (b) Suppose that R, = 2. (i) Estimate the expected retruns of A, B and C implied by the CAPM. (ii) Estimate the variance-coivariance matrix for the return of A, B and C. (iii) Construct a portfolio of the three stocks which determines the efficient frontier

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts