Question: 8 pts Consider a CDO with $100 million in collateral assets yielding a fixed rate of T plus 150 bps. The CDO is structured as

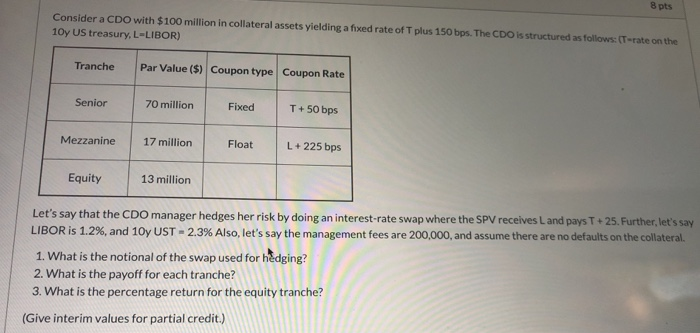

8 pts Consider a CDO with $100 million in collateral assets yielding a fixed rate of T plus 150 bps. The CDO is structured as follows: (T-rate on the 10y US treasury, L-LIBOR) Tranche Par Value ($) Coupon type Coupon Rate Senior 70 million Fixed T + 50 bps Mezzanine 17 million Float L+225 bps Equity 13 million Let's say that the CDO manager hedges her risk by doing an interest-rate swap where the SPV receives L and pays T + 25. Further, let's say LIBOR is 1.2%, and 10y UST - 2.3% Also, let's say the management fees are 200,000, and assume there are no defaults on the collateral. 1. What is the notional of the swap used for hedging? 2. What is the payoff for each tranche? 3. What is the percentage return for the equity tranche? (Give interim values for partial credit.) 8 pts Consider a CDO with $100 million in collateral assets yielding a fixed rate of T plus 150 bps. The CDO is structured as follows: (T-rate on the 10y US treasury, L-LIBOR) Tranche Par Value ($) Coupon type Coupon Rate Senior 70 million Fixed T + 50 bps Mezzanine 17 million Float L+225 bps Equity 13 million Let's say that the CDO manager hedges her risk by doing an interest-rate swap where the SPV receives L and pays T + 25. Further, let's say LIBOR is 1.2%, and 10y UST - 2.3% Also, let's say the management fees are 200,000, and assume there are no defaults on the collateral. 1. What is the notional of the swap used for hedging? 2. What is the payoff for each tranche? 3. What is the percentage return for the equity tranche? (Give interim values for partial credit.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts