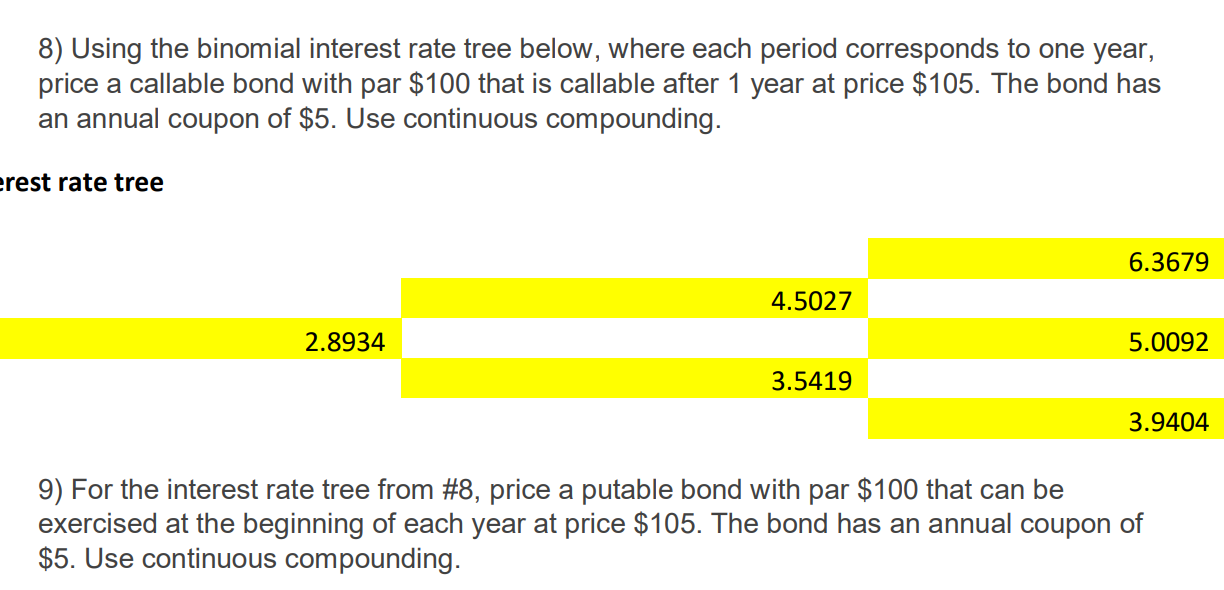

Question: 8) Using the binomial interest rate tree below, where each period corresponds to one year, price a callable bond with par $100 that is callable

8) Using the binomial interest rate tree below, where each period corresponds to one year, price a callable bond with par $100 that is callable after 1 year at price $105. The bond has an annual coupon of $5. Use continuous compounding. erest rate tree 6.3679 4.5027 2.8934 5.0092 3.5419 3.9404 9) For the interest rate tree from #8, price a putable bond with par $100 that can be exercised at the beginning of each year at price $105. The bond has an annual coupon of $5. Use continuous compounding. 8) Using the binomial interest rate tree below, where each period corresponds to one year, price a callable bond with par $100 that is callable after 1 year at price $105. The bond has an annual coupon of $5. Use continuous compounding. erest rate tree 6.3679 4.5027 2.8934 5.0092 3.5419 3.9404 9) For the interest rate tree from #8, price a putable bond with par $100 that can be exercised at the beginning of each year at price $105. The bond has an annual coupon of $5. Use continuous compounding

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts