a. An investor buys a European put option on a share for 3. The current stock price

Question:

a. An investor buys a European put option on a share for £3. The current stock price is £21 and the strike price is £18. The maturity of the option is in 3 months. Briefly discuss the investor’s motivation for purchasing the put option. Draw a diagram showing the investor’s potential profit/loss on this position at maturity. [5 marks]

b. An investor writes a European call option on a share for £1. The current stock price is £11 and the strike price is £12. The maturity of the option is in 3 months. Briefly discuss the investor’s motivation for selling the call option and highlight the key challenge of this position. Draw a diagram showing the investor’s potential profit/loss on this position at the maturity. [5 marks]

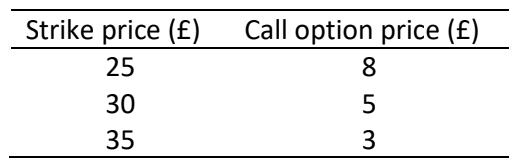

c. A butterfly spread involves positions in four options of the same option type on the same underlying security, all with the same expiry date but with three different strike prices. An investor has created a butterfly spread by buying one European call option with a £25 strike price, buying one European call option with a £35 strike price, and writing (selling) two European call options with a £30 strike price. Suppose that the market prices of the options are as follows:

REQUIRED:

i. Draw a diagram for the investor’s net profit/loss from creating the butterfly spread. (Mark the strike prices, the lower bound and the upper bound on the net profit/loss if possible.).

ii. Briefly discuss the investor’s motivation for building the butterfly spread.

d. Discuss “Time to Expiry” as one of the key factors that influences European option prices

e. Briefly discuss the key differences between forwards and futures.

f. Suppose the risk-free rate is 6% per annum and the dividend yield on a stock index over the next three months is 1.5% per annum. All interest rates and dividend yields are continuously compounded. If the index is trading at 1,000 and the 9-month stock index future contract is currently trading at 1,020, is there any mis-pricing? If so, how can investors exploit the mispricing?

Expert Answer:

Financial Statement Analysis

ISBN: 978-0078110962

11th edition

Authors: K. R. Subramanyam, John Wild