Question: 9) Consider a multifactor APT. There are two independent economic factors, F and F2. The risk-free rate of return is 2%. The following information is

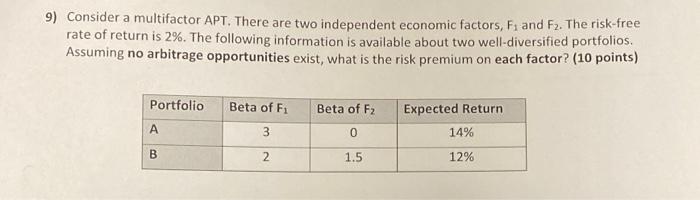

9) Consider a multifactor APT. There are two independent economic factors, F and F2. The risk-free rate of return is 2%. The following information is available about two well-diversified portfolios. Assuming no arbitrage opportunities exist, what is the risk premium on each factor? (10 points) Portfolio Beta of F1 Beta of F2 Expected Return 14% A 3 0 B 2 1.5 12%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock