Question: (a) (b) Applying FRS 102 Share-based Payments, prepare the journal entries to record the transactions from 1 January 20x1 to 31 December 20x4. Narrations are

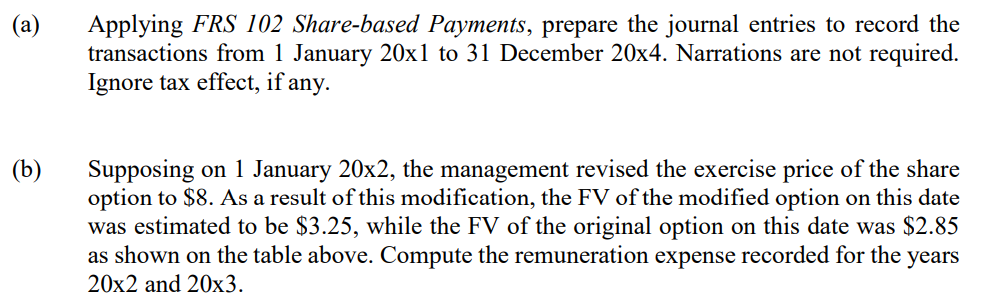

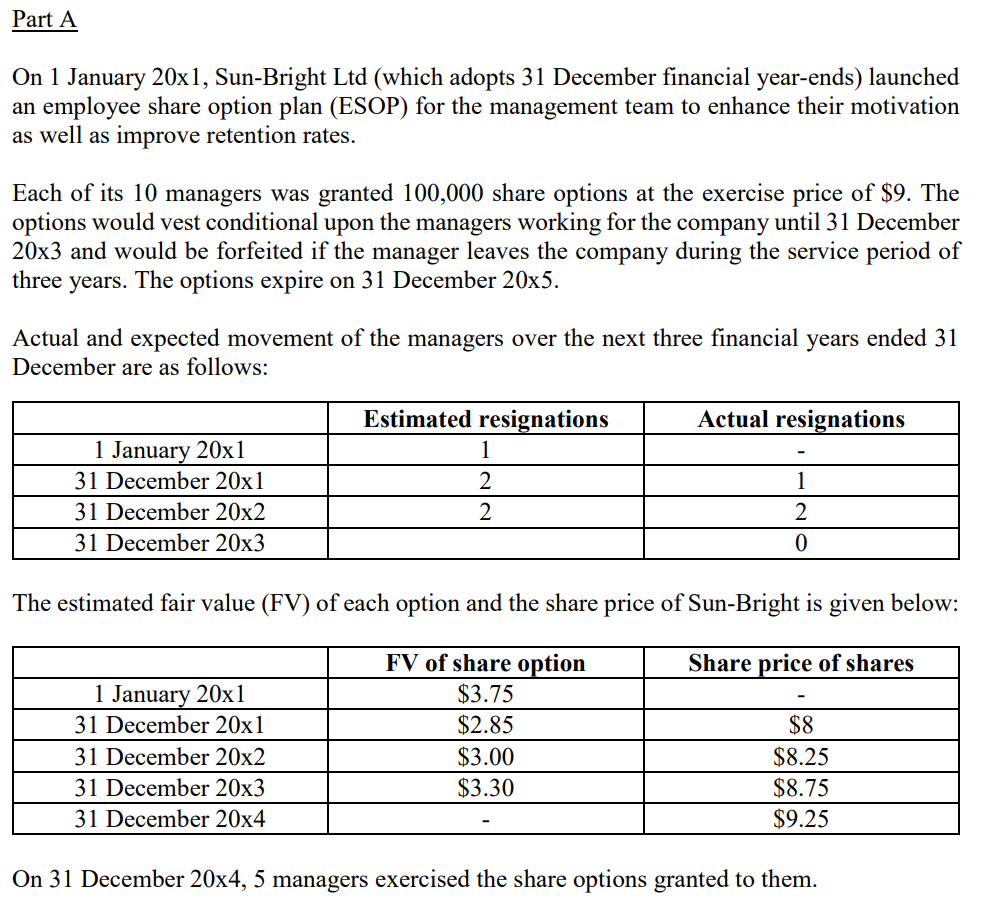

(a) (b) Applying FRS 102 Share-based Payments, prepare the journal entries to record the transactions from 1 January 20x1 to 31 December 20x4. Narrations are not required. Ignore tax effect, if any. Supposing on 1 January 20x2, the management revised the exercise price of the share option to $8. As a result of this modification, the FV of the modified option on this date was estimated to be $3.25, while the FV of the original option on this date was $2.85 as shown on the table above. Compute the remuneration expense recorded for the years 20x2 and 20x3. Part A On 1 January 20x1, Sun-Bright Ltd (which adopts 31 December financial year-ends) launched an employee share option plan (ESOP) for the management team to enhance their motivation as well as improve retention rates. Each of its 10 managers was granted 100,000 share options at the exercise price of $9. The options would vest conditional upon the managers working for the company until 31 December 20x3 and would be forfeited if the manager leaves the company during the service period of three years. The options expire on 31 December 20x5. Actual and expected movement of the managers over the next three financial years ended 31 December are as follows: Estimated resignations Actual resignations 1 January 20x1 31 December 20x1 31 December 20x2 31 December 20x3 The estimated fair value (FV) of each option and the share price of Sun-Bright is given below: FV of share option Share price of shares 1 January 20x1 $3.75 31 December 20x1 $2.85 $8 31 December 20x2 $3.00 $8.25 31 December 20x3 $3.30 $8.75 31 December 20x4 $9.25 On 31 December 20x4, 5 managers exercised the share options granted to them

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts