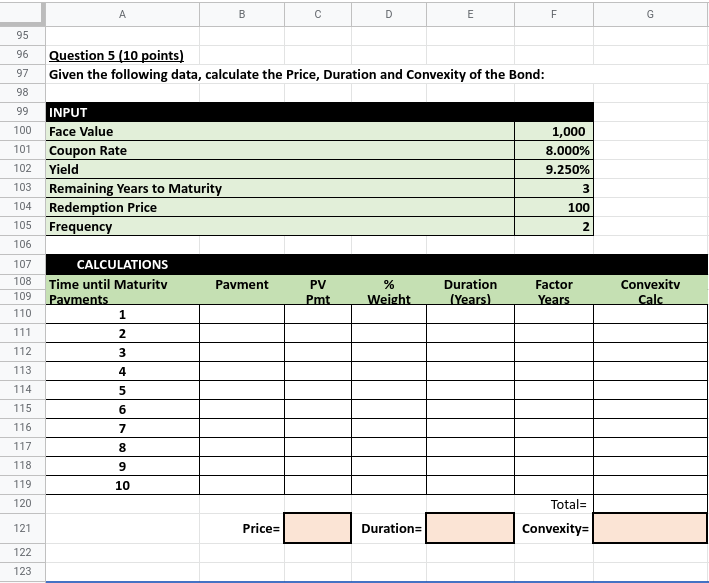

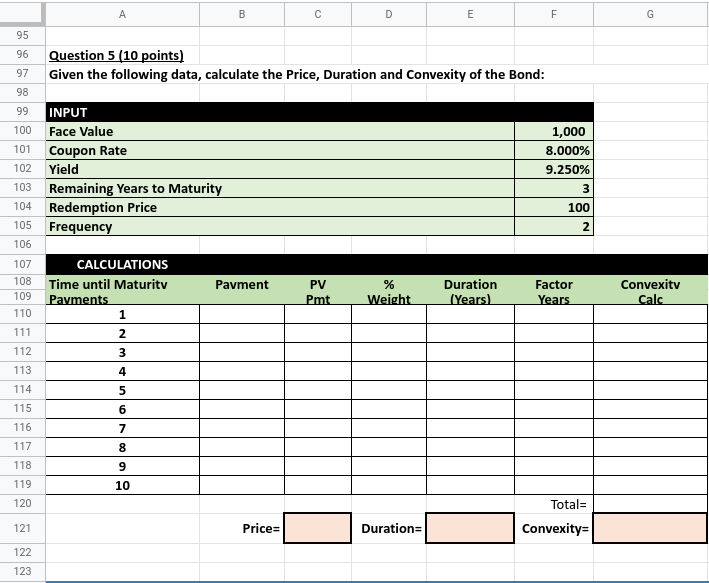

Question: A B C D E F G 95 96 Question 5 (10 points) 97 Given the following data, calculate the Price, Duration and Convexity of

A B C D E F G 95 96 Question 5 (10 points) 97 Given the following data, calculate the Price, Duration and Convexity of the Bond: 98 99 INPUT 100 Face Value 1,000 101 Coupon Rate 8.000% 102 Yield 9.250% 103 Remaining Years to Maturity 104 Redemption Price 100 105 Frequency 2 106 107 CALCULATIONS 108 109 Time until Maturity Payment PV % Payments Duration Factor Convexity Pit 110 Weight (Years) Years 1 Calc 111 IN 112 3 113 4 114 5 115 6 116 7 117 8 118 9 119 10 120 Total= 121 Price: Duration= Convexity= 122 123

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock