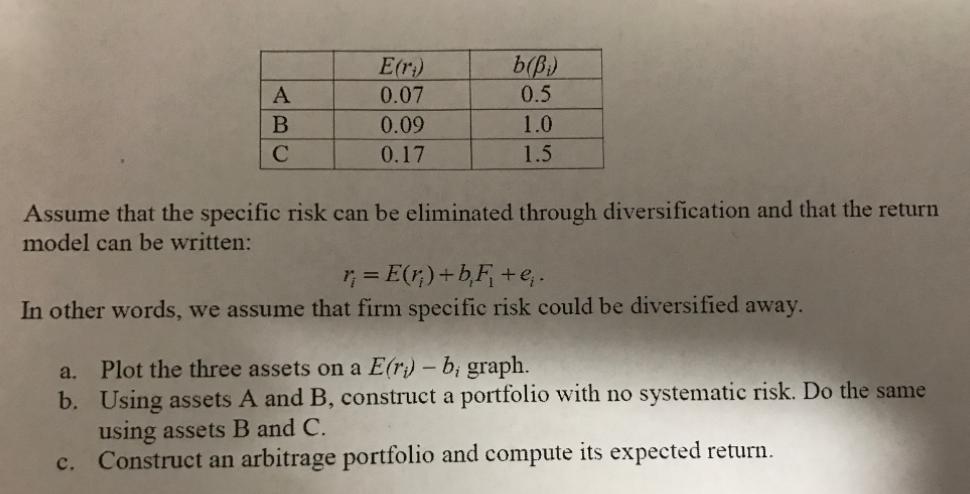

Question: A B E(r) 0.07 0.09 0.17 b(B) 0.5 1.0 1.5 Assume that the specific risk can be eliminated through diversification and that the return

A B E(r) 0.07 0.09 0.17 b(B) 0.5 1.0 1.5 Assume that the specific risk can be eliminated through diversification and that the return model can be written: a. b. r = E(r) + bF +e. In other words, we assume that firm specific risk could be diversified away. Plot the three assets on a E(r) - b, graph. Using assets A and B, construct a portfolio with no systematic risk. Do the same using assets B and C. c. Construct an arbitrage portfolio and compute its expected return.

Step by Step Solution

★★★★★

3.39 Rating (152 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock