Question: A bank is considering using a three against six $2,000,000 FRA to cover its potential loss. The purpose of the FRA is to cover the

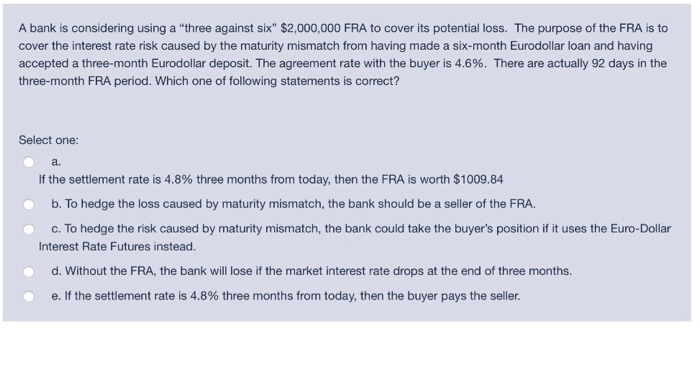

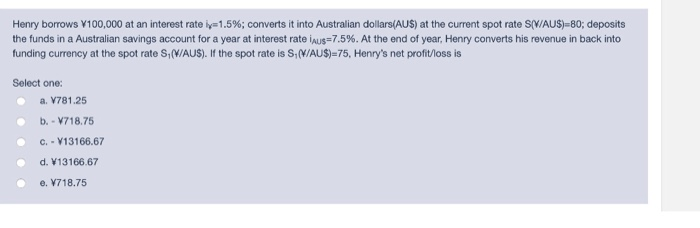

A bank is considering using a "three against six" $2,000,000 FRA to cover its potential loss. The purpose of the FRA is to cover the interest rate risk caused by the maturity mismatch from having made a six-month Eurodollar loan and having accepted a three-month Eurodollar deposit. The agreement rate with the buyer is 4.6%. There are actually 92 days in the three-month FRA period. Which one of following statements is correct? Select one: a. If the settlement rate is 4.8% three months from today, then the FRA is worth $1009.84 b. To hedge the loss caused by maturity mismatch, the bank should be a seller of the FRA. C. To hedge the risk caused by maturity mismatch, the bank could take the buyer's position if it uses the Euro-Dollar Interest Rate Futures instead. d. Without the FRA, the bank will lose if the market interest rate drops at the end of three months. e. If the settlement rate is 4.8% three months from today, then the buyer pays the seller. Henry borrows 7100,000 at an interest rate ir=1.5%; converts it into Australian dollars(AUS) at the current spot rate S/V/AUS)=80; deposits the funds in a Australian savings account for a year at interest rate ius=7.5%. At the end of year, Henry converts his revenue in back into funding currency at the spot rate S,(W/AUS). If the spot rate is S, (W/AUS)=75, Henry's net profit/loss is Select one: a. 1781.25 b. - V718.75 c. - V13166.67 d. V13166.67 e. V718.75

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts