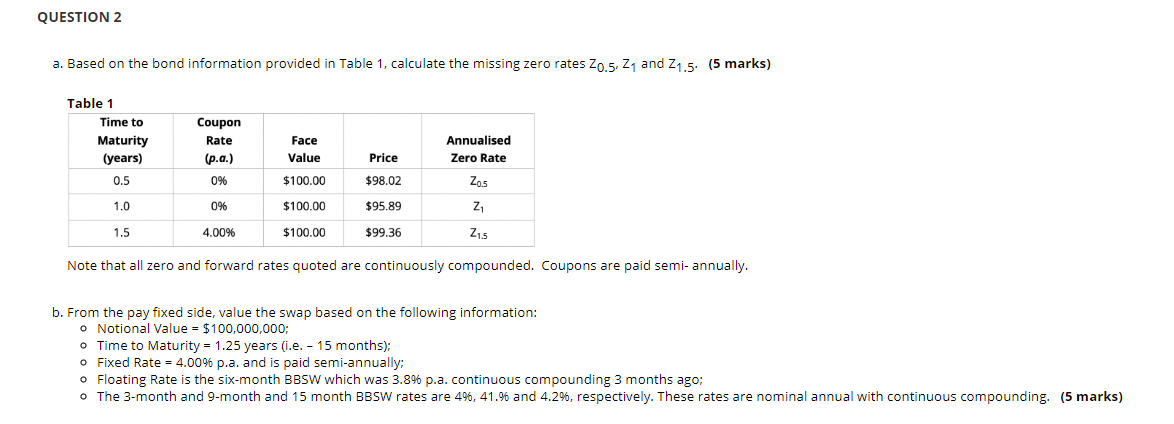

Question: a. Based on the bond information provided in Table 1, calculate the missing zero rates z0.5,z1 and z1.5. (5 marks) Note that all zero and

a. Based on the bond information provided in Table 1, calculate the missing zero rates z0.5,z1 and z1.5. (5 marks) Note that all zero and forward rates quoted are continuously compounded. Coupons are paid semi- annually. b. From the pay fixed side, value the swap based on the following information: - Notional Value =$100,000,000; - Time to Maturity =1.25 years (i.e. 15 months); - Fixed Rate =4.00% p.a. and is paid semi-annually; - Floating Rate is the six-month BBSW which was 3.8% p.a. continuous compounding 3 months ago; - The 3-month and 9-month and 15 month BBSW rates are 4%,41.% and 4.2%, respectively. These rates are nominal annual with continuous compounding. (5 marks) a. Based on the bond information provided in Table 1, calculate the missing zero rates z0.5,z1 and z1.5. (5 marks) Note that all zero and forward rates quoted are continuously compounded. Coupons are paid semi- annually. b. From the pay fixed side, value the swap based on the following information: - Notional Value =$100,000,000; - Time to Maturity =1.25 years (i.e. 15 months); - Fixed Rate =4.00% p.a. and is paid semi-annually; - Floating Rate is the six-month BBSW which was 3.8% p.a. continuous compounding 3 months ago; - The 3-month and 9-month and 15 month BBSW rates are 4%,41.% and 4.2%, respectively. These rates are nominal annual with continuous compounding

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts