Question: A . Compute the exchange exposure faced by the U . S . firm. B . What is the variance of the dollar price of

A Compute the exchange exposure faced by the US firm.

B What is the variance of the dollar price of this asset if the US firm remains unhedged against this exposure?

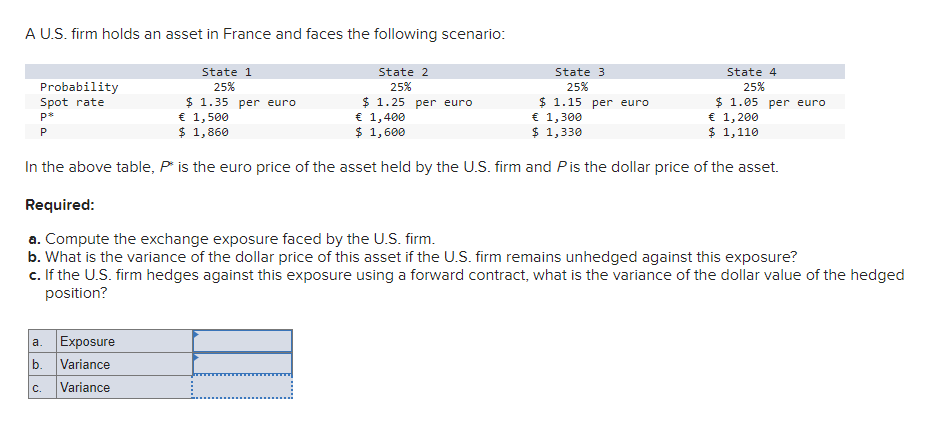

C IA US firm holds an asset in France and faces the following scenario:

In the above table, is the euro price of the asset held by the US firm and is the dollar price of the asset.

Required:

a Compute the exchange exposure faced by the US firm.

b What is the variance of the dollar price of this asset if the US firm remains unhedged against this exposure?

c If the US firm hedges against this exposure using a forward contract, what is the variance of the dollar value of the hedged

position?f the US firm hedges against this exposure using a forward contract, what is the variance of the dollar value of the hedged position?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock