Question: (a) Consider a discrete time market model with 2 time steps. In this model, the market consists of two assets, a risk-free asset such that

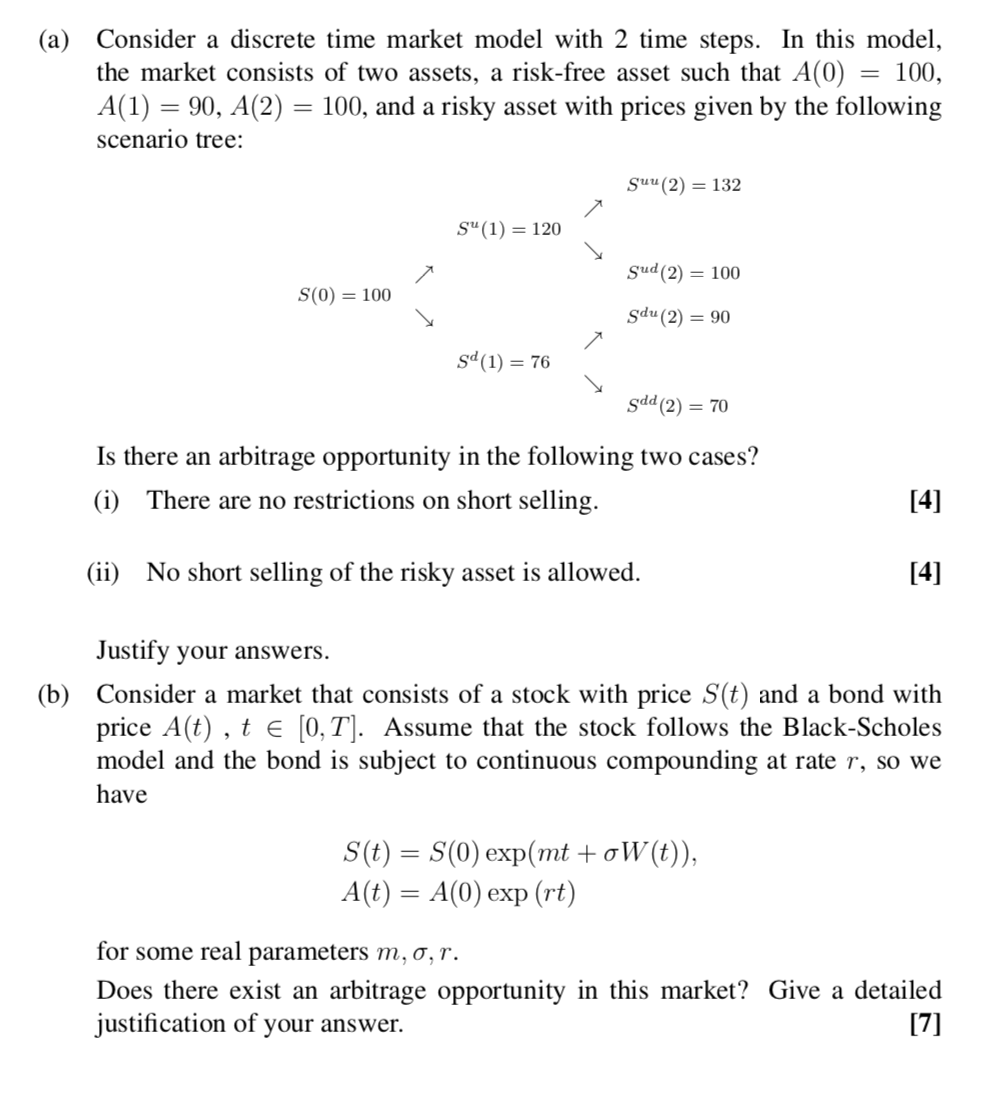

(a) Consider a discrete time market model with 2 time steps. In this model, the market consists of two assets, a risk-free asset such that A(0) 100, A(1) = 90, A(2) = 100, and a risky asset with prices given by the following scenario tree: Suu (2) = 132 S(1) = 120 gud(2) = 100 S(0) = 100 Sdu (2) = 90 sd(1) = 76 gdd (2) = 70 Is there an arbitrage opportunity in the following two cases? (i) There are no restrictions on short selling. [4] (ii) No short selling of the risky asset is allowed. [4] Justify your answers. (b) Consider a market that consists of a stock with price S(t) and a bond with price Aft), t E (0,T]. Assume that the stock follows the Black-Scholes model and the bond is subject to continuous compounding at rate r, so we have S(t) = S(0) exp(mt+oW(t)), A(t) = A(0) exp (rt) for some real parameters m, 0,r. Does there exist an arbitrage opportunity in this market? Give a detailed [7] justification of your answer. (c) Let N EN, N > 2 and consider a discrete time market model consisting of two assets: a risky one and a risk-free one. So, stock price is given by a sequence of random variables S(t), t = 0, ...,N. Please mind that we do not assume any specific structure of the sequence of random variables S(t). In particular, we do not assume the binomial tree model in this problem. The risk-free asset prices form a deterministic sequence At), t = 0, ...,N such that Alt) > 0 for all t = 0,...,N. Assume that you know a self-financing predictable trading strategy with wealth process V(t), t = 0, ...,N, which satisfies the following properties (i) V(0)=0, (ii) for some k E N, 0 0 in all scenarios. Is it true or false that in this situation there necessarily exists an arbitrage opportunity? Justify your answer. [10] (a) Consider a discrete time market model with 2 time steps. In this model, the market consists of two assets, a risk-free asset such that A(0) 100, A(1) = 90, A(2) = 100, and a risky asset with prices given by the following scenario tree: Suu (2) = 132 S(1) = 120 gud(2) = 100 S(0) = 100 Sdu (2) = 90 sd(1) = 76 gdd (2) = 70 Is there an arbitrage opportunity in the following two cases? (i) There are no restrictions on short selling. [4] (ii) No short selling of the risky asset is allowed. [4] Justify your answers. (b) Consider a market that consists of a stock with price S(t) and a bond with price Aft), t E (0,T]. Assume that the stock follows the Black-Scholes model and the bond is subject to continuous compounding at rate r, so we have S(t) = S(0) exp(mt+oW(t)), A(t) = A(0) exp (rt) for some real parameters m, 0,r. Does there exist an arbitrage opportunity in this market? Give a detailed [7] justification of your answer. (c) Let N EN, N > 2 and consider a discrete time market model consisting of two assets: a risky one and a risk-free one. So, stock price is given by a sequence of random variables S(t), t = 0, ...,N. Please mind that we do not assume any specific structure of the sequence of random variables S(t). In particular, we do not assume the binomial tree model in this problem. The risk-free asset prices form a deterministic sequence At), t = 0, ...,N such that Alt) > 0 for all t = 0,...,N. Assume that you know a self-financing predictable trading strategy with wealth process V(t), t = 0, ...,N, which satisfies the following properties (i) V(0)=0, (ii) for some k E N, 0 0 in all scenarios. Is it true or false that in this situation there necessarily exists an arbitrage opportunity? Justify your answer. [10]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts