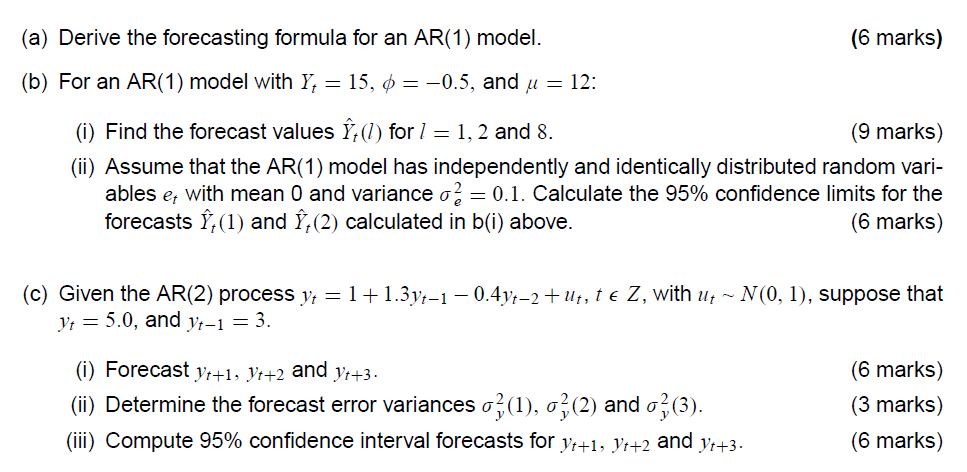

Question: (a) Derive the forecasting formula for an AR(1) model. (6 marks) (b) For an AR(1) model with Y, = 15, p = -0.5, and u

(a) Derive the forecasting formula for an AR(1) model. (6 marks) (b) For an AR(1) model with Y, = 15, p = -0.5, and u = 12: (i) Find the forecast values Y, (1) for / = 1, 2 and 8. (9 marks) (ii) Assume that the AR(1) model has independently and identically distributed random vari- ables e, with mean 0 and variance o = 0.1. Calculate the 95% confidence limits for the forecasts Y, (1) and Y, (2) calculated in b(i) above. (6 marks) (c) Given the AR(2) process y, = 1 + 1.3y-1 - 0.4yr-2 + ut, te Z, with ut ~ N(0, 1), suppose that yt = 5.0, and yr-1 = 3. (i) Forecast yi+1, 1+2 and y1+3. (6 marks) (ii) Determine the forecast error variances o? (1), o (2) and o? (3). (3 marks) (iii) Compute 95% confidence interval forecasts for yr+1, Vi+2 and yr+3. (6 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts