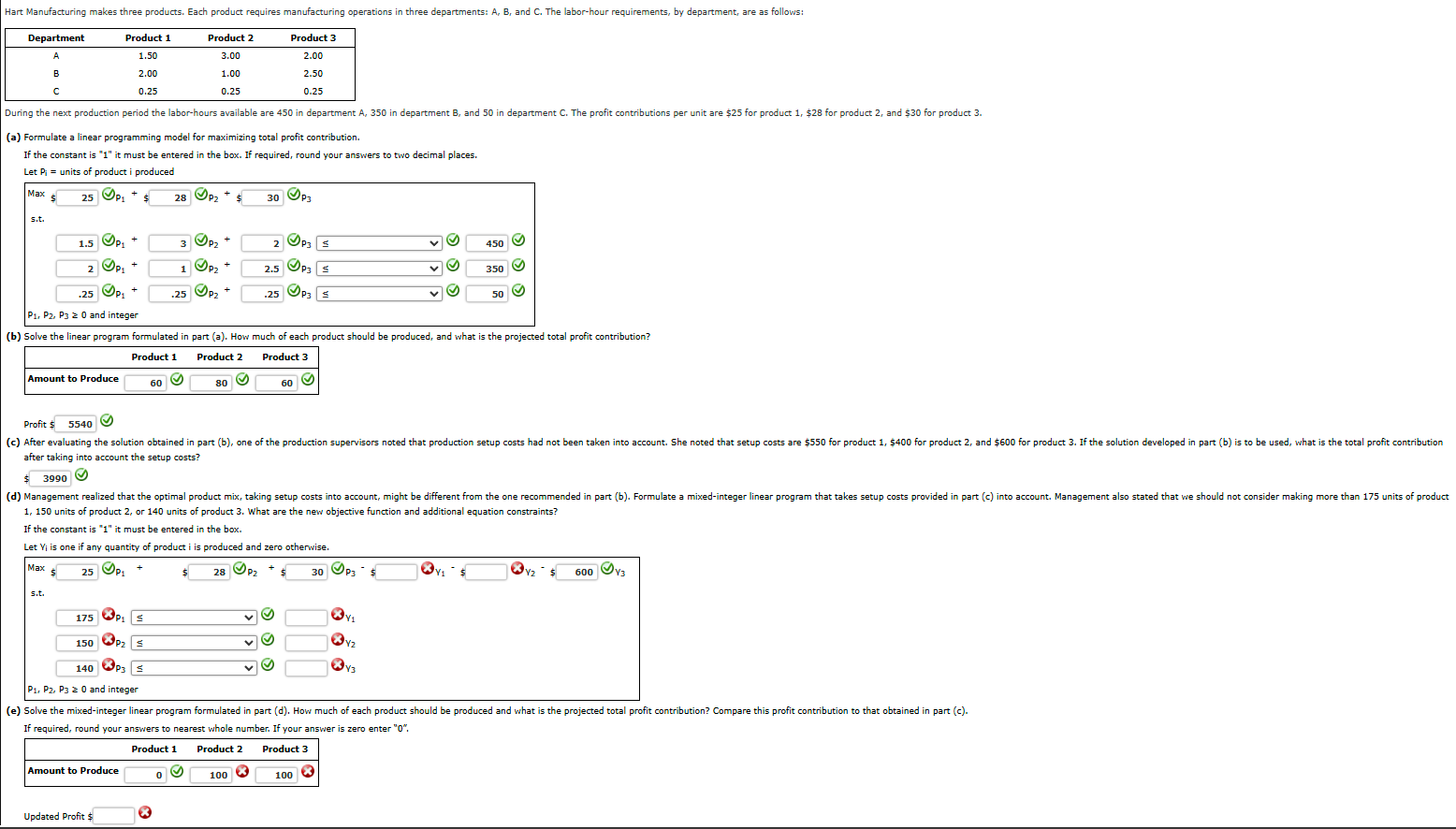

Question: ( a ) Formulate a linear programming model for maximizing total profit contribution. If the constant is 1 it must be entered in

a Formulate a linear programming model for maximizing total profit contribution.

If the constant is it must be entered in the box. If required, round your answers to two decimal places.

Let mathrmPmathrmi units of product i produced

b Solve the linear program formulated in part a How much of each product should be produced, and what is the projected total profit contribution?

Profit $ after taking into account the setup costs?

$ units of product or units of product What are the new objective function and additional equation constraints?

If the constant is it must be entered in the box.

Let mathrmVmathrmi is one if any quantity of product i is produced and zero otherwise.

e Solve the mixedinteger linear program formulated in part d How much of each product should be produced and what is the projected total profit contribution? Compare this profit contribution to that obtained in part c If required, round your answers to nearest whole number. If your answer is zero enter

Updated Profit $

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To solve this linear programming problem lets break it down into steps Part a Formulate the Linear P... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock