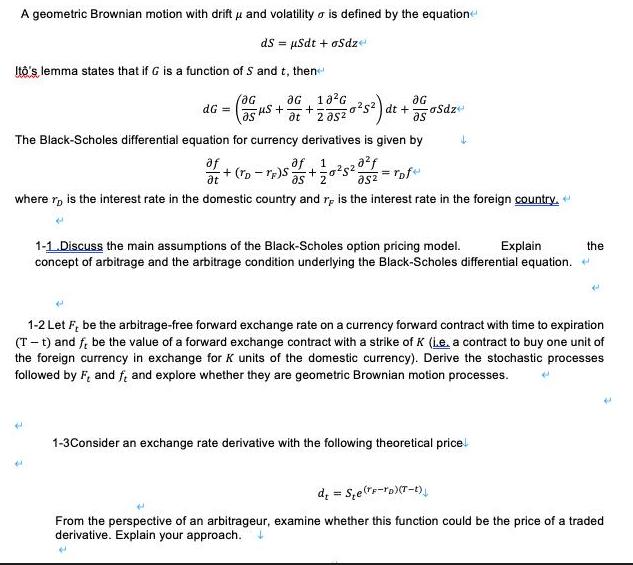

A geometric Brownian motion with drift and volatility is defined by the equation ds =...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: