Question: (a) Given an initial condition for ya. answer the following questions. where y; is the random variable at time t, s is the error, I

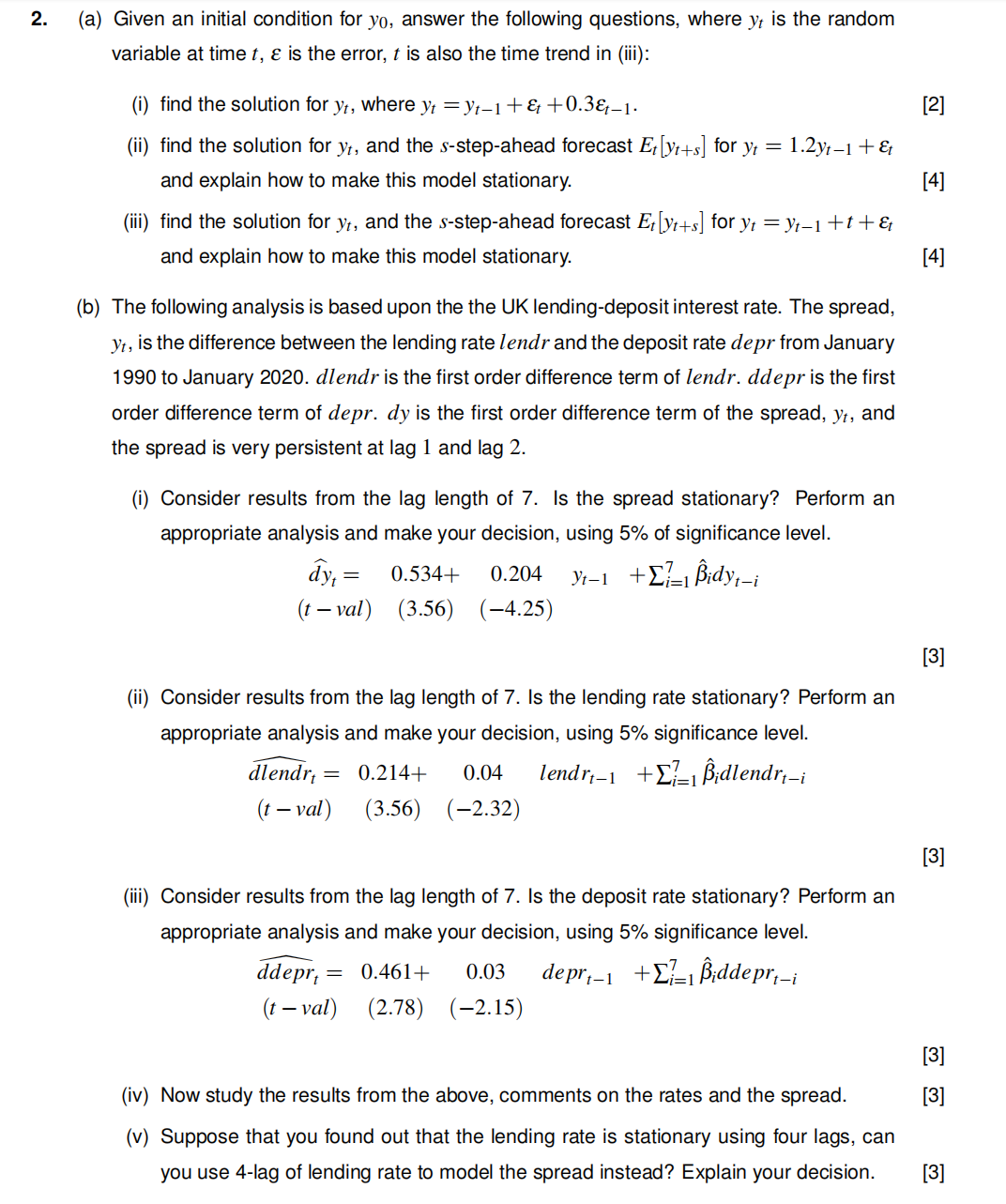

(a) Given an initial condition for ya. answer the following questions. where y; is the random variable at time t, s is the error, I is also the time trend in (iii): (i) find the solution for y,, where y; =y,_1+ 8: +0.3,_1. (ii) find the solution for yr. and the s-step-ahead forecast E([y(+5] for y; = 1.2y;_1 + E: and explain how to make this model stationary. (iii) find the solution for y\" and the s-step-ahead forecast E, [ym] for y; = y,_1 + r + s: and explain how to make this model stationary. (b) The following analysis is based upon the the UK lending-deposit interest rate. The spread, y\" is the difference between the lending rate lendr and the deposit rate depr from January 1990 to January 2020. dlendr is the first order difference term of lendr. ddepr is the first order difference term of depr. dy is the first order difference term of the spread. yr, and the spread is very persistent at lag l and lag 2. (i) Consider results from the lag length of 7. Is the spread stationary? Perform an appropriate analysis and make your decision, using 5% of significance level. .5332, = 0534+ 0.204 y,_1 +2=1fidy,_i (r va) (3.56) (4.25) (ii) Consider results from the lag length of 7. Is the lending rate stationary? Perform an appropriate analysis and make your decision, using 5% significance level. Mr, = 0214+ 0.04 sendr,_1 + 23:] Bidlendr,_l- (r val) (3.56) (2.32) (iii) Consider results from the lag length of 7. Is the deposit rate stationary? Perform an appropriate analysis and make your decision, using 5% significance level. (Mr = {1461+ 0.03 depr,_1 +3=1iddepr,_i (r val) (2.78) (2.15) (iv) Now study the results from the above. comments on the rates and the spread. (v) Suppose that you found out that the lending rate is stationary using four lags, can you use 4-lag of lending rate to model the spread instead? Explain your decision. [2] [4] [4] [3] [3] [3] [3] [3]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts