Question: (a) Given this benchmark interest rates and volatility, the OAS with a particular option-embedded bond issue is 40 bp. Explain what the OAS measures (b)

(a) Given this benchmark interest rates and volatility, the OAS with a particular option-embedded bond issue is 40 bp. Explain what the OAS measures

(b) The issuer has a 3-year 6% callable bond (par $100 annual payment), with call rule Year 1 $101 and Year 2 $100. With OAS = 40bp, compute the value of this 3-year 6% callable bond.

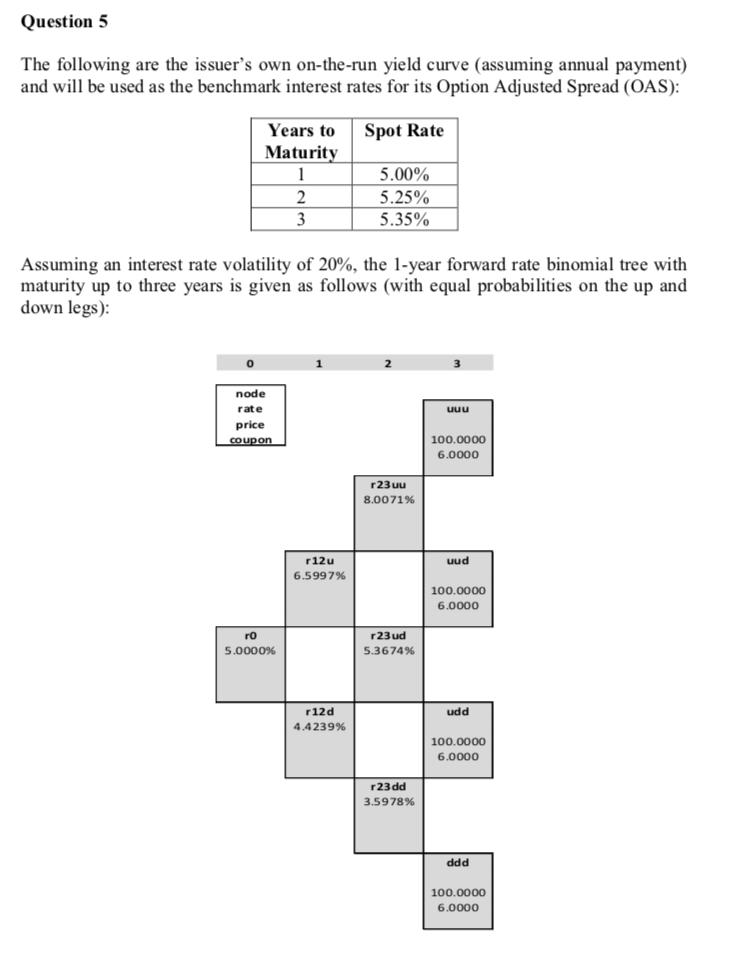

Question 5 The following are the issuer's own on-the-run yield curve (assuming annual payment) and will be used as the benchmark interest rates for its Option Adjusted Spread (OAS) Years toSpot Rate Maturit 5.00% 5.25% 5.35% Assuming an interest rate volatility of 20%, the 1-year forward rate binomial tree with maturity up to three years is given as follows (with equal probabilities on the up and down legs) 0 node rate price 100.0000 6.0000 r23 uu 8.00 71% r12u 6.5997% uud 100.0000 6.0000 ro 5.0000% r23 ud 5.3674% r12d 4.4239% udd 100.0000 6.0000 r23dd 3.5978% 100.0000 6.0000 Question 5 The following are the issuer's own on-the-run yield curve (assuming annual payment) and will be used as the benchmark interest rates for its Option Adjusted Spread (OAS) Years toSpot Rate Maturit 5.00% 5.25% 5.35% Assuming an interest rate volatility of 20%, the 1-year forward rate binomial tree with maturity up to three years is given as follows (with equal probabilities on the up and down legs) 0 node rate price 100.0000 6.0000 r23 uu 8.00 71% r12u 6.5997% uud 100.0000 6.0000 ro 5.0000% r23 ud 5.3674% r12d 4.4239% udd 100.0000 6.0000 r23dd 3.5978% 100.0000 6.0000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts