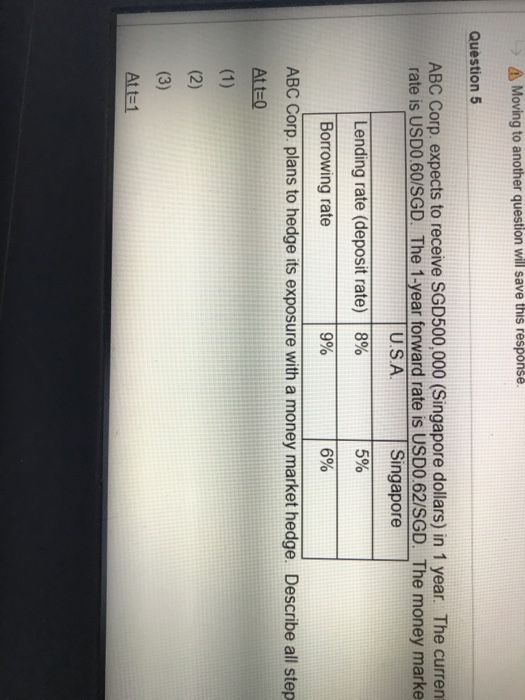

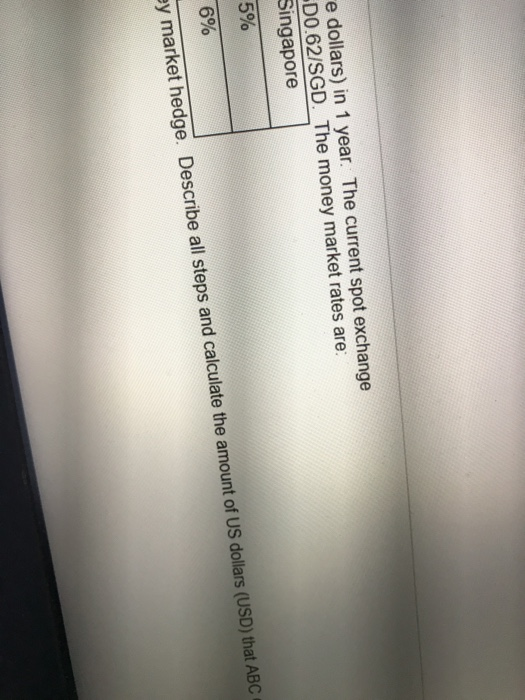

Question: A Moving to another question will save this response. Question 5 ABC Corp. expects to receive SGD500,000 (Singapore dollars) in 1 year. The current rate

A Moving to another question will save this response. Question 5 ABC Corp. expects to receive SGD500,000 (Singapore dollars) in 1 year. The current rate is USD0.60/SGD. The 1-year forward rate is USD0.62/SGD. The money marke U.S.A. Singapore Lending rate (deposit rate) 8% 5% Borrowing rate 9% 6% ABC Corp. plans to hedge its exposure with a money market hedge. Describe all step At t=0 (2) (3) Att1 e dollars) in 1 year. The current spot exchange D0.62/SGD. The money market rates are: Singapore 5% 6% ey market hedge. Describe all steps and calculate the amount of US dollars (USD) that ABC

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock