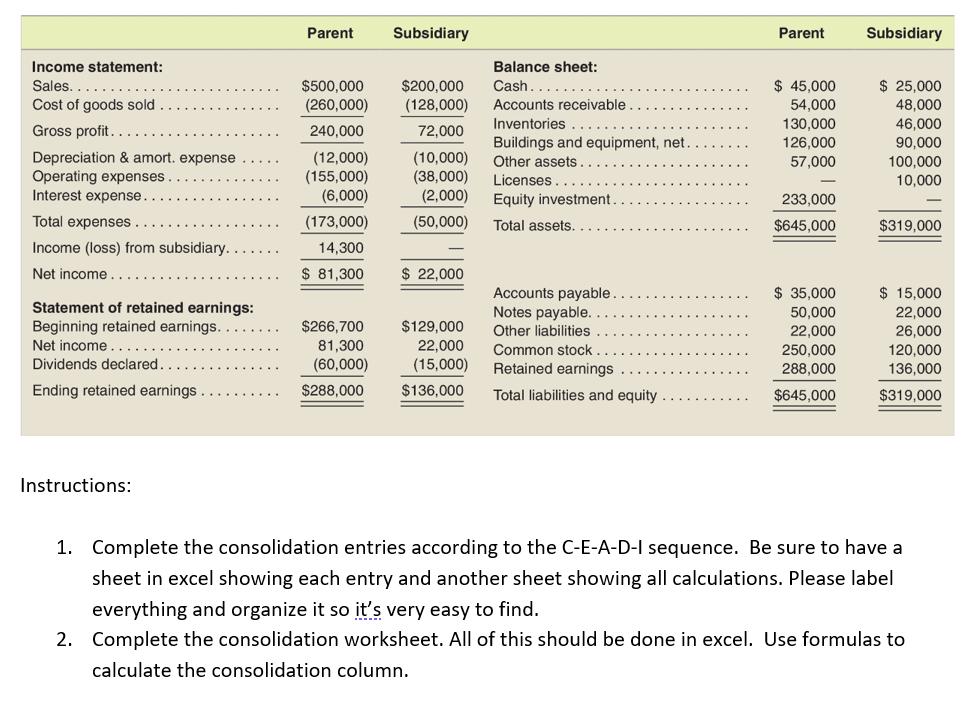

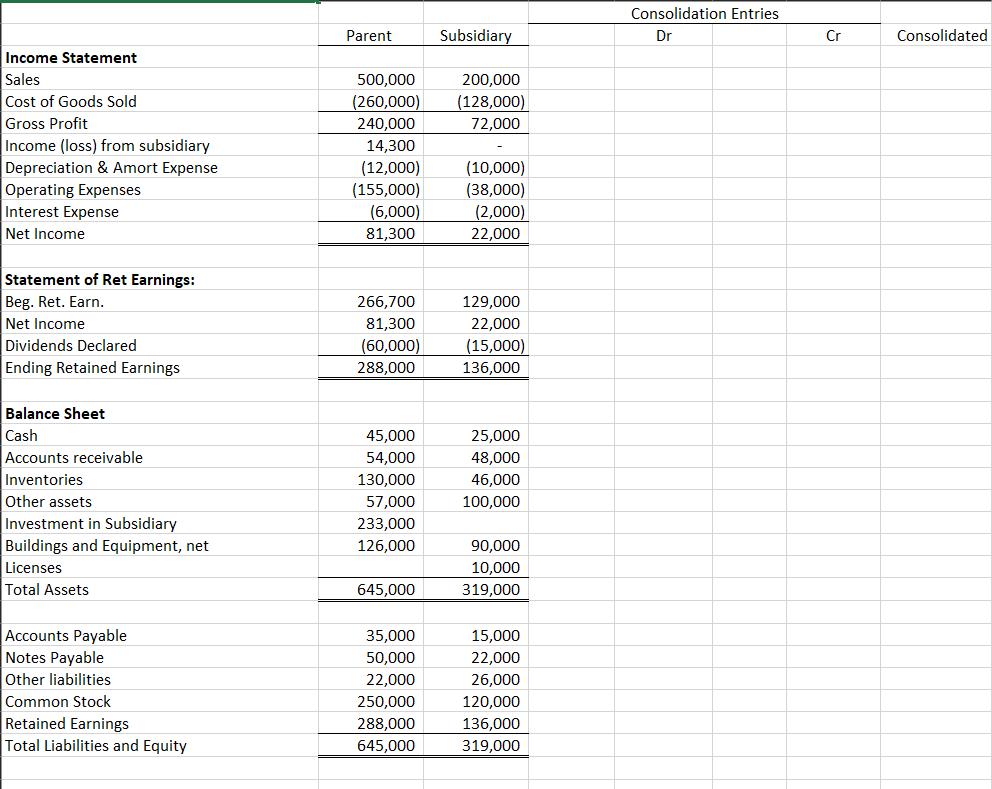

A parent company acquired 80% of the stock of a subsidiary company on January 1, 2015....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

A parent company acquired 80% of the stock of a subsidiary company on January 1, 2015. The total fair value of the controlling interest and the noncontrolling interest on that date was 94,000 in excess of the book value of the subsidiary's stockholders' equity on the acquisition date. $18,000 was assigned to building and equipment and was to be depreciated for 6 years. $42,000 was assigned to a license and amortized over 7 years and the remaining $34,000 was goodwill. The goodwill is not quite split 80/20 between the parent and subsidiary. For consolidation split the goodwill portion $27,800 to parent and remaining $6,200 to subsidiary. The other AAP assets will still have an 80/20 split. On January 1, 2018, the parent sold a building to the subsidiary for $80,000. On this date, the building was carried on the parent's books (net of accumulated depreciation) at $65,000. Both companies estimated that the building has a remaining life of 6 years on the intercompany sale date, with no salvage value. Each company routinely sells merchandise to the other company, with a profit margin of 25 percent of selling price (regardless of the direction of the sale). During 2019, intercompany sales amount to $15,000, of which $8,000 of merchandise remains in the ending inventory of the parent. On December 31, 2019, $4,000 of these intercompany sales remained unpaid. Additionally, the subsidiary's December 31, 2018 inventory includes $12,000 of merchandise purchased in the preceding year from the parent. During 2018, intercompany sales amount to $20,000, and on December 31, 2018, $6,000 of these intercompany sales remained unpaid. The parent accounts for its Equity Investment in the subsidiary using the equity method. The pre- consolidation financial statements for the two companies for the year ended December 31, 2019, are provided below: Income statement: Sales. Cost of goods sold Gross profit. Depreciation & amort. expense Operating expenses. Interest expense. Total expenses Income (loss) from subsidiary.. Net income Statement of retained earnings: Beginning retained earnings. Net income. Dividends declared. Ending retained earnings Instructions: Parent $500,000 (260,000) 240,000 (12,000) (155,000) (6,000) (173,000) 14,300 $ 81,300 $266,700 81,300 (60,000) $288,000 Subsidiary $200,000 (128,000) 72,000 (10,000) (38,000) (2,000) (50,000) $ 22,000 $129,000 22,000 (15,000) $136,000 Balance sheet: Cash. Accounts receivable Inventories Buildings and equipment, net Other assets Licenses Equity investment. Total assets. Accounts payable. Notes payable. Other liabilities. Common stock. Retained earnings Total liabilities and equity Parent $ 45,000 54,000 130,000 126,000 57,000 233,000 $645,000 $ 35,000 50,000 22,000 250,000 288,000 $645,000 Subsidiary $ 25,000 48,000 46,000 90,000 100,000 10,000 $319,000 $ 15,000 22,000 26,000 120,000 136,000 $319,000 1. Complete the consolidation entries according to the C-E-A-D-I sequence. Be sure to have a sheet in excel showing each entry and another sheet showing all calculations. Please label everything and organize it so it's very easy to find. 2. Complete the consolidation worksheet. All of this should be done in excel. Use formulas to calculate the consolidation column. Income Statement Sales Cost of Goods Sold Gross Profit Income (loss) from subsidiary Depreciation & Amort Expense Operating Expenses Interest Expense Net Income Statement of Ret Earnings: Beg. Ret. Earn. Net Income Dividends Declared Ending Retained Earnings Balance Sheet Cash Accounts receivable Inventories Other assets Investment in Subsidiary Buildings and Equipment, net Licenses Total Assets Accounts Payable Notes Payable Other liabilities Common Stock Retained Earnings Total Liabilities and Equity Parent 500,000 200,000 (260,000) (128,000) 240,000 72,000 14,300 (12,000) (155,000) (6,000) 81,300 266,700 81,300 (60,000) 288,000 45,000 54,000 130,000 57,000 233,000 126,000 645.000 Subsidiary 35,000 50,000 22,000 250,000 288,000 645,000 (10,000) (38,000) (2,000) 22,000 129,000 22,000 (15,000) 136,000 25,000 48,000 46,000 100,000 90,000 10,000 319,000 15,000 22,000 26,000 120,000 136,000 319,000 Consolidation Entries Dr Cr Consolidated A parent company acquired 80% of the stock of a subsidiary company on January 1, 2015. The total fair value of the controlling interest and the noncontrolling interest on that date was 94,000 in excess of the book value of the subsidiary's stockholders' equity on the acquisition date. $18,000 was assigned to building and equipment and was to be depreciated for 6 years. $42,000 was assigned to a license and amortized over 7 years and the remaining $34,000 was goodwill. The goodwill is not quite split 80/20 between the parent and subsidiary. For consolidation split the goodwill portion $27,800 to parent and remaining $6,200 to subsidiary. The other AAP assets will still have an 80/20 split. On January 1, 2018, the parent sold a building to the subsidiary for $80,000. On this date, the building was carried on the parent's books (net of accumulated depreciation) at $65,000. Both companies estimated that the building has a remaining life of 6 years on the intercompany sale date, with no salvage value. Each company routinely sells merchandise to the other company, with a profit margin of 25 percent of selling price (regardless of the direction of the sale). During 2019, intercompany sales amount to $15,000, of which $8,000 of merchandise remains in the ending inventory of the parent. On December 31, 2019, $4,000 of these intercompany sales remained unpaid. Additionally, the subsidiary's December 31, 2018 inventory includes $12,000 of merchandise purchased in the preceding year from the parent. During 2018, intercompany sales amount to $20,000, and on December 31, 2018, $6,000 of these intercompany sales remained unpaid. The parent accounts for its Equity Investment in the subsidiary using the equity method. The pre- consolidation financial statements for the two companies for the year ended December 31, 2019, are provided below: Income statement: Sales. Cost of goods sold Gross profit. Depreciation & amort. expense Operating expenses. Interest expense. Total expenses Income (loss) from subsidiary.. Net income Statement of retained earnings: Beginning retained earnings. Net income. Dividends declared. Ending retained earnings Instructions: Parent $500,000 (260,000) 240,000 (12,000) (155,000) (6,000) (173,000) 14,300 $ 81,300 $266,700 81,300 (60,000) $288,000 Subsidiary $200,000 (128,000) 72,000 (10,000) (38,000) (2,000) (50,000) $ 22,000 $129,000 22,000 (15,000) $136,000 Balance sheet: Cash. Accounts receivable Inventories Buildings and equipment, net Other assets Licenses Equity investment. Total assets. Accounts payable. Notes payable. Other liabilities. Common stock. Retained earnings Total liabilities and equity Parent $ 45,000 54,000 130,000 126,000 57,000 233,000 $645,000 $ 35,000 50,000 22,000 250,000 288,000 $645,000 Subsidiary $ 25,000 48,000 46,000 90,000 100,000 10,000 $319,000 $ 15,000 22,000 26,000 120,000 136,000 $319,000 1. Complete the consolidation entries according to the C-E-A-D-I sequence. Be sure to have a sheet in excel showing each entry and another sheet showing all calculations. Please label everything and organize it so it's very easy to find. 2. Complete the consolidation worksheet. All of this should be done in excel. Use formulas to calculate the consolidation column. Income Statement Sales Cost of Goods Sold Gross Profit Income (loss) from subsidiary Depreciation & Amort Expense Operating Expenses Interest Expense Net Income Statement of Ret Earnings: Beg. Ret. Earn. Net Income Dividends Declared Ending Retained Earnings Balance Sheet Cash Accounts receivable Inventories Other assets Investment in Subsidiary Buildings and Equipment, net Licenses Total Assets Accounts Payable Notes Payable Other liabilities Common Stock Retained Earnings Total Liabilities and Equity Parent 500,000 200,000 (260,000) (128,000) 240,000 72,000 14,300 (12,000) (155,000) (6,000) 81,300 266,700 81,300 (60,000) 288,000 45,000 54,000 130,000 57,000 233,000 126,000 645.000 Subsidiary 35,000 50,000 22,000 250,000 288,000 645,000 (10,000) (38,000) (2,000) 22,000 129,000 22,000 (15,000) 136,000 25,000 48,000 46,000 100,000 90,000 10,000 319,000 15,000 22,000 26,000 120,000 136,000 319,000 Consolidation Entries Dr Cr Consolidated

Expert Answer:

Answer rating: 100% (QA)

To complete the consolidation entries and worksheet we need to follow the CEADI sequence C Combine the balance sheet accounts eliminating intercompany transactions E Eliminate the subsidiarys equity a... View the full answer

Posted Date:

Students also viewed these accounting questions

-

Consider the goods market model where consumption is given by: C = Co + C(Y-T), investment is given by: I = bo + bY - bi, and G and T are given. Assuming Co 100, C1 = 0.6, bo = 150, b be the change...

-

A parent company acquired a 75% interest in a subsidiary company in Year 4. The acquisition price was $1,000,000, made up of cash of $700,000 and the parents common shares with a current market value...

-

Find the average rate of change of f(x) = x3 - 6x +7 over the following intervals. (a) From 7 to -4 (b) From 1 to 3 (c) From 3 to 8 (a)The average rate of change from 7 to -4 is

-

The need to be liked and to stay on good terms with most other people is the need for? a. Affiliation b. Power c. None of the above d. Achievement

-

When Phil died in the current year, he owned shares of Orange Corporation which are traded in the over-the-counter market. The market trades before and after Phils date of death occurred as follows....

-

Least squares regression finds the estimated values for the parameters in a regression model to minimize Why is it necessary to square the estimation errors? What problem might be encountered if we...

-

You have two cylindrical solenoids, one inside the other, with the two cylinders concentric. The outer solenoid has length \(\ell_{\text {ourer }}=400 \mathrm{~mm}\), radius \(R_{\text {outer }}=50...

-

Condensed balance sheet and income statement data for Glassgow Corporation are presented here. Additional information:1. The market price of Glassgow's common stock was $7.00, $7.50, and $8.50 for...

-

What two different types of firmware may be used on motherboards? a. POST b. UEFI c. CMOS d. BIOS

-

Using the same data set as in Exercise 3 and for house price growth, run several regression models with one, two, three, and four lags of price growth in the right-hand side of the model. Analyze the...

-

Under this approach, employees are given complete power to make decisions about their work. Managers are either eliminated, or their work is reconfigured to be supportive, not directive. Employee...

-

In the Disney Pixar case - 'the walt disney company and pixar inc. to acquire or not to acquire' one of the key risks Pixar feared was after acquisition Pixar's innovation culture would be...

-

What feature can only be accessed from the Format Cells dialog box?

-

Provide an introduction to the report including a summary of business requirements. This can be a summary of information that you provided in Section 1 of your Portfolio plus the rationale for...

-

Provides and in-depth discussion of the information that might be required to complete those reports, the reasons for completing those reports, the necessity of ensuring accuracy in reporting and the...

-

Describe the scope of financial accounting, including the recording, summarizing, and reporting of financial transactions Explain how the information provided by managerial accounting is used by...

-

3. 4. PC Exchange Company, a computer store in Greenhills, specializes in the sale of IBM compatibles and software packages and had the following transactions with one of its suppliers: Purchases of...

-

1A. If the researcher is concerned about the number of variables, the nature of the analysis, and completion rates, then, he/she is at which stage of the sampling design process (Figure 11.1 in the...

-

Use the magnitudes (Richter scale) of the earthquakes listed in Data Set 16 in Appendix B. In 1989, the San Francisco Bay Area was struck with an earthquake that measured 7.0 on the Richter scale....

-

James Madison, the fourth President of the United States, was 163 cm tall. His height converts to the z score of -2.28 when included among the heights of all presidents. Is his height above or below...

-

Carbon monoxide is measured in San Francisco on five different days, and the mean of those five values is 0.62 parts per million. Four of the values (in parts per million) are 0.3, 0.4, 1.1, and 0.7....

Study smarter with the SolutionInn App