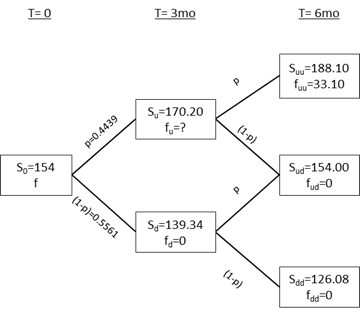

Question: A partial two-stage binomial tree is shown below for an American call option with a strike price of $155, spot price of $154, and volatility

A partial two-stage binomial tree is shown below for an American call option with a strike price of $155, spot price of $154, and volatility () of 20%. The risk-free rate is 1% per annum compounded continuously.

If the value of fu in the tree above turns out to be 10 , what would be the value (f) of this option today?

Answer Choices

f 5

5

15

30

f > 45

T=0 T= 3mo T= 6mo Suu=188.10 fuu=33.10 Sy=170.20 f,=? (1-P) - p=0.4439 So=154 f Sud=154.00 fud=0 (1-2)=0.5561 Sg-139.34 fq=0 (1-0) Sca=126.08 fd=0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock