Question: A pension fund manager is considering three mutual funds: a stock fund, a long-term bond fund and a money market fund that provides a risk-free

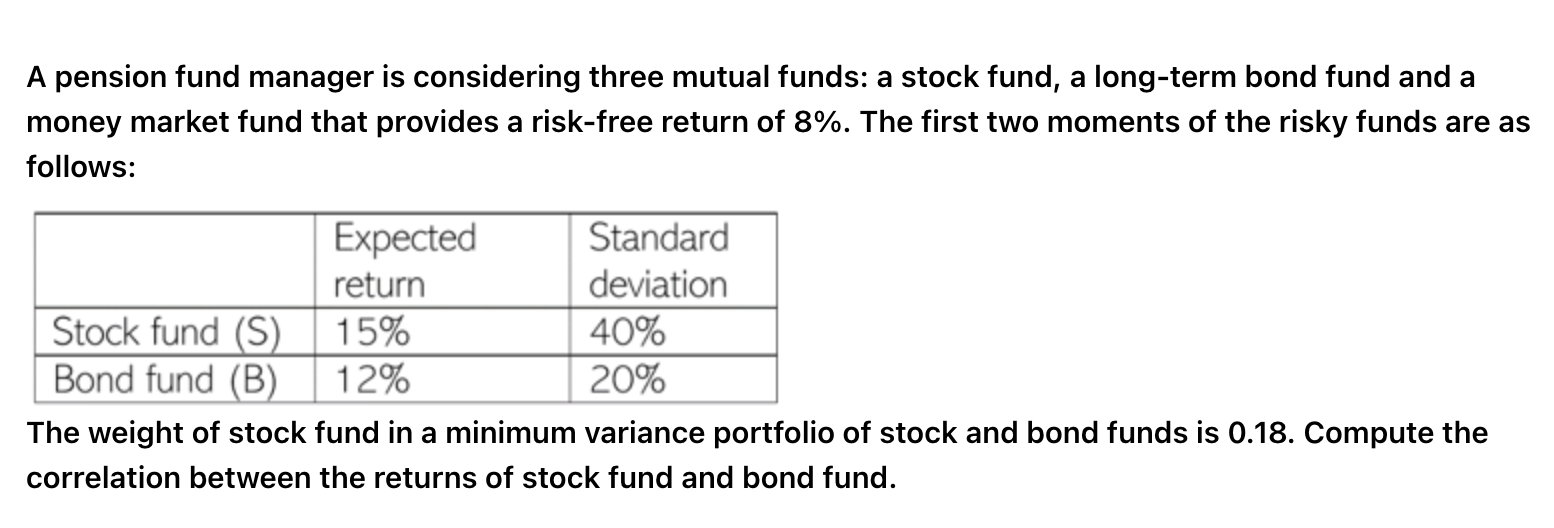

A pension fund manager is considering three mutual funds: a stock fund, a long-term bond fund and a money market fund that provides a risk-free return of 8%. The first two moments of the risky funds are as follows: The weight of stock fund in a minimum variance portfolio of stock and bond funds is 0.18. Compute the correlation between the returns of stock fund and bond fund

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock