Question: BKM Ch 6 problems ( Connect / Problem Sets ) 3 , 8 , 1 7 A portfolio's expected return is 1 2 % ,

BKM Ch problems ConnectProblem Sets

A portfolio's expected return is its standard deviation is and the riskfree rate is What Sharpe ratio

would result from each of the following changes?

a An increase of in the portfolio's expected return.

b A decrease of in the riskfree rate.

c A decrease of in the portfolio's standard deviation.

A pension fund manager is considering three mutual funds, a stock fund with expected return of and standard

deviation of a bond fund with expected return of and standard deviation of and a money market fund

with a sure rate of The correlation between the stock and bond funds is Tabulate and draw the investment

opportunity set of the two risky funds, using investment proportions for the stock fund from to in

increments of What is the lowestrisk of these combinations of the stock and bond funds?

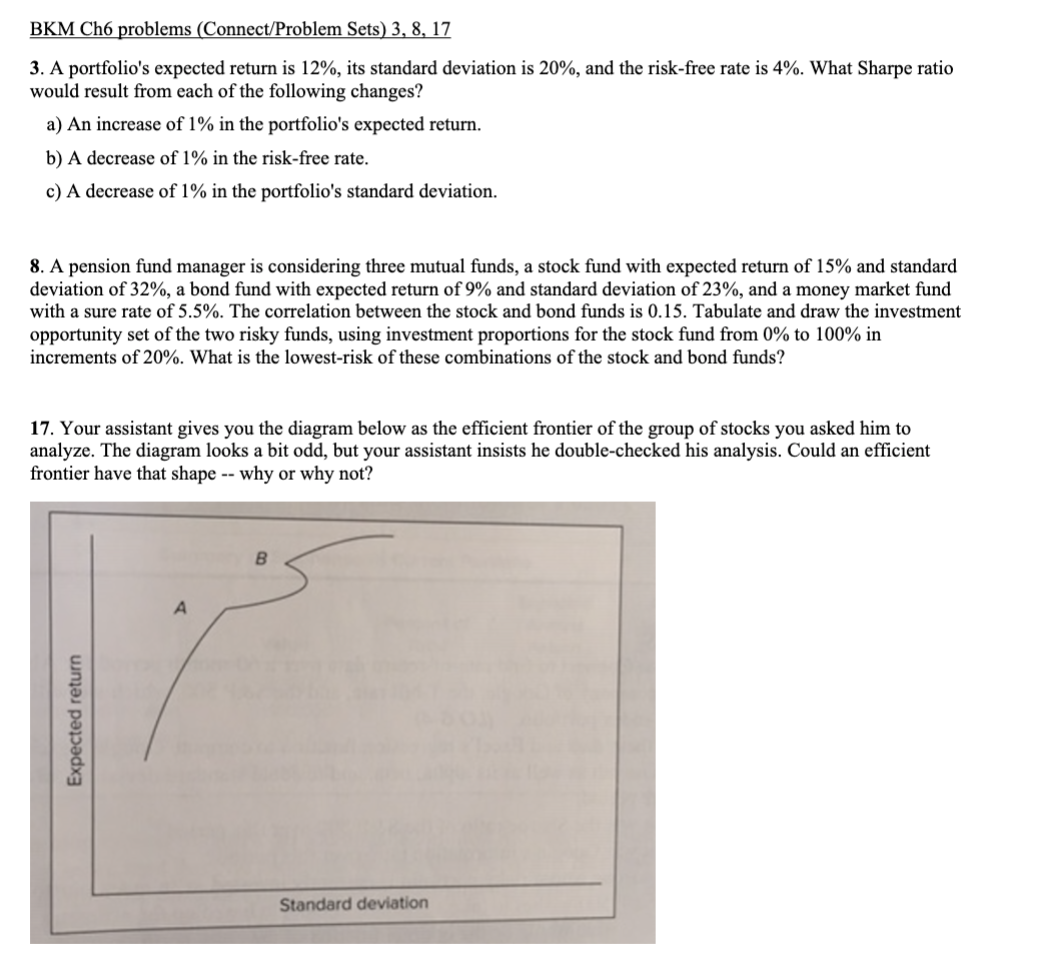

Your assistant gives you the diagram below as the efficient frontier of the group of stocks you asked him to

analyze. The diagram looks a bit odd, but your assistant insists he doublechecked his analysis. Could an efficient

frontier have that shape why or why not?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock