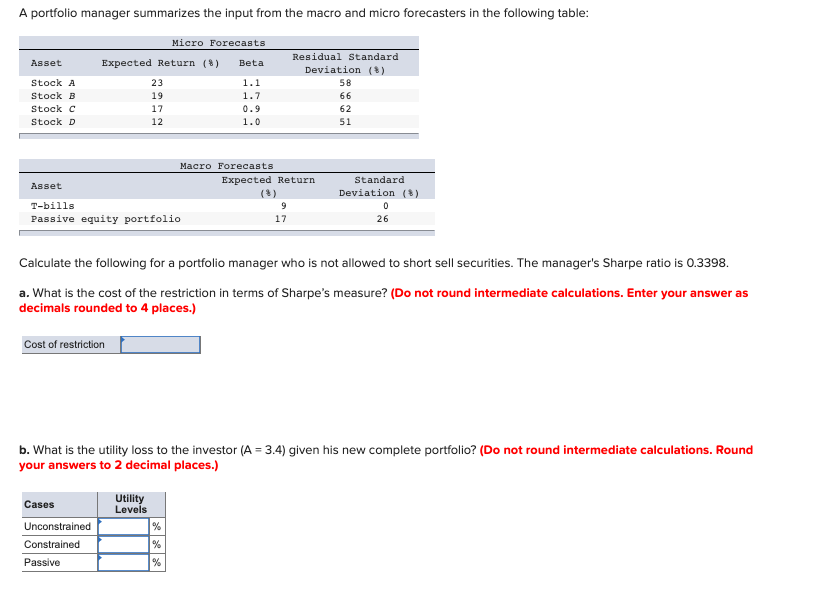

Question: A portfolio manager summarizes the input from the macro and micro forecasters in the following table: Residual standard Deviation (8) Asset Stock A Stock B

A portfolio manager summarizes the input from the macro and micro forecasters in the following table: Residual standard Deviation (8) Asset Stock A Stock B Stock C Stock D Micro Forecasts Expected Return (8) Beta 23 1.1 1.7 0.9 12 1.0 58 19 66 62 51 Macro Forecasts Expected Return Asset (3) T-bills Passive equity portfolio Standard Deviation (%) 17 26 Calculate the following for a portfolio manager who is not allowed to short sell securities. The manager's Sharpe ratio is 0.3398. a. What is the cost of the restriction in terms of Sharpe's measure? (Do not round intermediate calculations. Enter your answer as decimals rounded to 4 places.) Cost of restriction b. What is the utility loss to the investor (A = 3.4) given his new complete portfolio? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Cases Utility Levels Unconstrained Constrained Passive A portfolio manager summarizes the input from the macro and micro forecasters in the following table: Residual standard Deviation (8) Asset Stock A Stock B Stock C Stock D Micro Forecasts Expected Return (8) Beta 23 1.1 1.7 0.9 12 1.0 58 19 66 62 51 Macro Forecasts Expected Return Asset (3) T-bills Passive equity portfolio Standard Deviation (%) 17 26 Calculate the following for a portfolio manager who is not allowed to short sell securities. The manager's Sharpe ratio is 0.3398. a. What is the cost of the restriction in terms of Sharpe's measure? (Do not round intermediate calculations. Enter your answer as decimals rounded to 4 places.) Cost of restriction b. What is the utility loss to the investor (A = 3.4) given his new complete portfolio? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Cases Utility Levels Unconstrained Constrained Passive

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts