Question: A question on Financial Math. Please show step by step. Thank you so much!!! The following table shows the Macaulay duration and modified convexity of

A question on Financial Math.

Please show step by step.

Thank you so much!!!

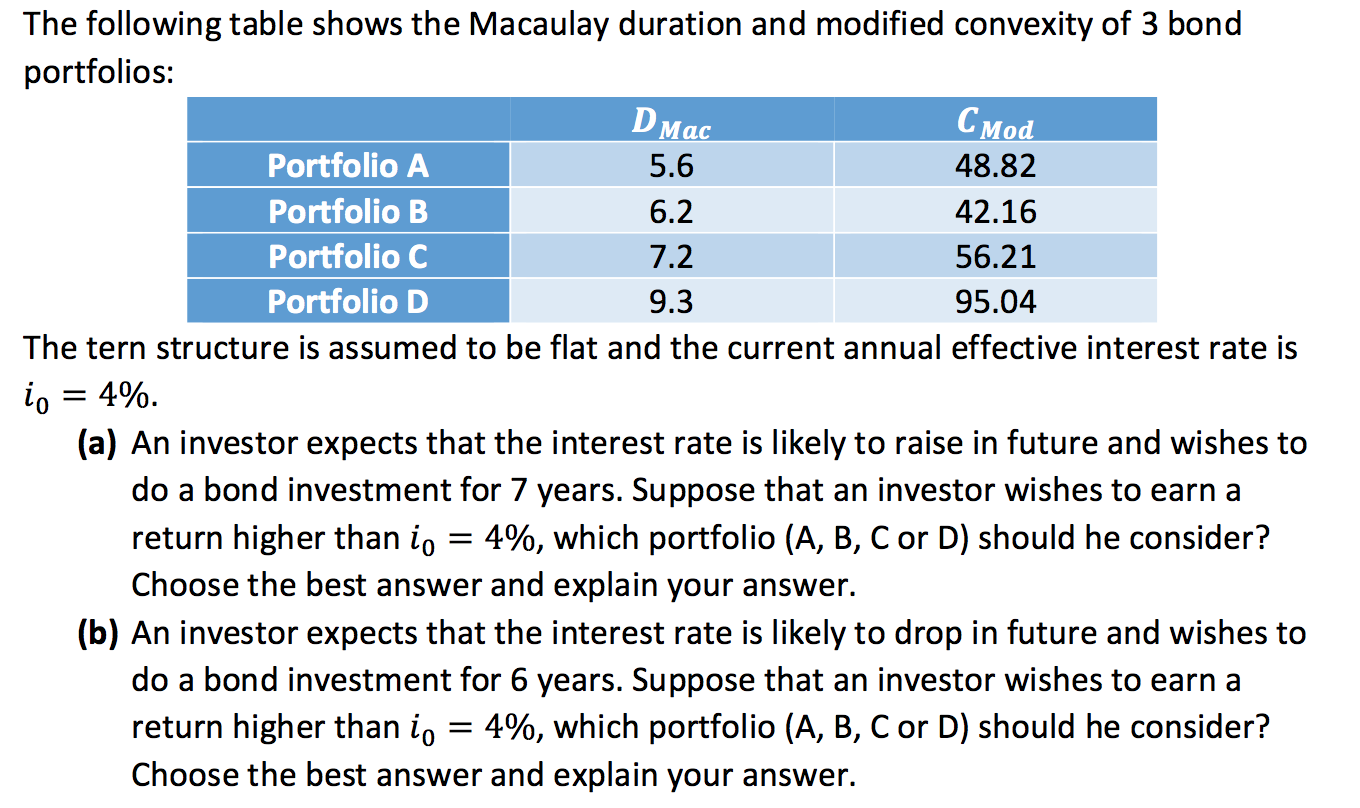

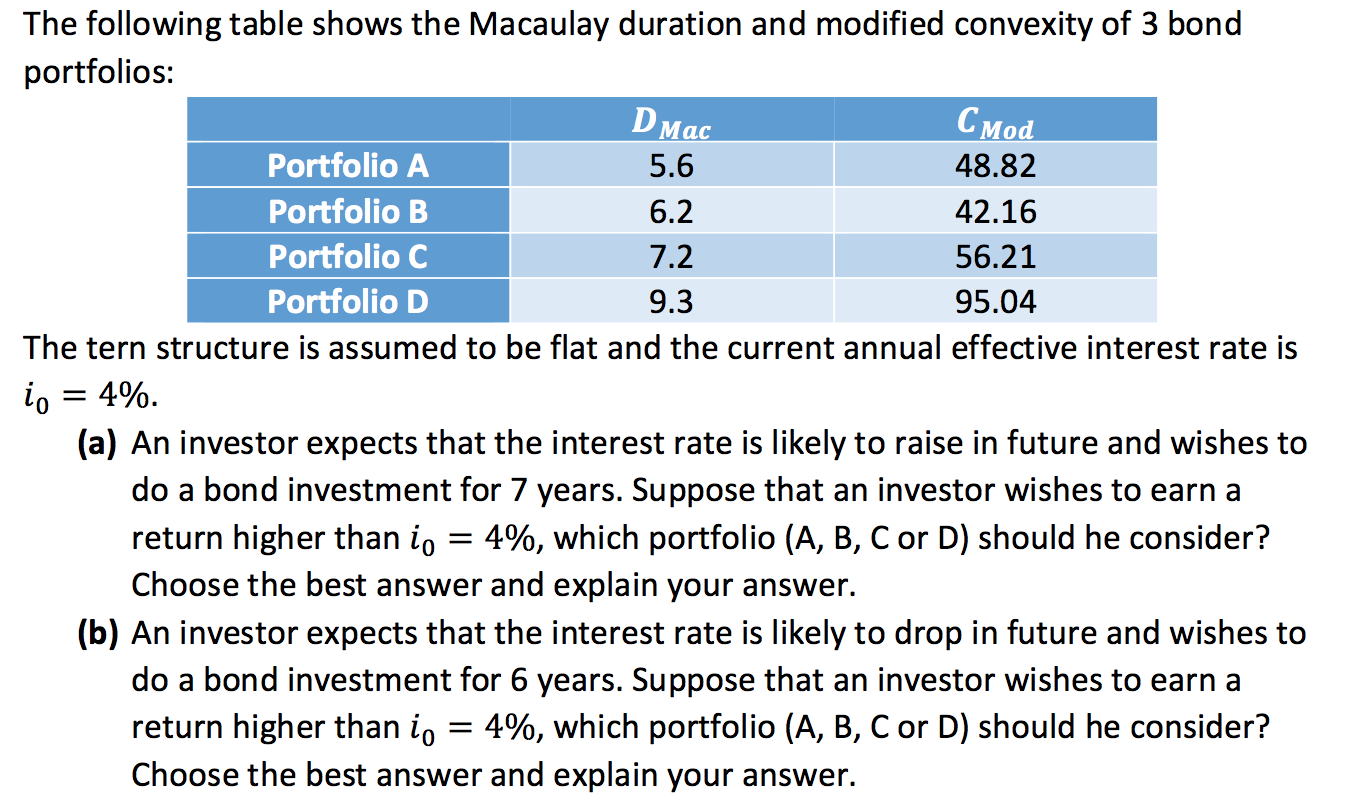

The following table shows the Macaulay duration and modified convexity of 3 bond portfolios: DMac CMod Portfolio A 5.6 48.82 Portfolio B 6.2 42.16 Portfolio C 7.2 56.21 Portfolio D 9.3 95.04 The tern structure is assumed to be flat and the current annual effective interest rate is to = 4%. (a) An investor expects that the interest rate is likely to raise in future and wishes to do a bond investment for 7 years. Suppose that an investor wishes to earn a return higher than i0 = 4%, which portfolio (A, B, C or D) should he consider? Choose the best answer and explain your answer. (b) An investor expects that the interest rate is likely to drop in future and wishes to do a bond investment for 6 years. Suppose that an investor wishes to earn a return higher than to = 4%, which portfolio (A, B, C or D) should he consider? Choose the best answer and explain your

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts