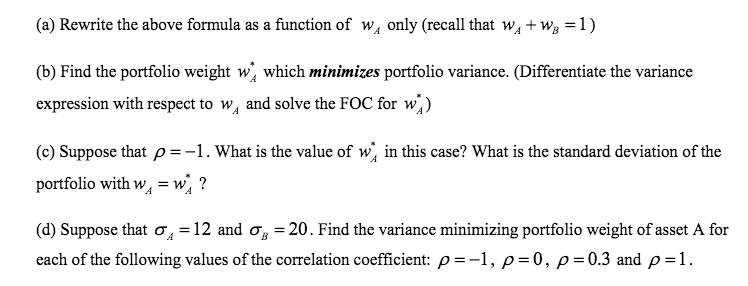

Question: (a) Rewrite the above formula as a function of w, only (recall that wtw, = 1) (b) Find the portfolio weight w which minimizes portfolio

(a) Rewrite the above formula as a function of w, only (recall that wtw, = 1) (b) Find the portfolio weight w which minimizes portfolio variance. (Differentiate the variance expression with respect to w and solve the FOC for w ) (c) Suppose that p =-1. What is the value of w, in this case? What is the standard deviation of the portfolio with w = w ? (d) Suppose that o =12 and o =20. Find the variance minimizing portfolio weight of asset A for each of the following values of the correlation coefficient: p =-1, p =0, p =0.3 and p =1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock