A stock price is currently $100. A call option on this stock with a strike price of

Fantastic news! We've Found the answer you've been seeking!

Question:

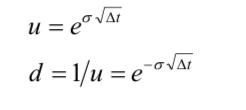

A stock price is currently $100. A call option on this stock with a strike price of $100 and one year to maturity costs $13.61. The continuous-time interest rate is 5%. By using a one-step binomial tree, estimate the expected volatility level (σ) for the stock. Assume that u and d are modeled as below.

( Excel's Goal Seek will help solving this and will be much appreciated to be posted to see how it has been used to solve this problem, thanks)

Expert Answer:

Related Book For

Posted Date: