Question: a) Suppose that zero rates with continuous compounding are as follows: Maturity (months) Rate (% per annum) 3 2.0 6 2.2 9 2.4 12 2.5

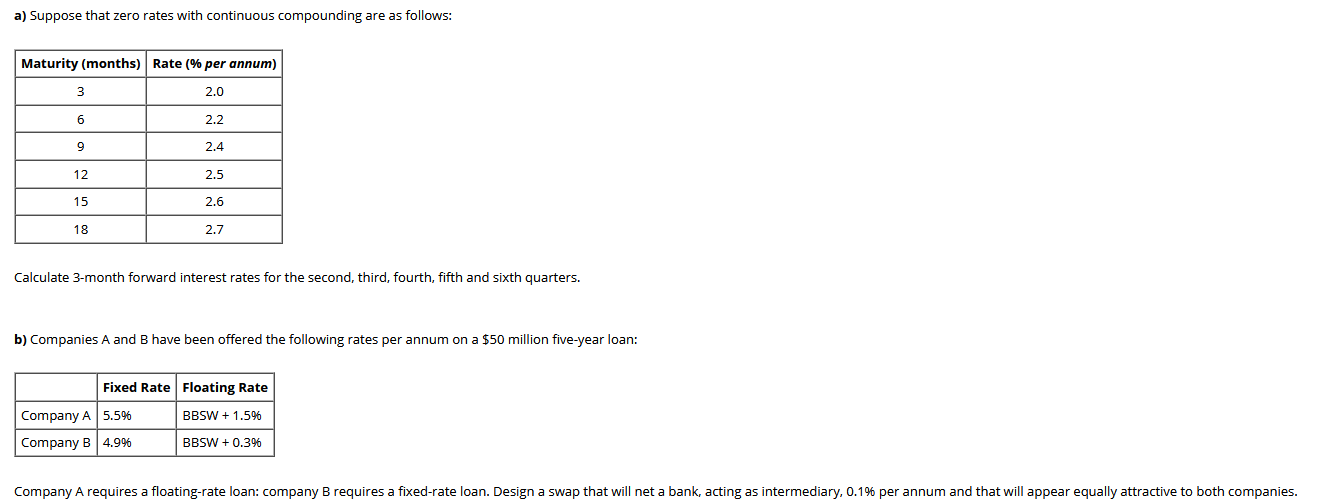

a) Suppose that zero rates with continuous compounding are as follows: Maturity (months) Rate (% per annum) 3 2.0 6 2.2 9 2.4 12 2.5 15 2.6 18 2.7 Calculate 3-month forward interest rates for the second, third, fourth, fifth and sixth quarters. b) Companies A and have been offered the following rates per annum on a $50 million five-year loan: Fixed Rate Floating Rate Company A 5.5% BBSW + 1.596 Company B 4.9% BBSW + 0.396 Company A requires a floating-rate loan: company B requires a fixed-rate loan. Design a swap that will net a bank, acting as intermediary, 0.196 per annum and that will appear equally attractive to both companies. a) Suppose that zero rates with continuous compounding are as follows: Maturity (months) Rate (% per annum) 3 2.0 6 2.2 9 2.4 12 2.5 15 2.6 18 2.7 Calculate 3-month forward interest rates for the second, third, fourth, fifth and sixth quarters. b) Companies A and have been offered the following rates per annum on a $50 million five-year loan: Fixed Rate Floating Rate Company A 5.5% BBSW + 1.596 Company B 4.9% BBSW + 0.396 Company A requires a floating-rate loan: company B requires a fixed-rate loan. Design a swap that will net a bank, acting as intermediary, 0.196 per annum and that will appear equally attractive to both companies

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts