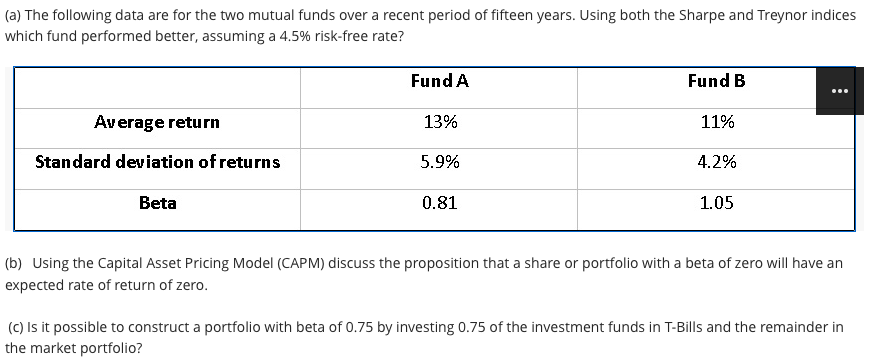

Question: (a) The following data are for the two mutual funds over a recent period of fifteen years. Using both the Sharpe and Treynor indices which

(a) The following data are for the two mutual funds over a recent period of fifteen years. Using both the Sharpe and Treynor indices which fund performed better, assuming a 4.5% risk-free rate? Fund A Fund B ... Average return 13% 11% Standard deviation of returns 5.9% 4.2% Beta 0.81 1.05 (b) Using the Capital Asset Pricing Model (CAPM) discuss the proposition that a share or portfolio with a beta of zero will have an expected rate of return of zero. (C) Is it possible to construct a portfolio with beta of 0.75 by investing 0.75 of the investment funds in T-Bills and the remainder in the market portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock