Question: A thoretical question on time seres, ARMA model, see below please 4. (a) Describe the following concepts: (i) strict stationarity, (ii) weak stationarity and (iii)

A thoretical question on time seres, ARMA model, see below please

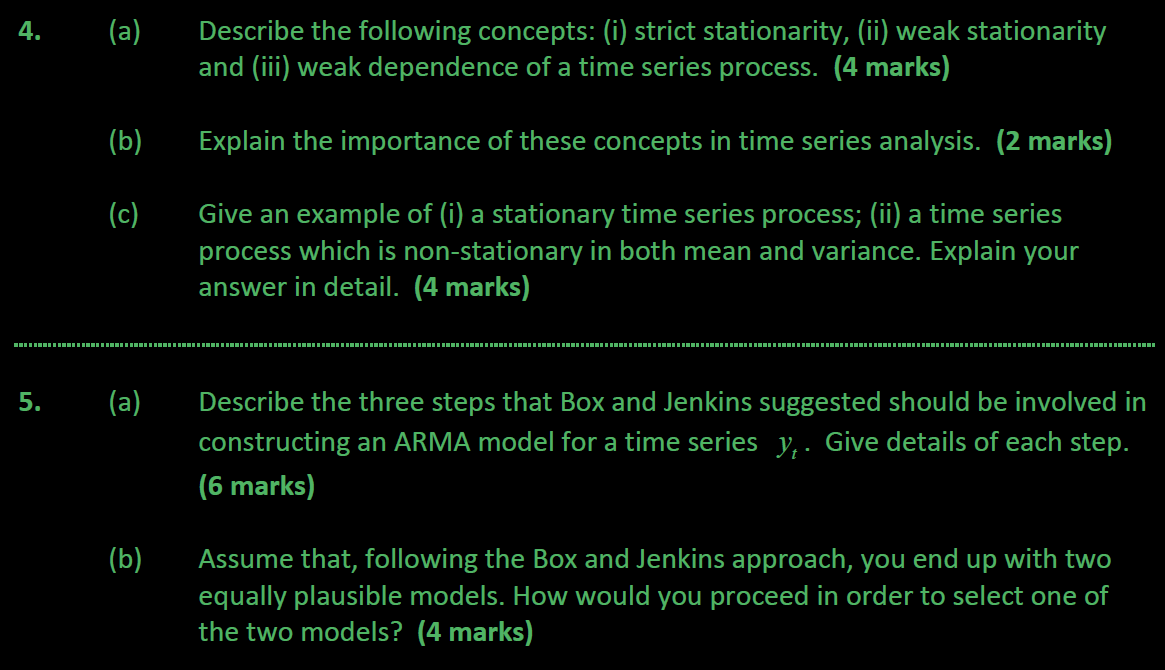

4. (a) Describe the following concepts: (i) strict stationarity, (ii) weak stationarity and (iii) weak dependence of a time series process. (4 marks) (b) Explain the importance of these concepts in time series analysis. (2 marks) (c) Give an example of (i) a stationary time series process; (ii) a time series process which is non-stationary in both mean and variance. Explain your answer in detail. (4 marks) 5. (a) Describe the three steps that Box and Jenkins suggested should be involved in constructing an ARMA model for a time series y . Give details of each step. (6 marks) (b) Assume that, following the Box and Jenkins approach, you end up with two equally plausible models. How would you proceed in order to select one of the two models? (4 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts