Question: a time series problem Consider the time series process: Xt = aX-ate+ Biet-2 + Bget-3 where er follows a Gaussian white noise process with variance

a time series problem

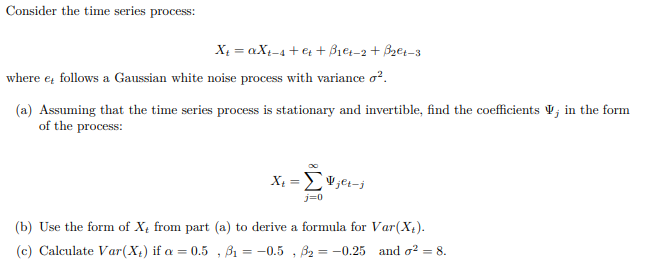

Consider the time series process: Xt = aX-ate+ Biet-2 + Bget-3 where er follows a Gaussian white noise process with variance o'. (a) Assuming that the time series process is stationary and invertible, find the coefficients V, in the form of the process: X = >vjet-i j=0 (b) Use the form of X, from part (a) to derive a formula for Var(X.). (c) Calculate Var(X) if a = 0.5 , 81 = -0.5 , 82 = -0.25 and o' = 8

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock