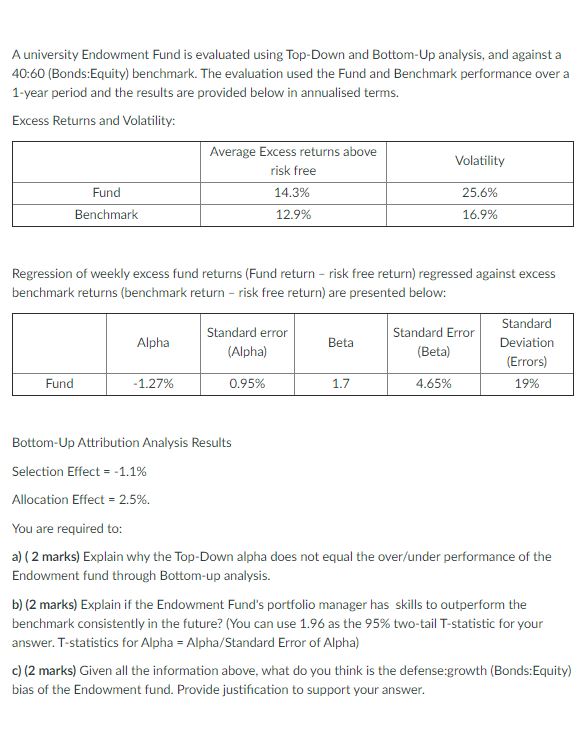

Question: A university Endowment Fund is evaluated using Top-Down and Bottom-Up analysis, and against a 40:60 (Bonds:Equity) benchmark. The evaluation used the Fund and Benchmark performance

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock