Question: (a) What is the Black-Scholes Partial Differential Equation for the price f(t, St) at time t of a European derivative security on a stock with

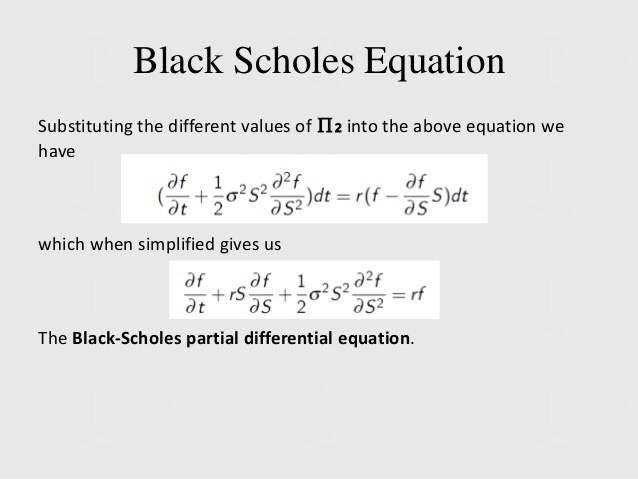

(a) What is the Black-Scholes Partial Differential Equation for the price f(t, St) at time t of a European derivative security on a stock with price St? Specify the meaning of the terms or symbols in the equation. (b) Note that the Black-Scholes Partial Differential Equation does not specify whether the derivative is a call option, a put option, or some other derivative. How do you incorporate the derivative payoff when using Black-Scholes PDE to price a derivative? Black Scholes Equation Substituting the different values of II z into the above equation we have to? 2 4 )dt = rf - Side which when simplified gives us af af 1 de tract-02 S2 Sto?5202 2S2 = rf The Black-Scholes partial differential equation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts