Interpreting Non-GAAP Disclosures The Boeing Company reported the following information in its MD&A section of a...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

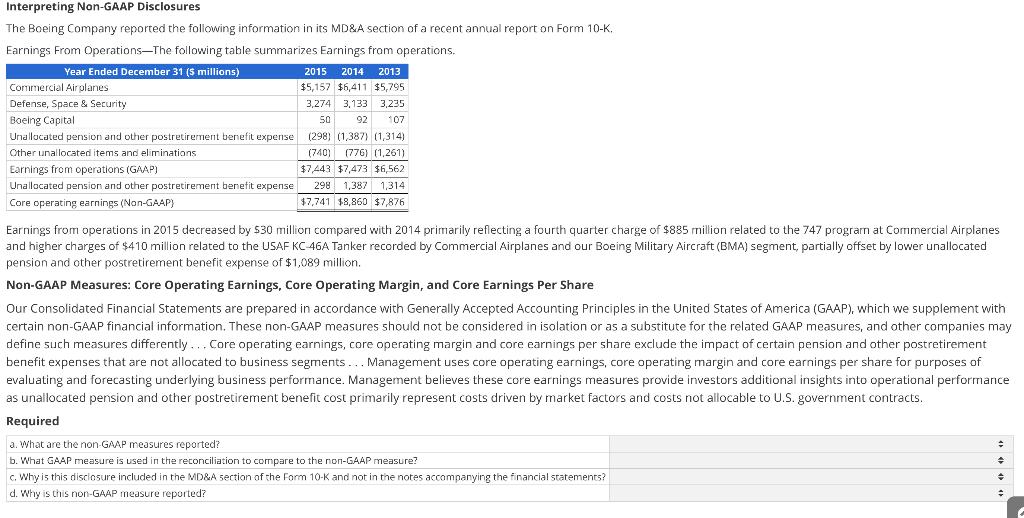

Interpreting Non-GAAP Disclosures The Boeing Company reported the following information in its MD&A section of a recent annual report on Form 10-K. Earnings From Operations-The following table summarizes Earnings from operations. Year Ended December 31 ($ millions) Commercial Airplanes Defense, Space & Security Boeing Capital Unallocated pension and other postretirement benefit expense Other unallocated items and eliminations. Earnings from operations (GAAP) Unallocated pension and other postretirement benefit expense Core operating earnings (Non-GAAP) 2015 2014 2013 $5,157 $6,411 $5,795 3,274 3,133 3,235 50 92 107 (298) (1,387) (1,314) (740) (776) (1,261) $7,443 $7,473 $6,562 298 1,387 1,314 $7,741 $8,860 $7,876 Earnings from operations in 2015 decreased by $30 million compared with 2014 primarily reflecting a fourth quarter charge of $885 million related to the 747 program at Commercial Airplanes. and higher charges of $410 million related to the USAF KC-46A Tanker recorded by Commercial Airplanes and our Boeing Military Aircraft (BMA) segment, partially offset by lower unallocated pension and other postretirement benefit expense of $1,089 million. Non-GAAP Measures: Core Operating Earnings, Core Operating Margin, and Core Earnings Per Share Our Consolidated Financial Statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (GAAP), which we supplement with certain non-GAAP financial information. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently... Core operating earnings, core operating margin and core earnings per share exclude the impact of certain pension and other postretirement benefit expenses that are not allocated to business segments... Management uses core operating earnings, core operating margin and core earnings per share for purposes of evaluating and forecasting underlying business performance. Management believes these core earnings measures provide investors additional insights into operational performance as unallocated pension and other postretirement benefit cost primarily represent costs driven by market factors and costs not allocable to U.S. government contracts. Required a. What are the non-GAAP measures reported? b. What GAAP measure is used in the reconciliation to compare to the non-GAAP measure? c. Why is this disclosure included in the MD&A section of the Form 10-K and not in the notes accompanying the financial statements? d. Why is this non-GAAP measure reported? = + ÷ Non-GAAP Measures: Core Operating Earnings, Core Operating Margin, and Core Earnings Per Share Our Consolidated Financial Statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (GAAP), which we supplement with certain non-GAAP financial information. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently... Core operating earnings, core operating margin and core earnings per share exclude the impact of certain pension and other postretirement benefit expenses that are not allocated to business segments... Management uses core operating ea evaluating and forecasting underlying business performance. Management believes these core earnin as unallocated pension and other postretirement benefit cost primarily represent costs driven by mar Required a. What are the non-GAAP measures reported? b. What GAAP measure is used in the reconciliation to compare to the non-GAAP measure? c. Why is this disclosure included in the MD&A section of the Form 10-K and not in the notes accompanying the financial stat d. Why is this non-GAAP measure reported? Net assets Net income Non-GAAP measures are a required component of the MD&A section Non-GAAP measures may be explained in the notes to financial statements Non-GAAP measures must be explained in the notes to financial statements The reporting affirms the computation of a measure widely and consistently used across companies The reporting of non-GAAP measures is a required industry practice Total assets Core operating earnings, core operating margin, core earnings per share Disclosure is not based on a GAAP standard Earnings from operations Voluntary decision made by management Interpreting Non-GAAP Disclosures The Boeing Company reported the following information in its MD&A section of a recent annual report on Form 10-K. Earnings From Operations-The following table summarizes Earnings from operations. Year Ended December 31 ($ millions) Commercial Airplanes Defense, Space & Security Boeing Capital Unallocated pension and other postretirement benefit expense Other unallocated items and eliminations. Earnings from operations (GAAP) Unallocated pension and other postretirement benefit expense Core operating earnings (Non-GAAP) 2015 2014 2013 $5,157 $6,411 $5,795 3,274 3,133 3,235 50 92 107 (298) (1,387) (1,314) (740) (776) (1,261) $7,443 $7,473 $6,562 298 1,387 1,314 $7,741 $8,860 $7,876 Earnings from operations in 2015 decreased by $30 million compared with 2014 primarily reflecting a fourth quarter charge of $885 million related to the 747 program at Commercial Airplanes. and higher charges of $410 million related to the USAF KC-46A Tanker recorded by Commercial Airplanes and our Boeing Military Aircraft (BMA) segment, partially offset by lower unallocated pension and other postretirement benefit expense of $1,089 million. Non-GAAP Measures: Core Operating Earnings, Core Operating Margin, and Core Earnings Per Share Our Consolidated Financial Statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (GAAP), which we supplement with certain non-GAAP financial information. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently... Core operating earnings, core operating margin and core earnings per share exclude the impact of certain pension and other postretirement benefit expenses that are not allocated to business segments... Management uses core operating earnings, core operating margin and core earnings per share for purposes of evaluating and forecasting underlying business performance. Management believes these core earnings measures provide investors additional insights into operational performance as unallocated pension and other postretirement benefit cost primarily represent costs driven by market factors and costs not allocable to U.S. government contracts. Required a. What are the non-GAAP measures reported? b. What GAAP measure is used in the reconciliation to compare to the non-GAAP measure? c. Why is this disclosure included in the MD&A section of the Form 10-K and not in the notes accompanying the financial statements? d. Why is this non-GAAP measure reported? = + ÷ Non-GAAP Measures: Core Operating Earnings, Core Operating Margin, and Core Earnings Per Share Our Consolidated Financial Statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (GAAP), which we supplement with certain non-GAAP financial information. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently... Core operating earnings, core operating margin and core earnings per share exclude the impact of certain pension and other postretirement benefit expenses that are not allocated to business segments... Management uses core operating ea evaluating and forecasting underlying business performance. Management believes these core earnin as unallocated pension and other postretirement benefit cost primarily represent costs driven by mar Required a. What are the non-GAAP measures reported? b. What GAAP measure is used in the reconciliation to compare to the non-GAAP measure? c. Why is this disclosure included in the MD&A section of the Form 10-K and not in the notes accompanying the financial stat d. Why is this non-GAAP measure reported? Net assets Net income Non-GAAP measures are a required component of the MD&A section Non-GAAP measures may be explained in the notes to financial statements Non-GAAP measures must be explained in the notes to financial statements The reporting affirms the computation of a measure widely and consistently used across companies The reporting of non-GAAP measures is a required industry practice Total assets Core operating earnings, core operating margin, core earnings per share Disclosure is not based on a GAAP standard Earnings from operations Voluntary decision made by management

Expert Answer:

Answer rating: 100% (QA)

a The nonGAAP measures reported are core operating earnings core operating margin and core earnings ... View the full answer

Related Book For

Corporate Financial Accounting

ISBN: 978-1133952411

12th edition

Authors: Carl S. Warren, James M. Reeve, Jonathan E. Duchac

Posted Date:

Students also viewed these accounting questions

-

Earnings per Share Disclosure Extreme Company reported the following information about its stock on its December 31, 2016, balance sheet: Preferred stock, $2 par value, 5% cumulative, 300,000 shares...

-

The Abercrombie Supply Company reported the following information for 2014. Prepare a common-size income statement for the year ended June 30, 2014. Abercrombie Supply Company Income Statement for...

-

Hometown Supply Company reported the following information in its comparative financial statements for the fiscal year ended January 31, 2018: Requirements 1. Compute the net profit margin ratio for...

-

Solve the equation symbolically. Then solve the related inequality. 1 - X

-

Winning team data were collected for teams in different sports, with the results given in the accompanying table. Use a 0.10 level of significance to test the claim that home/visitor wins are...

-

general manager for CRU Computer Rentals, was studying the sales and financial figures for the first quarter of the year and was at a loss to explain the numbers. After a period of declining sales...

-

Refer to Problem 3.1. Data From Problem 3.1 Consider the National Football League data in Table B.1. a. Find a $95 % \mathrm{CI}$ on $\beta_{7}$. b. Find a $95 %$ CI on the mean number of games won...

-

Multiple Choice Questions 1. Candy Corp. is a C corporation that began operations in year 1. Candy Corp.'s year 1 through year 3 taxable earnings and profits (E & P) are computed as follows. Year E &...

-

The technology company, Samsung, is considering to revamp an old tablet product of theirs and would like for it to make a big impression against other competitors in this day and age. -What branding...

-

Elizabeth Burke has asked you to do some preliminary analysis of the data in the Performance Lawn Equipment database. First, she would like you to edit the worksheets Dealer Satisfaction and End-...

-

Prepare Journal Entry ? Accounts Cash Accounts Receivable Supplies Equipment Accumulated Depreciation Salaries Payable Common Stock Retained Earnings Totals Debits Credits $ 13,500 6,700 2,700 16,500...

-

Troy Barnes, P . Eng, is evaluating a proposal for new equipment that will generate process improvements for the production of Air Conditioning Units at his company, Greendale AC Ltd . The initial...

-

You have forecast the free cash flows to the firm for Permelac Inc., a young and growing company, for the next ten years. You estimate that the cash flows will be negative for the first six years and...

-

Two particles with masses m are placed at the (0, a) and (0, -a) points on y-axis. Find the magnitude of gravitational acceleration (g) at the point P(x,0) on x-axis. (a) (b) 0 (d) (e) 4Gmx (x+a)/2...

-

6. The four capacitors in the combination illustrated below each has a capacitance C. If all the capacitors are then filled with a dielectric having a dielectric constant of 2, what is the new total...

-

A 0.40 kg object undergoing simple harmonic motion has a the period of the oscillation? (a) 0.8 N/m, 0.5 s (b) 1.6 N/m, 7 s (c) 1.4 N/m, 2x s = -3 m/s2 when r=0.75 m. What is the spring constant and...

-

A steel rotating-beam test specimen has an ultimate strength of 1100 MPa. Estimate the fatigue strength corresponding to a life of 141313 cycles of stress reversal. Give your answer to 3 significant...

-

Write a while loop that uses an explicit iterator to accomplish the same thing as Exercise 7.3. Exercise 7.3. Write a for-each loop that calls the addInterest method on each BankAccount object in a...

-

Assume the same facts as in Exercise 9-25, except that the book value of the press traded in is $108,500. (a) What is the amount of cash given? (b) What is the gain or loss on the exchange? In...

-

The unadjusted trial balance of La Mesa Laundry at August 31, 2014, the end of the current fiscal year, is shown below. The data needed to determine year-end adjustments are as follows: a. Wages...

-

The supplies account had a beginning balance of $1,975 and was debited for $4,125 for supplies purchased during the year. Journalize the adjusting entry required at the end of the year assuming the...

-

Indonesia produces about 60 percent of the worlds palm oil. Palm oil is used in the production of shampoo, ice cream, and chocolate. Assume that Switzerland does not produce palm oil but companies in...

-

An article in the Wall Street Journal stated that Chinas treatment of American know-how has been a central issue to U.S.-China trade tensions over the past five years. a. What does the article mean...

-

James Halperin, co-chair of Heritage Auctions, was interviewed about his experiences auctioning rare coins. Noting that when the auction house first opened in the 1970s, I used to proofread every...

Study smarter with the SolutionInn App