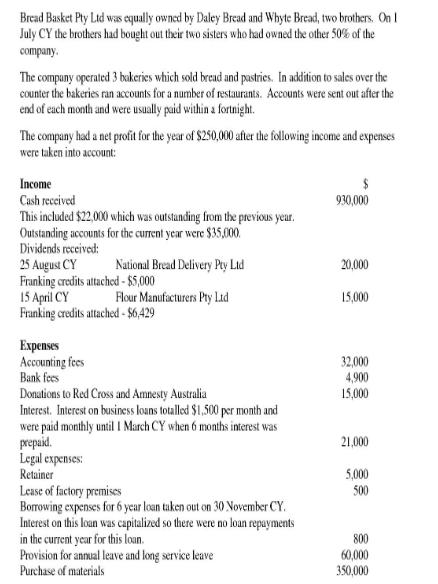

Bread Basket Pty Ltd was equally owned by Daley Bread and Whyte Bread, two brothers. On...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

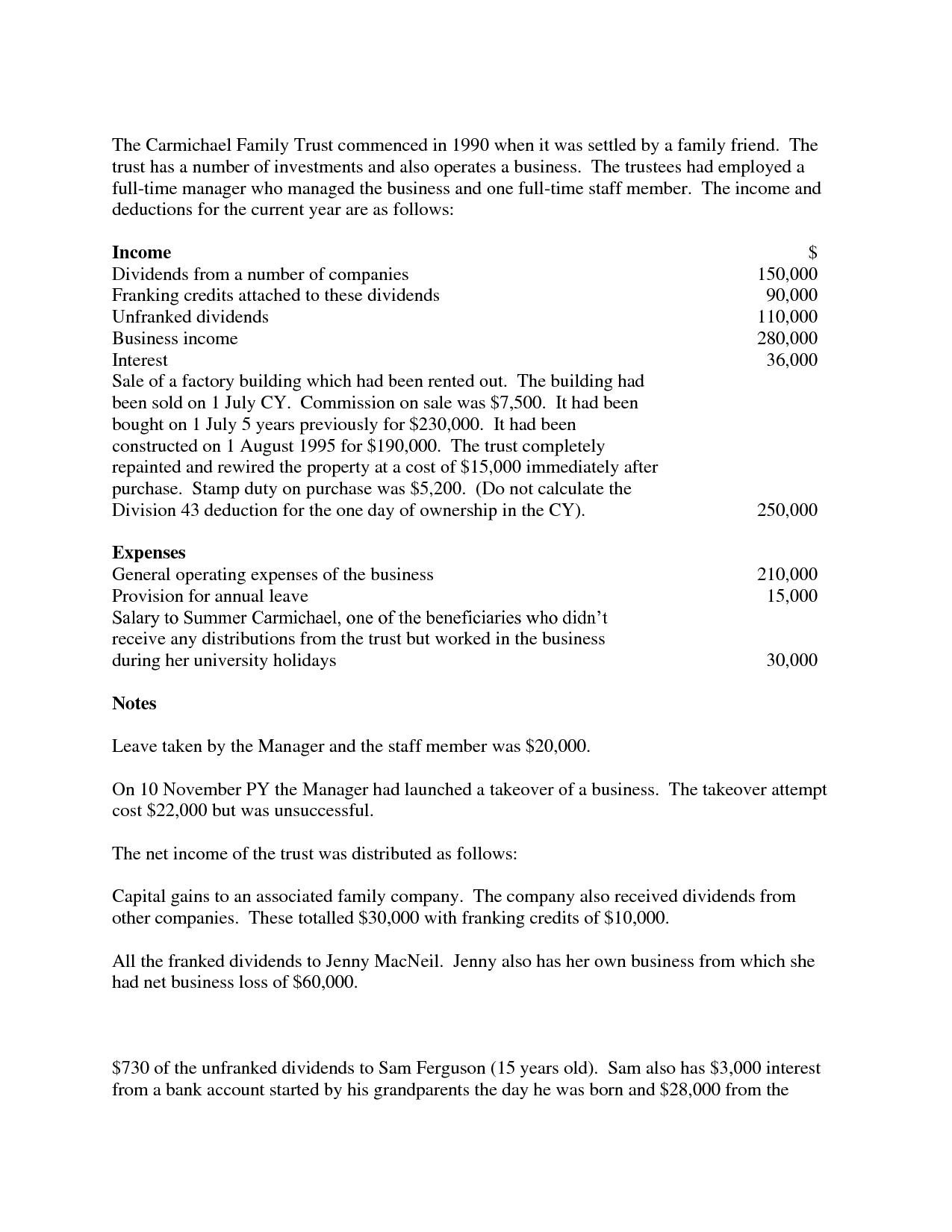

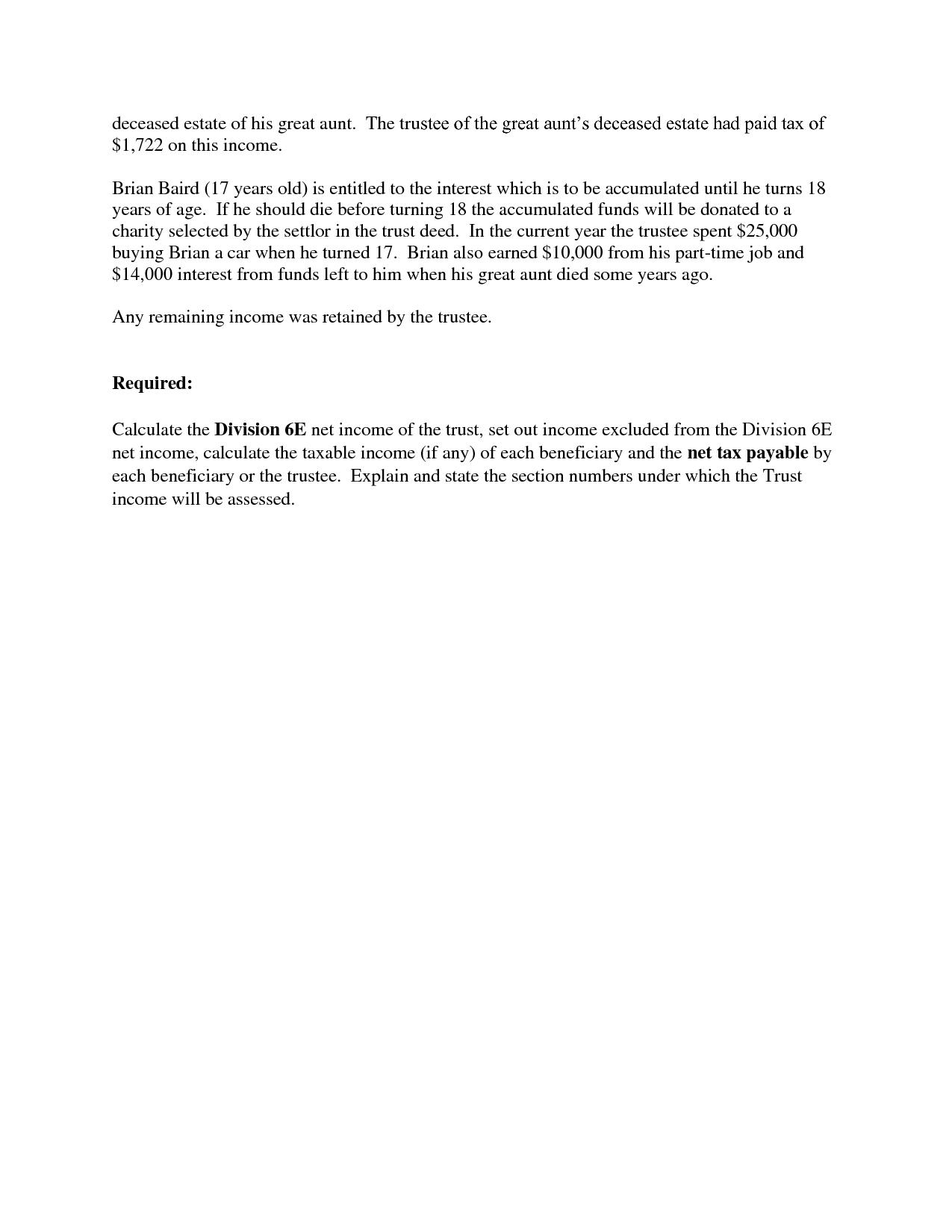

Bread Basket Pty Ltd was equally owned by Daley Bread and Whyte Bread, two brothers. On I July CY the brothers had bought out their two sisters who had owned the other 50% of the company. The company operated 3 bakeries which sold bread and pastries. In addition to sales over the counter the bakeries ran accounts for a number of restaurants. Accounts were sent out after the end of each month and were usually paid within a fortnight. The company had a net profit for the year of $250,000 after the following income and expenses were taken into account: Income Cash received This included $22,000 which was outstanding from the previous year. Outstanding accounts for the current year were $35,000. Dividends received: 25 August CY Franking credits attached - $5,000 15 April CY Franking credits attached - $6,429 National Bread Delivery Pty Ltd Expenses Accounting fees Bank fees Flour Manufacturers Pty Ltd Donations to Red Cross and Amnesty Australia Interest. Interest on business loans totalled $1,500 per month and were paid monthly until I March CY when 6 months interest was prepaid. Legal expenses: Retainer Lease of factory premises Borrowing expenses for 6 year loan taken out on 30 November CY. Interest on this loan was capitalized so there were no loan repayments in the current year for this loan. Provision for annual leave and long service leave Purchase of materials 930,000 20,000 15,000 32,000 4,900 15,000 21,000 5,000 500 800 60,000 350,000 Travelling expenses: Daley Bread traveled to a Small Business Conference in Sydney. His wife traveled with him and attended some of the social functions organised by the conference organisers. Daley's costs were 70% of the total expenses paid by the company. The remainder related to his wife. Wages to staff Superannuation for staff Notes: Actual leave taken by staff was $93,000. Purchase of new office on 1 June CY for $340,000. The building had been constructed on 1 April 2003 at a cost of $100,000. Write off of bad debt of $2,800 on 15 June CY. The debt arose from sales to a restaurant in the previous year. The restaurant had gone out of business and there was going to be no return to unsecured creditors. 5,100 500,000 45,000 The following PAYG (Instalments) or refunds received were paid or received during the year: $ 28 July CY 28 October CY 30 November CY 28 February CY 28 April CY 28 July FY 4th instalment of PY tax 1st instalment of CY tax refund of PY tax 2nd instalment of CY tax 3rd instalment of CY tax 4th instalment of CY tax 3,200 15,800 840 14,200 16,800 23,000 The company paid two dividends during the year. The first totalled $35,000 and was franked to 100%. It was paid on 1 July CY. The second dividend was paid on 1 December CY. The dividend totalled $60,000 and was franked to 30%. The balance in the franking account at 30 June PY was a debit of $2,000 which was paid on 28 July CY. Required: Using the reconciliation method, calculate the taxable income and the net tax payable of the company for the year ended 30 June CY assuming the company wished to minimise it's taxable income but did not wish to use pooling for depreciation purposes and did not wish to use SBE elections. Treat them as a non BRE Set out the franking account for the company for the current year including any franking additional tax or franking deficit tax which may be payable. Question 2 The Carmichael Family Trust commenced in 1990 when it was settled by a family friend. The trust has a number of investments and also operates a business. The trustees had employed a full-time manager who managed the business and one full-time staff member. The income and deductions for the current year are as follows: Income Dividends from a number of companies Franking credits attached to these dividends Unfranked dividends Business income Interest Sale of a factory building which had been rented out. The building had been sold on 1 July CY. Commission on sale was $7,500. It had been bought on 1 July 5 years previously for $230,000. It had been constructed on 1 August 1995 for $190,000. The trust completely repainted and rewired the property at a cost of $15,000 immediately after purchase. Stamp duty on purchase was $5,200. (Do not calculate the Division 43 deduction for the one day of ownership in the CY). Expenses General operating expenses of the business Provision for annual leave Salary to Summer Carmichael, one of the beneficiaries who didn't receive any distributions from the trust but worked in the business during her university holidays Notes 150,000 90,000 110,000 280,000 36,000 The net income of the trust was distributed as follows: 250,000 210,000 15,000 30,000 Leave taken by the Manager and the staff member was $20,000. On 10 November PY the Manager had launched a takeover of a business. The takeover attempt cost $22,000 but was unsuccessful. Capital gains to an associated family company. The company also received dividends from other companies. These totalled $30,000 with franking credits of $10,000. All the franked dividends to Jenny MacNeil. Jenny also her own business from which had net business loss of $60,000. $730 of the unfranked dividends to Sam Ferguson (15 years old). Sam also has $3,000 interest from a bank account started by his grandparents the day he was born and $28,000 from the deceased estate of his great aunt. The trustee of the great aunt's deceased estate had paid tax of $1,722 on this income. Brian Baird (17 years old) is entitled to the interest which is to be accumulated until he turns 18 years of age. If he should die before turning 18 the accumulated funds will be donated to a charity selected by the settlor in the trust deed. In the current year the trustee spent $25,000 buying Brian a car when he turned 17. Brian also earned $10,000 from his part-time job and $14,000 interest from funds left to him when his great aunt died some years ago. Any remaining income was retained by the trustee. Required: Calculate the Division 6E net income of the trust, set out income excluded from the Division 6E net income, calculate the taxable income (if any) of each beneficiary and the net tax payable by each beneficiary or the trustee. Explain and state the section numbers under which the Trust income will be assessed. Bread Basket Pty Ltd was equally owned by Daley Bread and Whyte Bread, two brothers. On I July CY the brothers had bought out their two sisters who had owned the other 50% of the company. The company operated 3 bakeries which sold bread and pastries. In addition to sales over the counter the bakeries ran accounts for a number of restaurants. Accounts were sent out after the end of each month and were usually paid within a fortnight. The company had a net profit for the year of $250,000 after the following income and expenses were taken into account: Income Cash received This included $22,000 which was outstanding from the previous year. Outstanding accounts for the current year were $35,000. Dividends received: 25 August CY Franking credits attached - $5,000 15 April CY Franking credits attached - $6,429 National Bread Delivery Pty Ltd Expenses Accounting fees Bank fees Flour Manufacturers Pty Ltd Donations to Red Cross and Amnesty Australia Interest. Interest on business loans totalled $1,500 per month and were paid monthly until I March CY when 6 months interest was prepaid. Legal expenses: Retainer Lease of factory premises Borrowing expenses for 6 year loan taken out on 30 November CY. Interest on this loan was capitalized so there were no loan repayments in the current year for this loan. Provision for annual leave and long service leave Purchase of materials 930,000 20,000 15,000 32,000 4,900 15,000 21,000 5,000 500 800 60,000 350,000 Travelling expenses: Daley Bread traveled to a Small Business Conference in Sydney. His wife traveled with him and attended some of the social functions organised by the conference organisers. Daley's costs were 70% of the total expenses paid by the company. The remainder related to his wife. Wages to staff Superannuation for staff Notes: Actual leave taken by staff was $93,000. Purchase of new office on 1 June CY for $340,000. The building had been constructed on 1 April 2003 at a cost of $100,000. Write off of bad debt of $2,800 on 15 June CY. The debt arose from sales to a restaurant in the previous year. The restaurant had gone out of business and there was going to be no return to unsecured creditors. 5,100 500,000 45,000 The following PAYG (Instalments) or refunds received were paid or received during the year: $ 28 July CY 28 October CY 30 November CY 28 February CY 28 April CY 28 July FY 4th instalment of PY tax 1st instalment of CY tax refund of PY tax 2nd instalment of CY tax 3rd instalment of CY tax 4th instalment of CY tax 3,200 15,800 840 14,200 16,800 23,000 The company paid two dividends during the year. The first totalled $35,000 and was franked to 100%. It was paid on 1 July CY. The second dividend was paid on 1 December CY. The dividend totalled $60,000 and was franked to 30%. The balance in the franking account at 30 June PY was a debit of $2,000 which was paid on 28 July CY. Required: Using the reconciliation method, calculate the taxable income and the net tax payable of the company for the year ended 30 June CY assuming the company wished to minimise it's taxable income but did not wish to use pooling for depreciation purposes and did not wish to use SBE elections. Treat them as a non BRE Set out the franking account for the company for the current year including any franking additional tax or franking deficit tax which may be payable. Question 2 The Carmichael Family Trust commenced in 1990 when it was settled by a family friend. The trust has a number of investments and also operates a business. The trustees had employed a full-time manager who managed the business and one full-time staff member. The income and deductions for the current year are as follows: Income Dividends from a number of companies Franking credits attached to these dividends Unfranked dividends Business income Interest Sale of a factory building which had been rented out. The building had been sold on 1 July CY. Commission on sale was $7,500. It had been bought on 1 July 5 years previously for $230,000. It had been constructed on 1 August 1995 for $190,000. The trust completely repainted and rewired the property at a cost of $15,000 immediately after purchase. Stamp duty on purchase was $5,200. (Do not calculate the Division 43 deduction for the one day of ownership in the CY). Expenses General operating expenses of the business Provision for annual leave Salary to Summer Carmichael, one of the beneficiaries who didn't receive any distributions from the trust but worked in the business during her university holidays Notes 150,000 90,000 110,000 280,000 36,000 The net income of the trust was distributed as follows: 250,000 210,000 15,000 30,000 Leave taken by the Manager and the staff member was $20,000. On 10 November PY the Manager had launched a takeover of a business. The takeover attempt cost $22,000 but was unsuccessful. Capital gains to an associated family company. The company also received dividends from other companies. These totalled $30,000 with franking credits of $10,000. All the franked dividends to Jenny MacNeil. Jenny also her own business from which had net business loss of $60,000. $730 of the unfranked dividends to Sam Ferguson (15 years old). Sam also has $3,000 interest from a bank account started by his grandparents the day he was born and $28,000 from the deceased estate of his great aunt. The trustee of the great aunt's deceased estate had paid tax of $1,722 on this income. Brian Baird (17 years old) is entitled to the interest which is to be accumulated until he turns 18 years of age. If he should die before turning 18 the accumulated funds will be donated to a charity selected by the settlor in the trust deed. In the current year the trustee spent $25,000 buying Brian a car when he turned 17. Brian also earned $10,000 from his part-time job and $14,000 interest from funds left to him when his great aunt died some years ago. Any remaining income was retained by the trustee. Required: Calculate the Division 6E net income of the trust, set out income excluded from the Division 6E net income, calculate the taxable income (if any) of each beneficiary and the net tax payable by each beneficiary or the trustee. Explain and state the section numbers under which the Trust income will be assessed.

Expert Answer:

Answer rating: 100% (QA)

To calculate the taxable income and net tax payable for Bread Basket Pty Ltd we need to reconcile th... View the full answer

Related Book For

Financial Accounting Tools for business decision making

ISBN: 978-0470534779

6th Edition

Authors: Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso

Posted Date:

Students also viewed these accounting questions

-

A business makes a allowance for doubtful accounts equal to 0.05 of its account receivables. At 30 April 2020 the allowance for doubtful accounts was $850 At 30 April 2021 the net account receivable...

-

6. On January 1, Puckett Company paid $1.6 million for 50,000 shares of Harrison's voting com- mon stock, which represents a 40 percent investment. No allocation to goodwill or other spe- cific...

-

Computation of selected ratios. The following data is given: December 31, 2015 2014 Cash$ 66,000 $50,000 Accounts receivable (net) 90,000 60,000 Inventories 90,000 110,000 Plant assets (net) 383,000...

-

In the game of roulette, a gambler who wins the bet receives $36 for every dollar she or he bet. A gambler who does not win receives nothing. If the gambler bets $1, what is the expected value of the...

-

A division reports divisional margin/profit of $80 000, residual income of $20 000 and an investment for the period of $800 000. What is the minimum return being required by management?

-

In Exercises 716, prove using the IVT. For all integers n, sinnx = cos x for some x [0, ].

-

A four cylinder, four stroke spark ignition engine has bore of \(80 \mathrm{~mm}\), stroke of \(80 \mathrm{~mm}\), and compression ratio of 8 . Calculate cubic capacity of engine and clearance volume...

-

You are auditing a bank, and someone provides you with an anonymous tip that an employee is embezzling money from the bank. You decide to investigate the allegation. Your interviews with other bank...

-

A company has just announced a dividend of $0.80 for this year and $0.835 for the next year. Dividends are expected to grow at a constant rate indefinitely. What is the current stock price if the...

-

Using the trial balance provided above, prepare an income statement and statement of changes in equity for the first year ended July 31, 2017, and a balance sheet at July 31, 2017. Analysis...

-

Solve the boundary-value problem by method of separation of variables: Su +39 Sx dy 2u, given u (x, 0) = 2e 2.x + 5e 4r

-

Koala Pty Ltd makes premium fishing rods and sells them to fishing retailers around Australia. Their products are in such high demand that Koala Pty Ltd sells everything they make (that is, they have...

-

7. In each of the following scenarios, a through d, determine whether the following is a microeconomic or macroeconomic issue and WHY. a. Dell computers announces that it will raise the price of its...

-

All of us are very familiar with chained food restaurants like KFC, McDonald and Subway. Compare decision-making in certain conditions and decision-making in uncertain conditionsthat occur in the one...

-

Discuss the following: a) b) c) The usefulness of models in managerial decision-making within firms. (5 marks) Process of theory formulation/model building (using an example of a theory/model known...

-

Thunderduck Shoes provides shoe shining and repair services to customers. For the year which ended Dec 31, the company reports the following amounts: Account Amount Account Amount Rent Expense 22,400...

-

1-3. In the steam return pipe failure described in Section 1.2.2, what are some of the costs which may result from this and similar failures?

-

How do individual companies respond to economic forces throughout the globe? One way to explore this is to see how well rates of return for stock of individual companies can be explained by stock...

-

Ndon Company reported net income of $157,000. It reported depreciation expense of $12,000 and accumulated depreciation of $47,000. Amortization expense was $8,000. Ndon purchased new equipment during...

-

This information is for OBrien Corporation for the year ended December 31, 2012. Cash received from lenders ..... $20,000 Cash received from customers ... 50,000 Cash paid for new equipment .......

-

Trattner Company had a beginning inventory on January 1 of 100 units of Product SXL at a cost of $20 per unit. During the year, purchases were: Mar. 15 300 units at $23 Sept. 4 ... 290 units at $28...

-

Eq. 7.36a is written for the conservation of momentum in y direction. Obtain Eq. 7.36-b wherein the stream function is independent variable. Eq. 7.36(a,b) y - v v +(1-y/R)v- + momentum: u u R-y + R P...

-

Using Maslen method, find the approximate value of pressure and density at the junction of the sphere and the cone of Problem 7.29 at Mach number 8. Problem 7.29 An empirical way to determine shock...

-

Show that the derivative of the boundary layer edge velocity is given by Eq. 7.64 for the figure given below. Eq. 7.64 M>>1 Ue dx R dy/dx = 1/R

Study smarter with the SolutionInn App