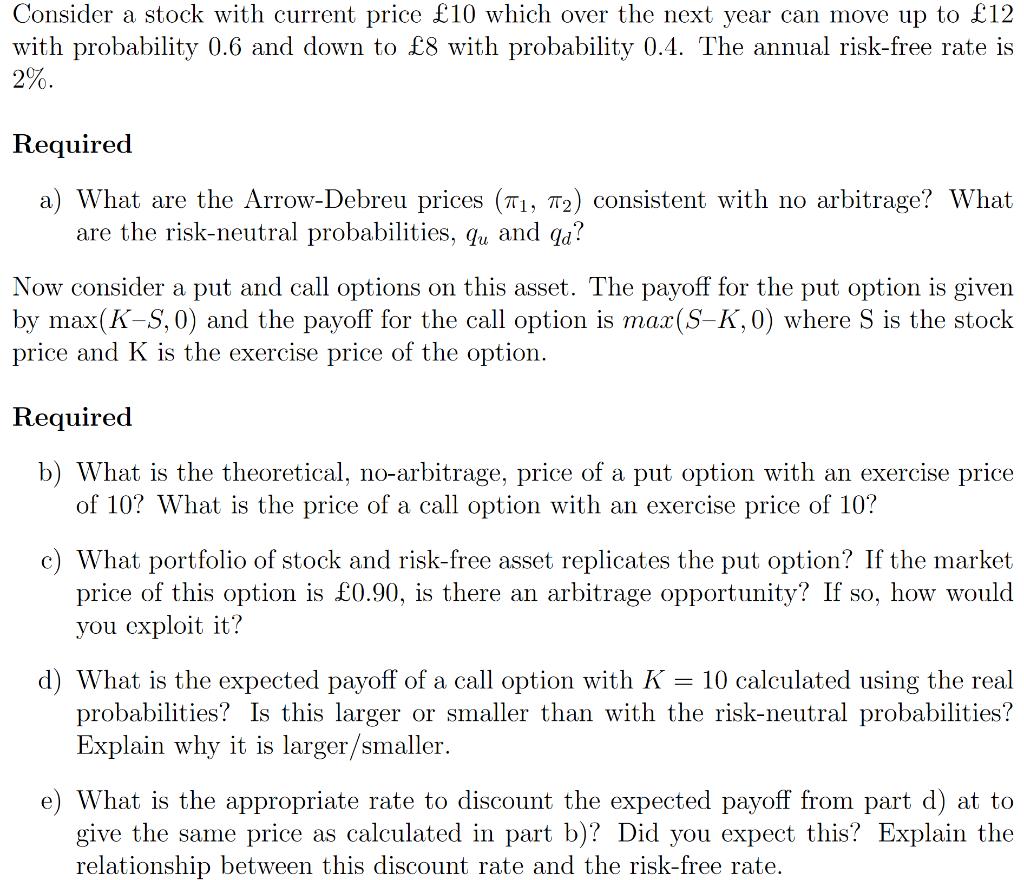

Consider a stock with current price 10 which over the next year can move up to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

ANSWER ANSWER a To find the ArrowDebreu prices we first need to calculate the state prices T1 and T2 Let qd be the probability of a down move and qu be the probability of an up move Then we have T1 1 ... View the full answer

Related Book For

Corporate Finance A Focused Approach

ISBN: 978-1439078082

4th Edition

Authors: Michael C. Ehrhardt , Eugene F. Brigham

Posted Date: