Your line manager has provided you with the following information: Two different clients are facing regular...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

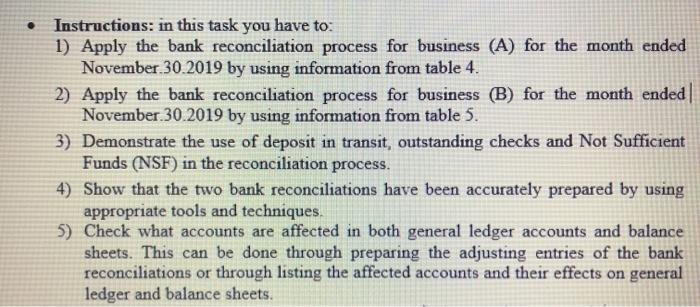

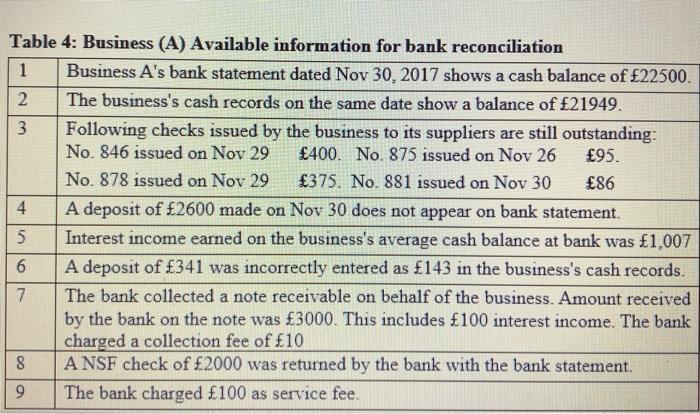

Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. £200. £420. Check No: 201, Issue date: 15 Nov 2017, Check No: 212, Issue date: 19 Nov 2017, Check No: 216, Issue £640. date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. Check No: 201, Issue date: 15 Nov 2017, £200. £420. Check No: 212, Issue Check No: 216, Issue £640. date: 19 Nov 2017, date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. Check No: 201, Issue date: 15 Nov 2017, £200. £420. Check No: 212, Issue Check No: 216, Issue £640. date: 19 Nov 2017, date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. Check No: 201, Issue date: 15 Nov 2017, £200. £420. Check No: 212, Issue Check No: 216, Issue £640. date: 19 Nov 2017, date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. Check No: 201, Issue date: 15 Nov 2017, £200. £420. Check No: 212, Issue Check No: 216, Issue £640. date: 19 Nov 2017, date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. £200. £420. Check No: 201, Issue date: 15 Nov 2017, Check No: 212, Issue date: 19 Nov 2017, Check No: 216, Issue £640. date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. Check No: 201, Issue date: 15 Nov 2017, £200. £420. Check No: 212, Issue Check No: 216, Issue £640. date: 19 Nov 2017, date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. Check No: 201, Issue date: 15 Nov 2017, £200. £420. Check No: 212, Issue Check No: 216, Issue £640. date: 19 Nov 2017, date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. Check No: 201, Issue date: 15 Nov 2017, £200. £420. Check No: 212, Issue Check No: 216, Issue £640. date: 19 Nov 2017, date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Your line manager has provided you with the following information: Two different clients are facing regular monthly problems with matching the cash balance of the bank statement with the cash balance found on their business's records. For this, your line manager has asked you to help these clients to handle and solve this issue by performing bank reconciliations for these two businesses (A & B) by using the available information in table 4&5. ● Instructions: in this task you have to: 1) Apply the bank reconciliation process for business (A) for the month ended November 30.2019 by using information from table 4. 2) Apply the bank reconciliation process for business (B) for the month ended November 30.2019 by using information from table 5. 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets. Table 4: Business (A) Available information for bank reconciliation 1 Business A's bank statement dated Nov 30, 2017 shows a cash balance of £22500. The business's cash records on the same date show a balance of £21949. 2 3 Following checks issued by the business to its suppliers are still outstanding: No. 846 issued on Nov 29 £400. No. 875 issued on Nov 26 £95. No. 878 issued on Nov 29 £375. No. 881 issued on Nov 30 £86 4 5 6 7 8 9 A deposit of £2600 made on Nov 30 does not appear on bank statement. Interest income earned on the business's average cash balance at bank was £1,007 A deposit of £341 was incorrectly entered as £143 in the business's cash records. The bank collected a note receivable on behalf of the business. Amount received by the bank on the note was £3000. This includes £100 interest income. The bank charged a collection fee of £10 ANSF check of £2000 was returned by the bank with the bank statement. The bank charged £100 as service fee. Table 5: Business (B) Available information for bank reconciliation 1 The bank statement of business (B) company shows a balance of £ 12,000 on 31 Nov 2017 The business's ledger shows a balance of £9488on the same date. 2 3 4 5 6 7 8 9 The following checks issued during the month of January have not yet been cleared by the bank. Check No: 201, Issue date: 15 Nov 2017, £200. £420. Check No: 212, Issue Check No: 216, Issue £640. date: 19 Nov 2017, date: 25 Nov 2017, Amount An amount of £1880 sent to the bank for deposit on 30 Nov 2017 does not appear in the bank statement. Amount Amount A note receivable amounting to £3,497 has been collected by bank for the business. The bank has charged £10 for the collection of note. The bank statement shows that interest amounting to £100 has been earned on average account balance during Nov. A check of £450 deposited by the business has been charged back as NSF. An amount of £95 has been deducted by bank as service charges for the month of Nov. The check no. 220 was issued to pay the business electricity. The check was in the amount of £105 but was erroneously recorded in the cash payments journal as £15. LO3: 1) Company (A) Bank Reconciliation Statement: Bank Statement Adjusted balance per bank Book Statement Adjusted balance per book- 2) Company (B) Bank Reconciliation Statement Bank Statement Adjusted balance per bank = Book Statement Adjusted balance per book- 3) Demonstrate the use of deposit in transit, outstanding checks and Not Sufficient Funds (NSF) in the reconciliation process. 4) Show that the two bank reconciliations have been accurately prepared by using appropriate tools and techniques. 5) Check what accounts are affected in both general ledger accounts and balance sheets. This can be done through preparing the adjusting entries of the bank reconciliations or through listing the affected accounts and their effects on general ledger and balance sheets.

Expert Answer:

Answer rating: 100% (QA)

ANSWER 1 Company A Bank Reconciliation Statement Items Unadjusted B... View the full answer

Related Book For

Financial Accounting Information For Decisions

ISBN: 978-0324672701

6th Edition

Authors: Robert w Ingram, Thomas L Albright

Posted Date:

Students also viewed these accounting questions

-

The audit manager has provided you with visualizations (created using visualization software) that include additional analytical information about Dandelions investment portfolio. She has asked you...

-

The Piano Studio Ltd. has provided you with the following information with respect to its piano inventory for the month of August. The company uses the specific identification cost formula....

-

John Ingles has provided you with the following information related to his various investment holdings as of December 31, 2012. Interest earned on joint bank account with his spouse (spouse...

-

At Blossom Company, events and transactions during 2020 included the following. The tax rate for all items is 20%. (1) Depreciation for 2018 was found to be understated by $148000. (2) A strike by...

-

If RRSP contributions of $3030.02 at the end of every six months are projected to generate a plan worth $500,000 in 25 years, what nominal and effective rates of return were assumed in the forecast?

-

Locate the centroid y of the cross-sectional area of the built-upbeam. 1 in.- 6 in. 1 in. 6 in. -| Bin--3 in.E 1 in. 1 in.

-

Monroe Bradstad borrowed \($100,000\) from his aunt, Jeanne Garland, to purchase farmland. Both parties subsequently signed a promissory note stipulating that interest would be accrued prior to or on...

-

Putnam Corporation had these transactions during 2014. (a) Purchased a machine for $30,000, giving a long-term note in exchange. (b) Issued $50,000 par value common stock for cash. (c) Issued...

-

In general, should a country's policymakers be concerned if the country has trade imbalances with other countries? If your answer ispolicymakers "no", are there situations in which policy makers...

-

The finance director of RM plc is considering several investment projects and has collected the following information about them. Projects D and E are mutually exclusive. The capital available for...

-

Downward Dog Ltd (DD) wanted to increase the amount of natural light in its yoga studio. The studio specialized in goat yoga and was held in an old barn on a farm. It decided to purchase a skylight...

-

The Taylor rule is a simple equation that describes movements in the target federal funds rate. It suggests that: a. When inflation rises, the FOMC raises the target rate by 1 times the increase in...

-

Show the impact on the Federal Reserves balance sheet of a foreign exchange market intervention where the Fed purchases $5,000 worth of foreign exchange reserves. Explain what impact, if any, the...

-

One goal of the regulatory reforms that followed the 2007-2009 financial crisis was to address the too-big-to-fail problem associated with large institutions. How did the reforms try to address this...

-

In 2012, the Federal Reserve joined many other central banks by making explicit a numerical target for inflation. Explain how stating that an annual inflation rate of 2 percent over the long run is...

-

A euro-area country that runs very large public deficits or shows a persistently high and rising debt-to-GDP ratio violates the provisions of a 2012 treaty aimed at promoting fiscal stability....

-

Run the program and chat with Magpie. Complete the worksheet with the responses received as the following statements are entered: I want to build a robot. I want to understand French. Do you like...

-

Use the T account for Cash below to record the portion of each of the following transactions, if any that affect cash. How do these transactions affect the companys liquidity? Jan. 2 Provided...

-

Mystic Communications leads its industry in product innovation. Its financial success has been the result of creating innovative products, getting them to market quickly, and building consumer...

-

A wealthy uncle has offered to give you either of two assets: (a) An asset that pays $500 at the end of three years or (b) An asset that pays $100 at the end of each year for five years. Assume that...

-

Explain how a company can have a net loss for a fiscal period but have a net increase in cash from operating activities.

-

Derive Eq. (13.79). Equation (13.79) Pa 1 (1+K) Mnp Mp-1 k=0 1 (Mnp+k) K k! (Mnp) (1+K,

-

Develop a MATLAB program to calculate the cumulative probability of detection.

-

The sum inside Eq. (13.79) presents a very formidable challenge. It can be, however, computed recursively with relative ease. Develop a recursive algorithm to calculate this sum. Equation (13.79)...

Study smarter with the SolutionInn App