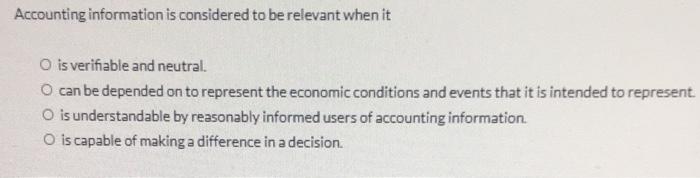

Question: Accounting information is considered to be relevant when it O is verifiable and neutral. O can be depended on to represent the economic conditions and

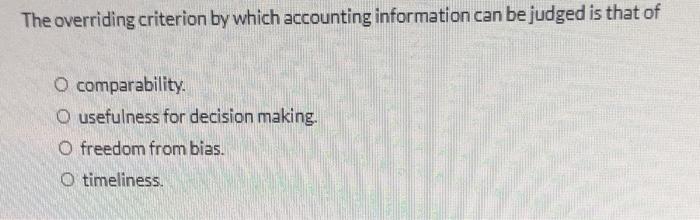

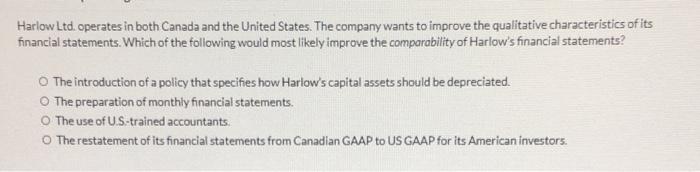

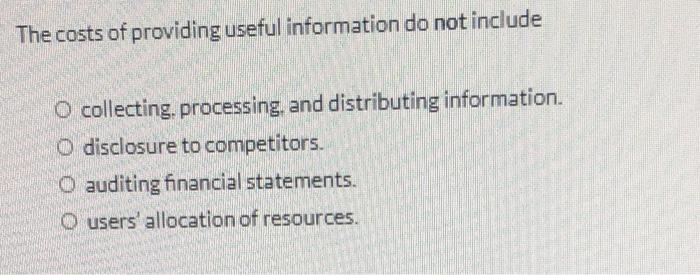

Accounting information is considered to be relevant when it O is verifiable and neutral. O can be depended on to represent the economic conditions and events that it is intended to represent O is understandable by reasonably informed users of accounting information O is capable of making a difference in a decision The overriding criterion by which accounting information can be judged is that of O comparability. O usefulness for decision making. O freedom from bias. O timeliness. Harlow Ltd. operates in both Canada and the United States. The company wants to improve the qualitative characteristics of its financial statements. Which of the following would most likely improve the comparability of Harlow's financial statements? The introduction of a policy that specifies how Harlow's capital assets should be depreciated. The preparation of monthly financial statements. O The use of U.S-trained accountants. The restatement of its financial statements from Canadian GAAP to US GAAP for its American investors. The costs of providing useful information do not include O collecting processing, and distributing information. O disclosure to competitors. O auditing financial statements. o users' allocation of resources. Fundamental qualitative characteristics include O relevance and representational faithfulness. O relevance and comparability. O representational faithfulness and timeliness. O verifiability and relevance

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts