Ques 02: THE CASE IS BASED ON a nonprofit organization. Students are required to analyze the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

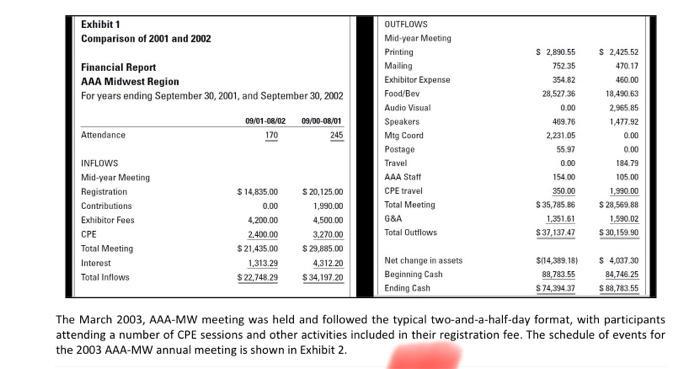

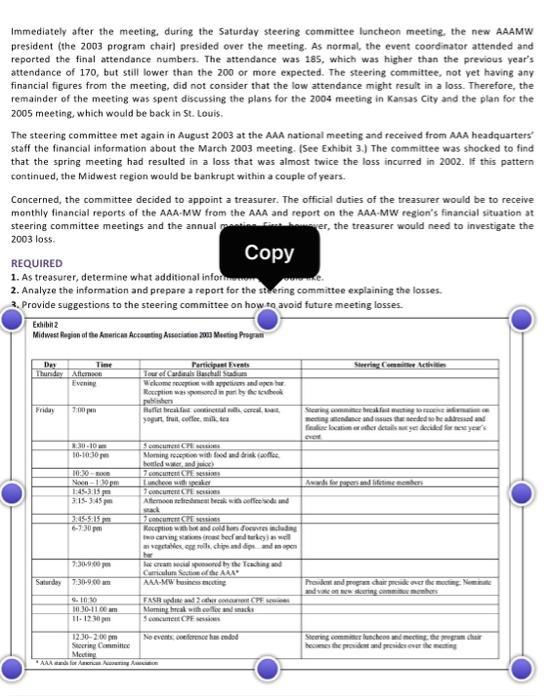

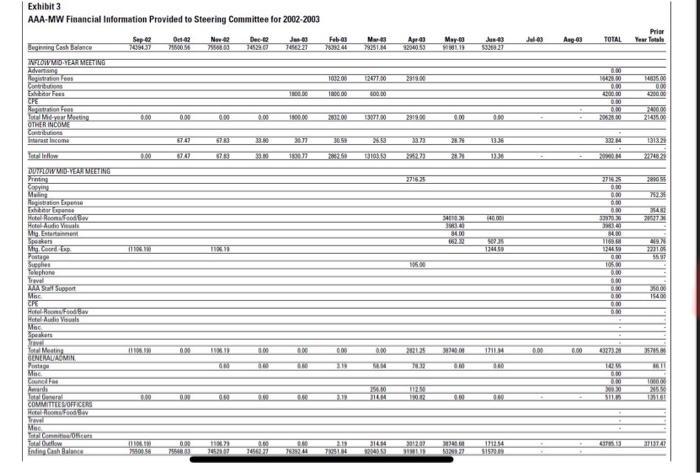

Ques 02: THE CASE IS BASED ON a nonprofit organization. Students are required to analyze the information given in the case to determine what information is relevant for analyzing variances, determine the reason for variances, and provide suggestions to avoid further losses. In addition, the case simulates a real-world situation where all relevant information is not available or not in a format that allows for detailed analysis. Keywords: budgeting, variance analysis, not-for-profit, and volunteer board's responsibility. Budgeting is important in all organizations, but it is especially in nonprofit organizations where revenue sources are often inconsistent from year to year. Nonprofit leadership has a fiscal responsibility to monitor the variances between actual revenues and cost and make operating decisions to ensure the organization's viability and success. INTRODUCTION In August 2003, the Steering Committee of the American Accounting Association Midwest Region (AAA-MW) discovered that its 2003 annual meeting had a net loss of $24,232, leaving a net account balance at less than $50,000. This was on top of a loss of $13,264 the previous year. Concerned about a possible trend, the board created a treasurer position and asked the treasurer to investigate these losses. THE ORGANIZATION The steering committee is an entirely volunteer board whose task is to organize and run an annual conference targeting members of the American Accounting Association who reside in the states of llinois, Indiana, lowa, Kansas Michigan, Minnesota, Missouri, North Dakota, South Dakota, Nebraska, and Wisconsin. The American Accounting Association (AAA) is a not-for-profit organization whose members are primarily accounting academics. organization "promotes worldwide excellence in accounting education, research and practice. Founded in 1916 as the American Association of University Instructors in Accounting, its present name was adopted in 1936. The Association brings together the academic community to further accounting education and to advance the discipline and profession of accounting." The steering committee meets twice a year; every spring at the annual AAA-MW Region meeting and in August at the national meeting of the American Accounting Association. The typical process for organizing the AAA-MW annual meeting was as follows: 1. Eighteen months prior to the meeting (usually at the August AAA national meeting), the steering committee determines in which city within the Midwest region to hold the meeting and submits a meeting site search request to the AAA national office. 2. The program chair for the meeting is a volunteer of the steering committee and is a different (and new) person each year. 3. The event coordinator (a third party hired by the AAA national office) contacts hotels in the chosen city and provides the AAA-MW steering committee with a list of hotels, room rates, and parking rates. 4. At the spring AAA-MW regional meeting, one year prior to the next meeting, the steering committee chooses a hotel based on its location in the city and room rates offered. 5. The event coordinator negotiates the final contract, it is signed by the AAA executive director, and a copy is kept in the AAA headquarter files. 6. The new AAA-MW regional meeting program chair is then responsible for organizing the meeting. There was little in the way of a formal process, so each program chair would determine how he/she wanted to run the meeting. There was a tradition of charging a registration fee that covered food, audiovisual needs, and meeting rooms. The program chair, working with a few other volunteers, would organize the call for papers, review of papers, 2|Page program speakers, receptions, and communication with members within the region. Typically, the meeting had multiple continuing professional education (CPE) sessions, offered breakfast on Friday and Saturday, lunch on Friday, snack breaks on Friday and Saturday morning and Friday afternoon, and evening receptions on both Thursday and Friday. All of this planning was a significant amount of effort and generally consumed the program chair's attention. All cash inflows and outflows were handled by the AAA staff members. They collected registration fees, paid the hotel bills, etc., charging or crediting the region's accounts. The AAA-Mw steering committee president would receive periodic account activity reports. Prior to 2002, the AAA-MW meetings had generally resulted in an increase in cash flow and the steering committee had little need to worry about finances. BACKGROUND At the August 2002 meeting of the AAA-MW steering committee, the committee learned that the spring 2002 regional meeting showed a loss of $14,389.13. The comparison of 2001 and 2002 is shown in Exhibit 1. The 2002 AAA-MW regional meeting had been held in Milwaukee in March and the attendance at that meeting was 170. This was a 30.6 percent drop from the previous year's meeting held in St. Louis, and one of the few times in the region's recent history that the meeting attendance was below 200 attendees. The committee believed the main reason for the low attendance was reluctance to fly (travel) so soon after the after the 9/11 terrorist attack. In addition, the committee believed the location (Milwaukee, Wisconsin)in early spring was difficult to travel to and may not have been appealing. Therefore, the committee was satisfied that the net cash outflow for the 2002 meeting was an anomaly and there was no need for more investigation. As such, the committee proceeded to discuss the plans for the 2003 AAAMW annual meeting, which was to be held the following spring at the Millennium Hotel in St. Louis. The Midwest region had the policy of holding the annual meeting in St. Louis every other year and, because of the central location and more favorable spring weather, the St. Louis meetings had always been well attended. For that reason, the committee was not concerned that the 2003 meeting might result in a loss. Exhibit 1 Comparison of 2001 and 2002 OUTFLOWS Mid-year Meeting Printing S 2,890.55 S 2,425.52 Mailing Exhibitor Expense 752.35 470.17 Financial Report AAA Midwest Region 354.82 460.00 For years ending September 30, 2001, and September 30, 2002 Food/Bev 28,527.36 18,490.63 Audio Visual 0.00 2,965.85 09/01-08/02 170 09/00-08/01 Speakers 489.76 1477.92 Mtg Coord Postage Attendance 245 2,231.05 0.00 55.97 0.00 INFLOWS Travel 0.00 184.79 Mid-year Meeting AAA Statt 154.00 105.00 Registration $ 14,835.00 S 20,125.00 CPE travel 350.00 1,990.00 Contributions 0.00 1,990.00 Total Meeting $35,785.86 $ 28,569.88 1,351.61 $37,137.47 Exhibitor Fees 4,200.00 4,500.00 G&A 1.590.02 CPE 2.400.00 3.270.00 Total Outflows S 30,159.90 Total Meeting $21,435.00 $ 29,885.00 $ 4,037.30 84,746 25 S 88,783.55 Interest 1,313.29 4,312.20 Net change in assets $14,389. 18) Total Inflows $22,748.29 $ 34, 197.20 Beginning Cash 88,783.55 Ending Cash S74,394.37 The March 2003, AAA-MW meeting was held and followed the typical two-and-a-half-day format, with participants attending a number of CPE sessions and other activities included in their registration fee. The schedule of events for the 2003 AAA-MW annual meeting is shown in Exhibit 2. Immediately after the meeting. during the Saturday steering committee luncheon meeting, the new AAAMW president (the 2003 program chair) presided over the meeting. As normal, the event coordinator attended and reported the final attendance numbers. The attendance was 185, which was higher than the previous year's attendance of 170, but still lower than the 200 or more expected. The steering committee, not yet having any financial figures from the meeting, did not consider that the low attendance might result in a loss. Therefore, the remainder of the meeting was spent discussing the plans for the 2004 meeting in Kansas City and the plan for the 2005 meeting, which would be back in St. Louis. The steering committee met again in August 2003 at the AAA national meeting and received from AAA headquarters staff the financial information about the March 2003 meeting. (See Exhibit 3.) The committee was shocked to find that the spring meeting had resulted in a loss that was almost twice the loss incurred in 2002. If this pattern continued, the Midwest region would be bankrupt within a couple of years. Concerned, the committee decided to appoint a treasurer. The official duties of the treasurer would be to receive monthly financial reports of the AAA-MW from the AAA and report on the AAA-MW region's financial situation at steering committee meetings and the annual me 2003 loss. er, the treasurer would need to investigate the Сopy REQUIRED 1. As treasurer, determine what additional infor 2. Analyze the information and prepare a report for the stering committee explaining the losses. 3. Provide suggestions to the steering committee on how to avoid future meeting losses. Exhibit 2 Midwest Region at the Amarican Accounting Asseciation 200 Meting Progra Sering Commie Activitie Dey Thundey Afternn Evening Time Perticipant Frats Tour of Cardaals Banchall Sadn Wekome reoeption with appeties and apen hr Roception was ponsoned in puri by the teheok peblishers Baflet hreal fa cotineal creal, a yogurt, truit, cofler. mik te T00 p a aIa s meing mendance and ssues the seededo he adressad and finlie kocation e uber detals yet decide art ye's Friday 30-10 Somcument CE Moming reepeon with fod and drisk (afee botled wer, and juce) 7 concurtett CPE sesi Lunchen wih peaker Fconcumene C ese Aftemoon seedment beck wih oofleodi nd ak 17 concurer CE sestines Roception wth bt and cold he doeres dadng o canving sis iroa becf d terke)wl vagetales, og rolh, chipe and dipnandmapen 10-1030 p 10:30- Noen-130 pm 145315 m 315-3:45 pm Awads for papers nd lifetime nenhers 3:45-515 pm 130 pm cream elpuored by the Teaching nd Curiculun Section of dhe AAA AAA-MW besines mecting 7:3090 pm Saturday Prodt nd prog chair preside over themoting Nemie and vate on new skering commit menhers 7:30-90 am . 1010 10.30-11 00 am I1- 1230 pen FASH de and 2 odr conan CPF Moming hreak with collor and unacks Sconcunen CPE sessin No events coeference han ended 1230-200 pm Saccring Committee Meeting *AAA for Aaenan Aarang A Steering comminer luncheon and mecting the pregram chair becmes the providetand presides ever the meting Exhibit 3 AAA-MW Financial Information Provided to Steering Committee for 2002-2003 Prier Oet 42 00 M Dec- 745297 Feba 7039244 Sep2 74394.37 May-00 Jun43 Ang 3 TOTAL Year Tetale Ne42 Ma Jul43 Begening Cash belance 744227 12040 53 NFLOWMIO TEARMEETING Tvtang 00 103200 1247700 2919.00 Contrtuton Ear Fees M835.00 00 4200.00 100.00 00.00 0.00 000 2020 Tta Mer Ming OTHER INCOME Cabutions iarat com 00 000 000 000 100 00 201200 291.00 2145.00 6747 3324 0.00 2026 DUYFLOWMIDVEAR MEETING Freting Copying 2716 25 200M 0.00 0.00 Rugstton Espee Esher tpene Hetel Roomod Hotel Aut Vals Mg. Entartanen Speken 0.00 3337030 40.00 8400 B00 Cord E Pstage 1244 0 0.00 TOK00 6.00 1344.50 2231.06 55.97 Telephone Tevel XXAS Suppert Mac 000 15400 0.00 Hete R o Hete Aulin Vouls Speakars Jravel Mesting GENERALAGMIN Fustage Mac Cnc Fas 0.00 100 0.00 202125 1711M 000 6.00 5745 146 0.00 200.30 COMMITTLES OFFICERS Hotel Roomad Travel Ta Commte Kren Tatal Dutlow nting Cnh Balanc 0.00 20127 11254 37137.47 7580156 755483 7639244 3214 Ques 02: THE CASE IS BASED ON a nonprofit organization. Students are required to analyze the information given in the case to determine what information is relevant for analyzing variances, determine the reason for variances, and provide suggestions to avoid further losses. In addition, the case simulates a real-world situation where all relevant information is not available or not in a format that allows for detailed analysis. Keywords: budgeting, variance analysis, not-for-profit, and volunteer board's responsibility. Budgeting is important in all organizations, but it is especially in nonprofit organizations where revenue sources are often inconsistent from year to year. Nonprofit leadership has a fiscal responsibility to monitor the variances between actual revenues and cost and make operating decisions to ensure the organization's viability and success. INTRODUCTION In August 2003, the Steering Committee of the American Accounting Association Midwest Region (AAA-MW) discovered that its 2003 annual meeting had a net loss of $24,232, leaving a net account balance at less than $50,000. This was on top of a loss of $13,264 the previous year. Concerned about a possible trend, the board created a treasurer position and asked the treasurer to investigate these losses. THE ORGANIZATION The steering committee is an entirely volunteer board whose task is to organize and run an annual conference targeting members of the American Accounting Association who reside in the states of llinois, Indiana, lowa, Kansas Michigan, Minnesota, Missouri, North Dakota, South Dakota, Nebraska, and Wisconsin. The American Accounting Association (AAA) is a not-for-profit organization whose members are primarily accounting academics. organization "promotes worldwide excellence in accounting education, research and practice. Founded in 1916 as the American Association of University Instructors in Accounting, its present name was adopted in 1936. The Association brings together the academic community to further accounting education and to advance the discipline and profession of accounting." The steering committee meets twice a year; every spring at the annual AAA-MW Region meeting and in August at the national meeting of the American Accounting Association. The typical process for organizing the AAA-MW annual meeting was as follows: 1. Eighteen months prior to the meeting (usually at the August AAA national meeting), the steering committee determines in which city within the Midwest region to hold the meeting and submits a meeting site search request to the AAA national office. 2. The program chair for the meeting is a volunteer of the steering committee and is a different (and new) person each year. 3. The event coordinator (a third party hired by the AAA national office) contacts hotels in the chosen city and provides the AAA-MW steering committee with a list of hotels, room rates, and parking rates. 4. At the spring AAA-MW regional meeting, one year prior to the next meeting, the steering committee chooses a hotel based on its location in the city and room rates offered. 5. The event coordinator negotiates the final contract, it is signed by the AAA executive director, and a copy is kept in the AAA headquarter files. 6. The new AAA-MW regional meeting program chair is then responsible for organizing the meeting. There was little in the way of a formal process, so each program chair would determine how he/she wanted to run the meeting. There was a tradition of charging a registration fee that covered food, audiovisual needs, and meeting rooms. The program chair, working with a few other volunteers, would organize the call for papers, review of papers, 2|Page program speakers, receptions, and communication with members within the region. Typically, the meeting had multiple continuing professional education (CPE) sessions, offered breakfast on Friday and Saturday, lunch on Friday, snack breaks on Friday and Saturday morning and Friday afternoon, and evening receptions on both Thursday and Friday. All of this planning was a significant amount of effort and generally consumed the program chair's attention. All cash inflows and outflows were handled by the AAA staff members. They collected registration fees, paid the hotel bills, etc., charging or crediting the region's accounts. The AAA-Mw steering committee president would receive periodic account activity reports. Prior to 2002, the AAA-MW meetings had generally resulted in an increase in cash flow and the steering committee had little need to worry about finances. BACKGROUND At the August 2002 meeting of the AAA-MW steering committee, the committee learned that the spring 2002 regional meeting showed a loss of $14,389.13. The comparison of 2001 and 2002 is shown in Exhibit 1. The 2002 AAA-MW regional meeting had been held in Milwaukee in March and the attendance at that meeting was 170. This was a 30.6 percent drop from the previous year's meeting held in St. Louis, and one of the few times in the region's recent history that the meeting attendance was below 200 attendees. The committee believed the main reason for the low attendance was reluctance to fly (travel) so soon after the after the 9/11 terrorist attack. In addition, the committee believed the location (Milwaukee, Wisconsin)in early spring was difficult to travel to and may not have been appealing. Therefore, the committee was satisfied that the net cash outflow for the 2002 meeting was an anomaly and there was no need for more investigation. As such, the committee proceeded to discuss the plans for the 2003 AAAMW annual meeting, which was to be held the following spring at the Millennium Hotel in St. Louis. The Midwest region had the policy of holding the annual meeting in St. Louis every other year and, because of the central location and more favorable spring weather, the St. Louis meetings had always been well attended. For that reason, the committee was not concerned that the 2003 meeting might result in a loss. Exhibit 1 Comparison of 2001 and 2002 OUTFLOWS Mid-year Meeting Printing S 2,890.55 S 2,425.52 Mailing Exhibitor Expense 752.35 470.17 Financial Report AAA Midwest Region 354.82 460.00 For years ending September 30, 2001, and September 30, 2002 Food/Bev 28,527.36 18,490.63 Audio Visual 0.00 2,965.85 09/01-08/02 170 09/00-08/01 Speakers 489.76 1477.92 Mtg Coord Postage Attendance 245 2,231.05 0.00 55.97 0.00 INFLOWS Travel 0.00 184.79 Mid-year Meeting AAA Statt 154.00 105.00 Registration $ 14,835.00 S 20,125.00 CPE travel 350.00 1,990.00 Contributions 0.00 1,990.00 Total Meeting $35,785.86 $ 28,569.88 1,351.61 $37,137.47 Exhibitor Fees 4,200.00 4,500.00 G&A 1.590.02 CPE 2.400.00 3.270.00 Total Outflows S 30,159.90 Total Meeting $21,435.00 $ 29,885.00 $ 4,037.30 84,746 25 S 88,783.55 Interest 1,313.29 4,312.20 Net change in assets $14,389. 18) Total Inflows $22,748.29 $ 34, 197.20 Beginning Cash 88,783.55 Ending Cash S74,394.37 The March 2003, AAA-MW meeting was held and followed the typical two-and-a-half-day format, with participants attending a number of CPE sessions and other activities included in their registration fee. The schedule of events for the 2003 AAA-MW annual meeting is shown in Exhibit 2. Immediately after the meeting. during the Saturday steering committee luncheon meeting, the new AAAMW president (the 2003 program chair) presided over the meeting. As normal, the event coordinator attended and reported the final attendance numbers. The attendance was 185, which was higher than the previous year's attendance of 170, but still lower than the 200 or more expected. The steering committee, not yet having any financial figures from the meeting, did not consider that the low attendance might result in a loss. Therefore, the remainder of the meeting was spent discussing the plans for the 2004 meeting in Kansas City and the plan for the 2005 meeting, which would be back in St. Louis. The steering committee met again in August 2003 at the AAA national meeting and received from AAA headquarters staff the financial information about the March 2003 meeting. (See Exhibit 3.) The committee was shocked to find that the spring meeting had resulted in a loss that was almost twice the loss incurred in 2002. If this pattern continued, the Midwest region would be bankrupt within a couple of years. Concerned, the committee decided to appoint a treasurer. The official duties of the treasurer would be to receive monthly financial reports of the AAA-MW from the AAA and report on the AAA-MW region's financial situation at steering committee meetings and the annual me 2003 loss. er, the treasurer would need to investigate the Сopy REQUIRED 1. As treasurer, determine what additional infor 2. Analyze the information and prepare a report for the stering committee explaining the losses. 3. Provide suggestions to the steering committee on how to avoid future meeting losses. Exhibit 2 Midwest Region at the Amarican Accounting Asseciation 200 Meting Progra Sering Commie Activitie Dey Thundey Afternn Evening Time Perticipant Frats Tour of Cardaals Banchall Sadn Wekome reoeption with appeties and apen hr Roception was ponsoned in puri by the teheok peblishers Baflet hreal fa cotineal creal, a yogurt, truit, cofler. mik te T00 p a aIa s meing mendance and ssues the seededo he adressad and finlie kocation e uber detals yet decide art ye's Friday 30-10 Somcument CE Moming reepeon with fod and drisk (afee botled wer, and juce) 7 concurtett CPE sesi Lunchen wih peaker Fconcumene C ese Aftemoon seedment beck wih oofleodi nd ak 17 concurer CE sestines Roception wth bt and cold he doeres dadng o canving sis iroa becf d terke)wl vagetales, og rolh, chipe and dipnandmapen 10-1030 p 10:30- Noen-130 pm 145315 m 315-3:45 pm Awads for papers nd lifetime nenhers 3:45-515 pm 130 pm cream elpuored by the Teaching nd Curiculun Section of dhe AAA AAA-MW besines mecting 7:3090 pm Saturday Prodt nd prog chair preside over themoting Nemie and vate on new skering commit menhers 7:30-90 am . 1010 10.30-11 00 am I1- 1230 pen FASH de and 2 odr conan CPF Moming hreak with collor and unacks Sconcunen CPE sessin No events coeference han ended 1230-200 pm Saccring Committee Meeting *AAA for Aaenan Aarang A Steering comminer luncheon and mecting the pregram chair becmes the providetand presides ever the meting Exhibit 3 AAA-MW Financial Information Provided to Steering Committee for 2002-2003 Prier Oet 42 00 M Dec- 745297 Feba 7039244 Sep2 74394.37 May-00 Jun43 Ang 3 TOTAL Year Tetale Ne42 Ma Jul43 Begening Cash belance 744227 12040 53 NFLOWMIO TEARMEETING Tvtang 00 103200 1247700 2919.00 Contrtuton Ear Fees M835.00 00 4200.00 100.00 00.00 0.00 000 2020 Tta Mer Ming OTHER INCOME Cabutions iarat com 00 000 000 000 100 00 201200 291.00 2145.00 6747 3324 0.00 2026 DUYFLOWMIDVEAR MEETING Freting Copying 2716 25 200M 0.00 0.00 Rugstton Espee Esher tpene Hetel Roomod Hotel Aut Vals Mg. Entartanen Speken 0.00 3337030 40.00 8400 B00 Cord E Pstage 1244 0 0.00 TOK00 6.00 1344.50 2231.06 55.97 Telephone Tevel XXAS Suppert Mac 000 15400 0.00 Hete R o Hete Aulin Vouls Speakars Jravel Mesting GENERALAGMIN Fustage Mac Cnc Fas 0.00 100 0.00 202125 1711M 000 6.00 5745 146 0.00 200.30 COMMITTLES OFFICERS Hotel Roomad Travel Ta Commte Kren Tatal Dutlow nting Cnh Balanc 0.00 20127 11254 37137.47 7580156 755483 7639244 3214

Expert Answer:

Related Book For

Posted Date:

Students also viewed these finance questions

-

When the Steering Committee of the Physicians Health Study Research Group (1988) reported the results of the effect of aspirin on heart attacks, committee members also reported the results of the...

-

Prince Albert Canning PLC had a net loss of 45,831 on sales of 198,352. What was the companys profit margin? Does the fact that these figures are quoted in a foreign currency make any difference?...

-

Prince Albert Canning PLC had a net loss of 37,543 on sales of 345,182. What was the companys profit margin? Does the fact that these figures are quoted in a foreign currency make any difference?...

-

With only a straightedge and compass, use a number line and the Pythagorean theorem to construct a segment whose length is 2. Measure the segment as accurately as possible, and write your answer in...

-

A distributer of prewashed shredded lettuce is opening a new plant and considering whether to use a mechanized process or a manual process to prepare the product. The manual process will have a fixed...

-

Walton Corporation began operations on April 1 by issuing 50,000 shares of $2 par value common stock for cash at $13 per share. On April 19, it issued 2,000 shares of common stock to attorneys in...

-

Do the following activities to complete your marketing plan: 1. Draw a simple organizational chart for your organization. 2. Develop a Gantt chart (see Chapter 2) to schedule the key activities...

-

Weighted-average method. Ashworth Handcraft is a manufacturer of picture frames for large retailers. Every picture frame passes through two departments: the assembly department and the finishing...

-

Let the widget industry demand curve be given by P= 200 - Q, where Q is the industry output. There are two firms, Firm 1 and Firm 2. Each has a marginal cost of $20. 1. Assume that these two firms...

-

A. Describe Spatial Technologys business model in terms of revenues, profits, and cash flows. B. What intellectual properly, if any, does Spatial Technology possess? C. Describe the experience and...

-

Modern private international law developed from the need to __________________ issues involving commercial transactions between traders belonging to different cities. A. Conciliate. B. Reconcile. C....

-

1. What is positive, what The Founder negative about Ray Kroc's character? 2. What ethical approach describes Kroc's activities? 3 What ethical position is taken by the McDonald's brothers? 4 What is...

-

The senior on a CPA firm's largest audit engagement received a request from the client's CFO for a copy of "any communications the firm has sent relating tointernal-control-relatedmatters identified...

-

In the "The Rationale of Cost Accounting" by R.S. Edwards the author writes about the problematic nature of costing overhead. In your own words, explain why costing overhead can be problematic and...

-

The velocity of an airplane flying into a headwind is given by v(t) = 30 (25-t2) mi/hr for 0 st4 hr. Assume that s(0) = 0. a. Determine the position function for Osts4. b. How far does the airplane...

-

Students in a particular class breathe a sigh of relief when they see that their professor does not have the red folder that he always carries into class when he administers pop quizzes. This CR by...

-

Write a program that reads the student information from a tab separated values (tsv) file and creates a text file that contains student information together with the course grades of the students....

-

Eleni Cabinet Company sold 2,200 cabinets during 2011 at $160 per cabinet. Its beginning inventory on January 1 was 130 cabinets at $56. Purchases made during the year were as follows: February . 225...

-

In a special double issue of Time magazine, the cover story featured Pope John Paul II as Man of the Year (26 December 19942 January 1995, pp. 7476). As part of the story, Time reported on the...

-

Give an example of two questions in which the order in which they are presented would determine whether the responses were likely to be biased.

-

In a test for extrasensory perception (ESP), described in Case Study 13.1 in the next chapter, people were asked to try to use psychic abilities to describe a hidden photo or video segment being...

-

Refer to the latest financial report of JB Hi-Fi Limited on its website, www.jbhifi.com.au, and answer the following questions. 1. Is it likely that JB Hi-Fi Limited would have to confront such...

-

Imelda Instruments Ltd manufactures two products: missile range instruments and space pressure gauges. During January, 53 range instruments and 360 pressure gauges were produced, and overhead costs...

-

Swiss Chocolates Ltd produces blocks of chocolate. Raw materials in the form of cocoa solids, milk and sugar are added at the beginning of the process, flavouring, fruit and nuts are added half-way...

Study smarter with the SolutionInn App