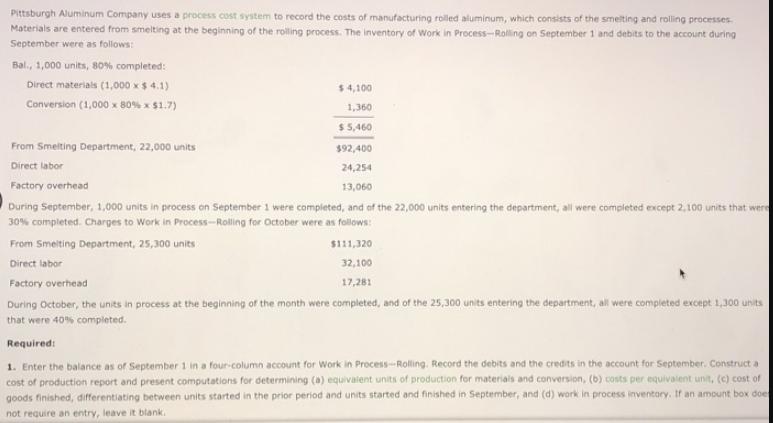

Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

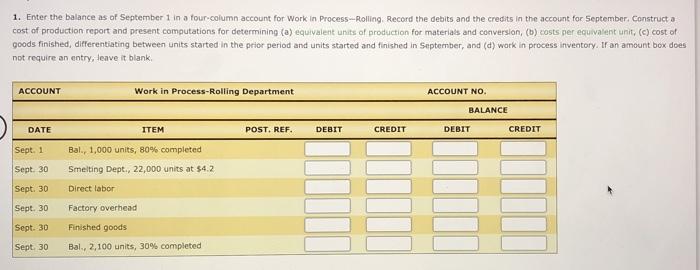

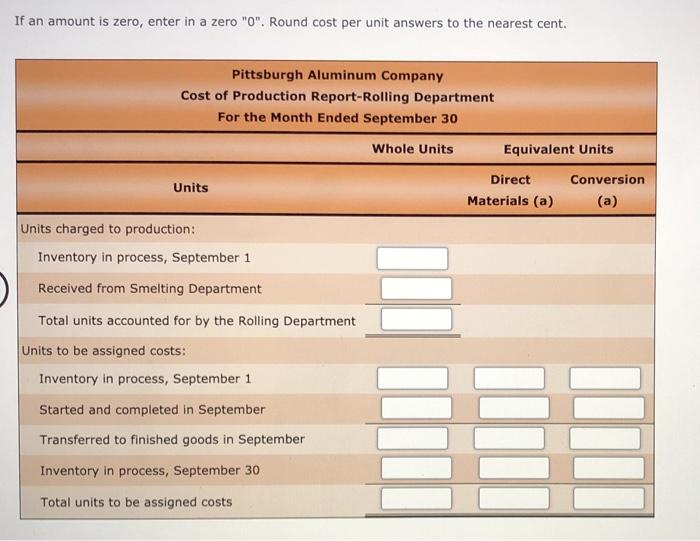

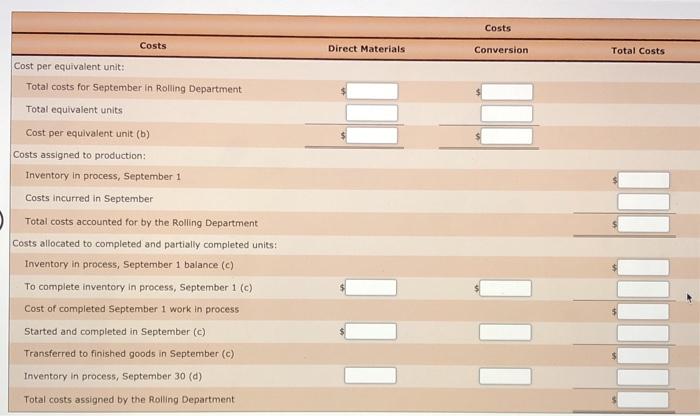

Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process-Rolling on September 1 and debits to the account during September were as follows: Bal, 1,000 units, 80% completed: Direct materials (1,000 x$ 4.1) Conversion (1,000 x 80% x $1.7) $ 4,100 1,360 $ 5,460 From Smeiting Department, 22,000 units $92,400 Direct labor 24,254 Factory overhead 13,060 During September, 1,000 units in process on September 1 were completed, and of the 22,000 units entering the department, all were completed except 2,100 units that were 30% completed. Charges to Work in Process-Rolling for October were as follows: From Smelting Department, 25,300 units $111,320 Direct labor 32,100 Factory overhead 17,281 During October, the units in process at the beginning of the month were completed, and of the 25,300 units entering the department, all were completed except 1,300 units that were 40% completed. Required: 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. Ir an amount box doe not require an entry, leave it blank. 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT No. BALANCE DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT Sept. 1 Bal., 1,000 units, 80% completed Sept. 30 Smelting Dept., 22,000 units at $4.2 Sept. 30 Direct labor Sept. 30 Factory overhead Sept. 30 Finished goods Sept. 30 Bal., 2,100 units, 30% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended September 30 Whole Units Equivalent Units Direct Conversion Units Materials (a) (a) Units charged to production: Inventory in process, September 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, September 1 Started and completed in September Transferred to finished goods in September Inventory in process, September 30 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for September in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, September 1 Costs incurred in September O Total costs accounted for by the Rolling Department Costs allocated to completed and partially completed units: Inventory in process, September 1 balance (c) To complete inventory in process, September 1 (c) Cost of completed September 1 work in process Started and completed in September (c) Transferred to finished goods in September (c) Inventory in process, September 30 (d) Total costs assigned by the Rolling Department 2. Provide the same information for October by recording the October transactions in the four-column work in process account. Construct a cost of production report, and present the October computations (a through d) listed in part (1). If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT NO. Balance DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT October 1 Balance October 31 Smelting Dept., 25,300 units at $4.4 October 31 Direct labor October 31 Factory overhead October 31 Finished goods October 31 Bal, 1,300 units, 40% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. If an amount is zero, enter in a zero "O". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended October 31 Whole Units Equivalent Units Units Direct Conversion Materials (a) (a) Units charged to production: Inventory in process, October 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, October 1 Started and completed in October Transferred to finished goods in October Inventory in process, October 31 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for October in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, October 1 Costs incurred in October Total costs accounted for by the Rolling Department Costs allocated to completed and partially.completed units: Inventory in process, October1 balance (c) To complete inventory in process, October 1 (c) Cost of completed October 1 work in process Started and completed in October (c) Transferred to finished goods in October (c) Inventory in process, October 31 (d) Total costs assigned by the Rolling Department from from August to October. The cost per equivalent unit for conversion costs 3. The cost per equivalent unit for direct materials August to October. These changes be investigated for their underlying causes, and any necessary corrective actions should be taken. Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process-Rolling on September 1 and debits to the account during September were as follows: Bal, 1,000 units, 80% completed: Direct materials (1,000 x$ 4.1) Conversion (1,000 x 80% x $1.7) $ 4,100 1,360 $ 5,460 From Smeiting Department, 22,000 units $92,400 Direct labor 24,254 Factory overhead 13,060 During September, 1,000 units in process on September 1 were completed, and of the 22,000 units entering the department, all were completed except 2,100 units that were 30% completed. Charges to Work in Process-Rolling for October were as follows: From Smelting Department, 25,300 units $111,320 Direct labor 32,100 Factory overhead 17,281 During October, the units in process at the beginning of the month were completed, and of the 25,300 units entering the department, all were completed except 1,300 units that were 40% completed. Required: 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. Ir an amount box doe not require an entry, leave it blank. 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT No. BALANCE DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT Sept. 1 Bal., 1,000 units, 80% completed Sept. 30 Smelting Dept., 22,000 units at $4.2 Sept. 30 Direct labor Sept. 30 Factory overhead Sept. 30 Finished goods Sept. 30 Bal., 2,100 units, 30% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended September 30 Whole Units Equivalent Units Direct Conversion Units Materials (a) (a) Units charged to production: Inventory in process, September 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, September 1 Started and completed in September Transferred to finished goods in September Inventory in process, September 30 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for September in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, September 1 Costs incurred in September O Total costs accounted for by the Rolling Department Costs allocated to completed and partially completed units: Inventory in process, September 1 balance (c) To complete inventory in process, September 1 (c) Cost of completed September 1 work in process Started and completed in September (c) Transferred to finished goods in September (c) Inventory in process, September 30 (d) Total costs assigned by the Rolling Department 2. Provide the same information for October by recording the October transactions in the four-column work in process account. Construct a cost of production report, and present the October computations (a through d) listed in part (1). If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT NO. Balance DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT October 1 Balance October 31 Smelting Dept., 25,300 units at $4.4 October 31 Direct labor October 31 Factory overhead October 31 Finished goods October 31 Bal, 1,300 units, 40% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. If an amount is zero, enter in a zero "O". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended October 31 Whole Units Equivalent Units Units Direct Conversion Materials (a) (a) Units charged to production: Inventory in process, October 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, October 1 Started and completed in October Transferred to finished goods in October Inventory in process, October 31 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for October in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, October 1 Costs incurred in October Total costs accounted for by the Rolling Department Costs allocated to completed and partially.completed units: Inventory in process, October1 balance (c) To complete inventory in process, October 1 (c) Cost of completed October 1 work in process Started and completed in October (c) Transferred to finished goods in October (c) Inventory in process, October 31 (d) Total costs assigned by the Rolling Department from from August to October. The cost per equivalent unit for conversion costs 3. The cost per equivalent unit for direct materials August to October. These changes be investigated for their underlying causes, and any necessary corrective actions should be taken. Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process-Rolling on September 1 and debits to the account during September were as follows: Bal, 1,000 units, 80% completed: Direct materials (1,000 x$ 4.1) Conversion (1,000 x 80% x $1.7) $ 4,100 1,360 $ 5,460 From Smeiting Department, 22,000 units $92,400 Direct labor 24,254 Factory overhead 13,060 During September, 1,000 units in process on September 1 were completed, and of the 22,000 units entering the department, all were completed except 2,100 units that were 30% completed. Charges to Work in Process-Rolling for October were as follows: From Smelting Department, 25,300 units $111,320 Direct labor 32,100 Factory overhead 17,281 During October, the units in process at the beginning of the month were completed, and of the 25,300 units entering the department, all were completed except 1,300 units that were 40% completed. Required: 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. Ir an amount box doe not require an entry, leave it blank. 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT No. BALANCE DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT Sept. 1 Bal., 1,000 units, 80% completed Sept. 30 Smelting Dept., 22,000 units at $4.2 Sept. 30 Direct labor Sept. 30 Factory overhead Sept. 30 Finished goods Sept. 30 Bal., 2,100 units, 30% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended September 30 Whole Units Equivalent Units Direct Conversion Units Materials (a) (a) Units charged to production: Inventory in process, September 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, September 1 Started and completed in September Transferred to finished goods in September Inventory in process, September 30 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for September in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, September 1 Costs incurred in September O Total costs accounted for by the Rolling Department Costs allocated to completed and partially completed units: Inventory in process, September 1 balance (c) To complete inventory in process, September 1 (c) Cost of completed September 1 work in process Started and completed in September (c) Transferred to finished goods in September (c) Inventory in process, September 30 (d) Total costs assigned by the Rolling Department 2. Provide the same information for October by recording the October transactions in the four-column work in process account. Construct a cost of production report, and present the October computations (a through d) listed in part (1). If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT NO. Balance DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT October 1 Balance October 31 Smelting Dept., 25,300 units at $4.4 October 31 Direct labor October 31 Factory overhead October 31 Finished goods October 31 Bal, 1,300 units, 40% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. If an amount is zero, enter in a zero "O". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended October 31 Whole Units Equivalent Units Units Direct Conversion Materials (a) (a) Units charged to production: Inventory in process, October 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, October 1 Started and completed in October Transferred to finished goods in October Inventory in process, October 31 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for October in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, October 1 Costs incurred in October Total costs accounted for by the Rolling Department Costs allocated to completed and partially.completed units: Inventory in process, October1 balance (c) To complete inventory in process, October 1 (c) Cost of completed October 1 work in process Started and completed in October (c) Transferred to finished goods in October (c) Inventory in process, October 31 (d) Total costs assigned by the Rolling Department from from August to October. The cost per equivalent unit for conversion costs 3. The cost per equivalent unit for direct materials August to October. These changes be investigated for their underlying causes, and any necessary corrective actions should be taken. Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process-Rolling on September 1 and debits to the account during September were as follows: Bal, 1,000 units, 80% completed: Direct materials (1,000 x$ 4.1) Conversion (1,000 x 80% x $1.7) $ 4,100 1,360 $ 5,460 From Smeiting Department, 22,000 units $92,400 Direct labor 24,254 Factory overhead 13,060 During September, 1,000 units in process on September 1 were completed, and of the 22,000 units entering the department, all were completed except 2,100 units that were 30% completed. Charges to Work in Process-Rolling for October were as follows: From Smelting Department, 25,300 units $111,320 Direct labor 32,100 Factory overhead 17,281 During October, the units in process at the beginning of the month were completed, and of the 25,300 units entering the department, all were completed except 1,300 units that were 40% completed. Required: 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. Ir an amount box doe not require an entry, leave it blank. 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT No. BALANCE DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT Sept. 1 Bal., 1,000 units, 80% completed Sept. 30 Smelting Dept., 22,000 units at $4.2 Sept. 30 Direct labor Sept. 30 Factory overhead Sept. 30 Finished goods Sept. 30 Bal., 2,100 units, 30% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended September 30 Whole Units Equivalent Units Direct Conversion Units Materials (a) (a) Units charged to production: Inventory in process, September 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, September 1 Started and completed in September Transferred to finished goods in September Inventory in process, September 30 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for September in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, September 1 Costs incurred in September O Total costs accounted for by the Rolling Department Costs allocated to completed and partially completed units: Inventory in process, September 1 balance (c) To complete inventory in process, September 1 (c) Cost of completed September 1 work in process Started and completed in September (c) Transferred to finished goods in September (c) Inventory in process, September 30 (d) Total costs assigned by the Rolling Department 2. Provide the same information for October by recording the October transactions in the four-column work in process account. Construct a cost of production report, and present the October computations (a through d) listed in part (1). If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT NO. Balance DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT October 1 Balance October 31 Smelting Dept., 25,300 units at $4.4 October 31 Direct labor October 31 Factory overhead October 31 Finished goods October 31 Bal, 1,300 units, 40% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. If an amount is zero, enter in a zero "O". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended October 31 Whole Units Equivalent Units Units Direct Conversion Materials (a) (a) Units charged to production: Inventory in process, October 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, October 1 Started and completed in October Transferred to finished goods in October Inventory in process, October 31 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for October in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, October 1 Costs incurred in October Total costs accounted for by the Rolling Department Costs allocated to completed and partially.completed units: Inventory in process, October1 balance (c) To complete inventory in process, October 1 (c) Cost of completed October 1 work in process Started and completed in October (c) Transferred to finished goods in October (c) Inventory in process, October 31 (d) Total costs assigned by the Rolling Department from from August to October. The cost per equivalent unit for conversion costs 3. The cost per equivalent unit for direct materials August to October. These changes be investigated for their underlying causes, and any necessary corrective actions should be taken. Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process-Rolling on September 1 and debits to the account during September were as follows: Bal, 1,000 units, 80% completed: Direct materials (1,000 x$ 4.1) Conversion (1,000 x 80% x $1.7) $ 4,100 1,360 $ 5,460 From Smeiting Department, 22,000 units $92,400 Direct labor 24,254 Factory overhead 13,060 During September, 1,000 units in process on September 1 were completed, and of the 22,000 units entering the department, all were completed except 2,100 units that were 30% completed. Charges to Work in Process-Rolling for October were as follows: From Smelting Department, 25,300 units $111,320 Direct labor 32,100 Factory overhead 17,281 During October, the units in process at the beginning of the month were completed, and of the 25,300 units entering the department, all were completed except 1,300 units that were 40% completed. Required: 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. Ir an amount box doe not require an entry, leave it blank. 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT No. BALANCE DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT Sept. 1 Bal., 1,000 units, 80% completed Sept. 30 Smelting Dept., 22,000 units at $4.2 Sept. 30 Direct labor Sept. 30 Factory overhead Sept. 30 Finished goods Sept. 30 Bal., 2,100 units, 30% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended September 30 Whole Units Equivalent Units Direct Conversion Units Materials (a) (a) Units charged to production: Inventory in process, September 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, September 1 Started and completed in September Transferred to finished goods in September Inventory in process, September 30 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for September in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, September 1 Costs incurred in September O Total costs accounted for by the Rolling Department Costs allocated to completed and partially completed units: Inventory in process, September 1 balance (c) To complete inventory in process, September 1 (c) Cost of completed September 1 work in process Started and completed in September (c) Transferred to finished goods in September (c) Inventory in process, September 30 (d) Total costs assigned by the Rolling Department 2. Provide the same information for October by recording the October transactions in the four-column work in process account. Construct a cost of production report, and present the October computations (a through d) listed in part (1). If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT NO. Balance DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT October 1 Balance October 31 Smelting Dept., 25,300 units at $4.4 October 31 Direct labor October 31 Factory overhead October 31 Finished goods October 31 Bal, 1,300 units, 40% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. If an amount is zero, enter in a zero "O". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended October 31 Whole Units Equivalent Units Units Direct Conversion Materials (a) (a) Units charged to production: Inventory in process, October 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, October 1 Started and completed in October Transferred to finished goods in October Inventory in process, October 31 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for October in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, October 1 Costs incurred in October Total costs accounted for by the Rolling Department Costs allocated to completed and partially.completed units: Inventory in process, October1 balance (c) To complete inventory in process, October 1 (c) Cost of completed October 1 work in process Started and completed in October (c) Transferred to finished goods in October (c) Inventory in process, October 31 (d) Total costs assigned by the Rolling Department from from August to October. The cost per equivalent unit for conversion costs 3. The cost per equivalent unit for direct materials August to October. These changes be investigated for their underlying causes, and any necessary corrective actions should be taken. Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting at the beginning of the rolling process. The inventory of Work in Process-Rolling on September 1 and debits to the account during September were as follows: Bal, 1,000 units, 80% completed: Direct materials (1,000 x$ 4.1) Conversion (1,000 x 80% x $1.7) $ 4,100 1,360 $ 5,460 From Smeiting Department, 22,000 units $92,400 Direct labor 24,254 Factory overhead 13,060 During September, 1,000 units in process on September 1 were completed, and of the 22,000 units entering the department, all were completed except 2,100 units that were 30% completed. Charges to Work in Process-Rolling for October were as follows: From Smelting Department, 25,300 units $111,320 Direct labor 32,100 Factory overhead 17,281 During October, the units in process at the beginning of the month were completed, and of the 25,300 units entering the department, all were completed except 1,300 units that were 40% completed. Required: 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. Ir an amount box doe not require an entry, leave it blank. 1. Enter the balance as of September 1 in a four-column account for Work in Process-Rolling. Record the debits and the credits in the account for September. Construct a cost of production report and present computations for determining (a) equivalent units of production for materials and conversion, (b) costs per equivalent unit, (c) cost of goods finished, differentiating between units started in the prior period and units started and finished in September, and (d) work in process inventory. If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT No. BALANCE DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT Sept. 1 Bal., 1,000 units, 80% completed Sept. 30 Smelting Dept., 22,000 units at $4.2 Sept. 30 Direct labor Sept. 30 Factory overhead Sept. 30 Finished goods Sept. 30 Bal., 2,100 units, 30% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended September 30 Whole Units Equivalent Units Direct Conversion Units Materials (a) (a) Units charged to production: Inventory in process, September 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, September 1 Started and completed in September Transferred to finished goods in September Inventory in process, September 30 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for September in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, September 1 Costs incurred in September O Total costs accounted for by the Rolling Department Costs allocated to completed and partially completed units: Inventory in process, September 1 balance (c) To complete inventory in process, September 1 (c) Cost of completed September 1 work in process Started and completed in September (c) Transferred to finished goods in September (c) Inventory in process, September 30 (d) Total costs assigned by the Rolling Department 2. Provide the same information for October by recording the October transactions in the four-column work in process account. Construct a cost of production report, and present the October computations (a through d) listed in part (1). If an amount box does not require an entry, leave it blank. ACCOUNT Work in Process-Rolling Department ACCOUNT NO. Balance DATE ITEM POST. REF. DEBIT CREDIT DEBIT CREDIT October 1 Balance October 31 Smelting Dept., 25,300 units at $4.4 October 31 Direct labor October 31 Factory overhead October 31 Finished goods October 31 Bal, 1,300 units, 40% completed If an amount is zero, enter in a zero "0". Round cost per unit answers to the nearest cent. If an amount is zero, enter in a zero "O". Round cost per unit answers to the nearest cent. Pittsburgh Aluminum Company Cost of Production Report-Rolling Department For the Month Ended October 31 Whole Units Equivalent Units Units Direct Conversion Materials (a) (a) Units charged to production: Inventory in process, October 1 Received from Smelting Department Total units accounted for by the Rolling Department Units to be assigned costs: Inventory in process, October 1 Started and completed in October Transferred to finished goods in October Inventory in process, October 31 Total units to be assigned costs Costs Costs Direct Materials Conversion Total Costs Cost per equivalent unit: Total costs for October in Rolling Department Total equivalent units Cost per equivalent unit (b) Costs assigned to production: Inventory in process, October 1 Costs incurred in October Total costs accounted for by the Rolling Department Costs allocated to completed and partially.completed units: Inventory in process, October1 balance (c) To complete inventory in process, October 1 (c) Cost of completed October 1 work in process Started and completed in October (c) Transferred to finished goods in October (c) Inventory in process, October 31 (d) Total costs assigned by the Rolling Department from from August to October. The cost per equivalent unit for conversion costs 3. The cost per equivalent unit for direct materials August to October. These changes be investigated for their underlying causes, and any necessary corrective actions should be taken.

Expert Answer:

Answer rating: 100% (QA)

3 The cost per equivalent unit for direct material in ... View the full answer

Related Book For

Financial and Managerial Accounting

ISBN: 978-1285078571

12th edition

Authors: Carl S. Warren, James M. Reeve, Jonathan Duchac

Posted Date:

Students also viewed these accounting questions

-

Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting...

-

Pittsburgh Aluminum Company uses a process cost system to record the costs of manufacturing rolled aluminum, which consists of the smelting and rolling processes. Materials are entered from smelting...

-

Baker's Chocolate common stock had annual returns of 13.7%, 11.3%, 4.6%, and - 8.9% over the last four years, respectively. What is the standard deviation of these returns? Select one: a. 11.8% b....

-

The manager of a $20 million portfolio of domestic stocks with a beta of 1.10 would like to begin diversifying internationally. He would like to sell $5 million of domestic stock and purchase $5...

-

Tais sales last week were $140 less than three times Veras sales. What were Tais sales if together their sales amounted to $940? For this problem, set up an equation in one unknown and solve.

-

As vice president for community relations, you want to explore the possibility of developing service learning programs with several nearby colleges and universities. Using Figure 2.5, suggest the...

-

The simplified financial statements of SPS Ltd appear below. Additional information 1. Dividends declared and paid were \($26\) 400. 2. During the year equipment was sold for \($10\) 200 cash. The...

-

On January 1, 2014, Vermont Maple Corp. had 2,650,000 shares of common stock issued and outstanding. During 2014, it had the following transactions that affected the common stock account. Mar. 1...

-

6. Explain in detail why 8086 supports a maximum of 1MB physical memory? (2 mark) 7. What will be the capacity in megabytes of the physical memory of a microprocessor with a 28 bit address bus? What...

-

The income statement for Weatherford International Inc.?s year ended December 31, 2020, was prepared by an inexperienced bookkeeper. As the new accountant, your immediate priority is to correct the...

-

Discuss the performance of the stocks, how the company's performance impacts the stock performance, and their investment potential. Include at least one paragraph for each company. You can consult...

-

Let \((B, W)\) be a two-dimensional Brownian motion and define \[T_{t}=\inf \left\{s \geq 0: W_{s}>t ight\}\] Prove that \(\left(Y_{t}=B_{T_{t}}, t \geq 0 ight)\) is a Cauchy process, i.e., a process...

-

A hospitals UM committee discovers that the rate of cesarean section births at the hospital is higher than the rate at other hospitals in the region, where more women have vaginal deliveries. The UM...

-

Many people who do not smoke cigars are bothered by the odor of cigar smoke. If private contracting is impossible, will too many or too few cigars be produced and consumed? Taking all costs into...

-

U.S. Aviation Underwriters issued an aircraft insurance policy to Cash Air, Inc., covering its employees. The policy stated that to be covered under the policy, the aircraft must be flown only by a...

-

Susan Colantuono: The Career Advice You Probably Didnt Get13:57 minutes https://www.youtube.com/watch?v=JFQLvbVJVMg How do the skills Colantuono talks about matter to measuring and implementing...

-

a survey reported that 72 of people or 24% of the group were smokers. how many people were surveyed

-

Solve each equation or inequality. |6x8-4 = 0

-

What types of accounts are referred to as temporary accounts?

-

What do the following data taken from a comparative balance sheet indicate about the companys ability to borrow additional funds on a long-term basis in the current year as compared to the...

-

Im Really Cold Coat Company makes womens and mens coats. Both products require filler and lining material. The following planning information has been made available: Im Really Cold Coat Company does...

-

Explain the building blocks of accounting: ethics, principles, and assumptions.

-

On May 1, 2025, Park Flying School Ltd., a company that provides flying lessons, was started with an investment of 45,000 cash in the business. Following are the assets and liabilities of the company...

-

The historical cost basis results in: a. initially recording assets at cost and adjusting when the current value changes. b. keeping activities of an entity separate and distinct from its owner. c....

Study smarter with the SolutionInn App