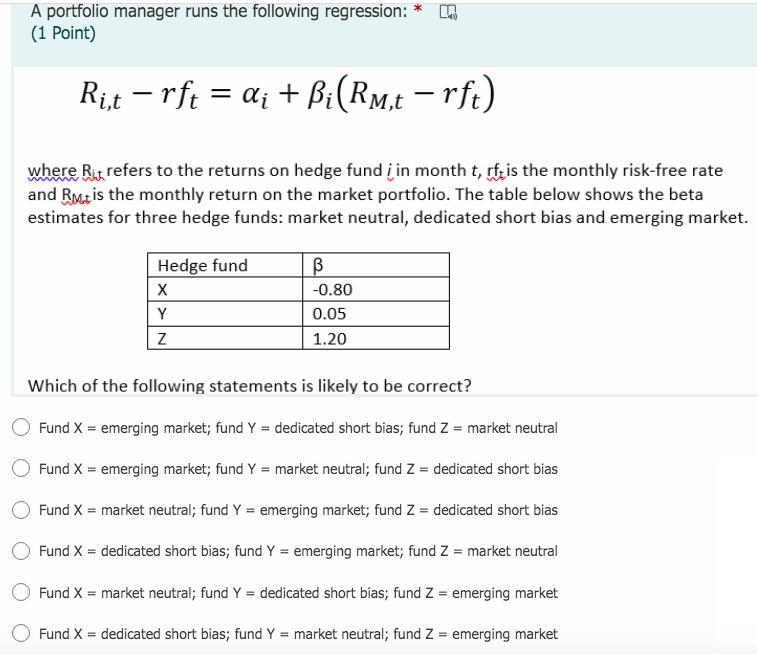

A portfolio manager runs the following regression: (1 Point) Ri,t = rft = i + Bi(Rm,t...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Answer If beta is positive but very low the hedge fund is known as market neutral fu... View the full answer

Related Book For

Posted Date: