Question: Address all the questions please. Thanks A random variable follows a Pareto distribution with density function: 5 x>0 For a given estimate d of

Address all the questions please. Thanks

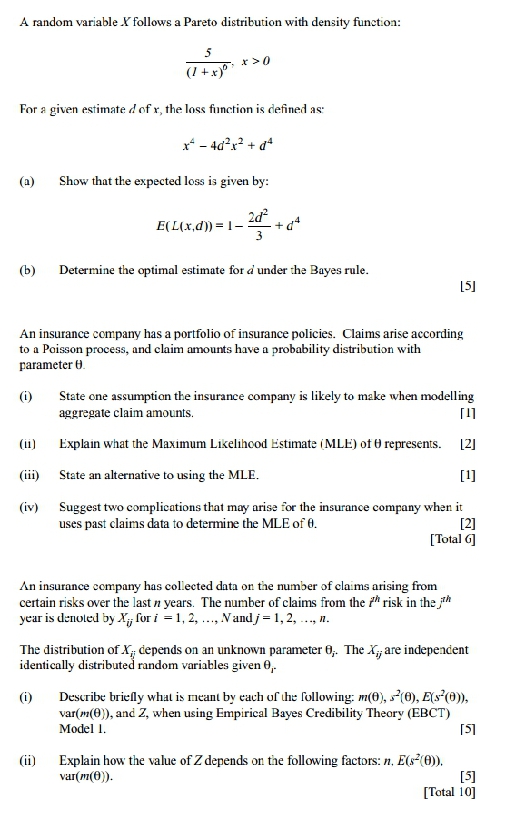

A random variable \\ follows a Pareto distribution with density function: 5 x>0 For a given estimate d of r, the loss function is defined as x* - 403x2+ 14 (@) Show that the expected loss is given by: E(L(x, d)) = 1- 2d- 3 + (b) Determine the optimal estimate for a under the Bayes rule. 15] An insurance company has a portfolio of insurance policies. Claims arise according to a Poisson process, and claim amounts have a probability distribution with parameter U. State one assumption the insurance company is likely to make when modelling aggregate claim amounts. (li) Explain what the Maximum Likelihood Estimate (MLE) of 0 represents. (iii) State an alternative to using the MLE. [1] (iv) Suggest two complications that may arise for the insurance company when it uses past claims data to determine the MLE of 0. [2] [Total 6] An insurance company has collected data on the number of claims arising from certain risks over the last n years. The number of claims from the ?" risk in the jrh year is denoted by X, for i = 1, 2, ..., Nand/ = 1, 2, ..., n. The distribution of X,; depends on an unknown parameter 0;. The X,, are independent identically distributed random variables given 0,- (i) Describe briefly what is meant by each of the following: moo), (0), Es'(@)), var(m(0)), and Z, when using Empirical Bayes Credibility Theory (EBCT) Model 1. 157 (ii) Explain how the value of Z depends on the following factors: n. E(-(0)). var (m(O)). [5] [Total 10]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts