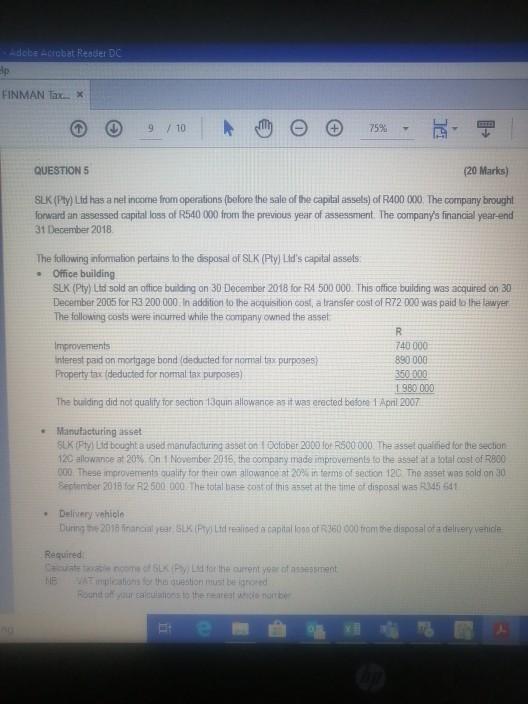

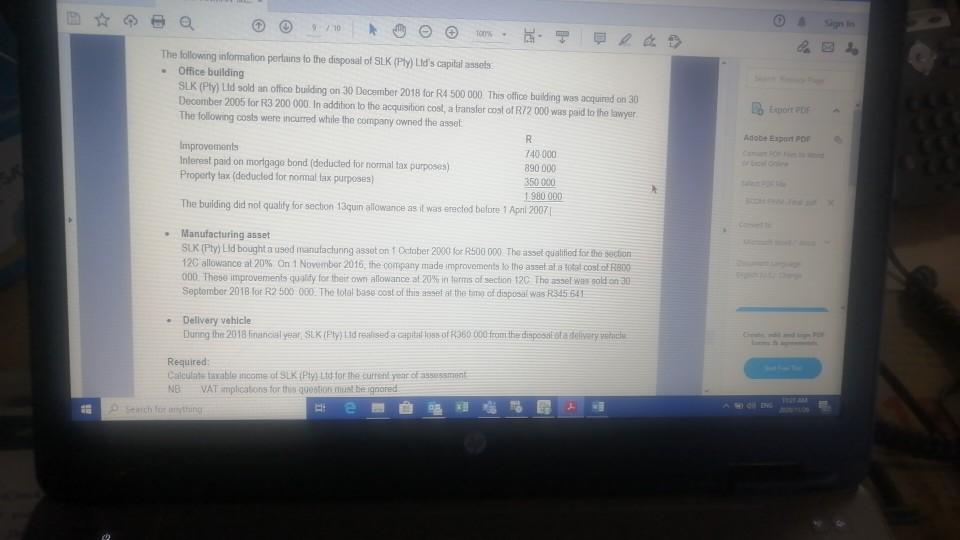

Question: Adobe Acrobat Reader DC ap FINMAN Tax 9 / 10 75% QUESTIONS (20 Marks) SLK (Pty) Ltd has a nel income from operations before the

Adobe Acrobat Reader DC ap FINMAN Tax 9 / 10 75% QUESTIONS (20 Marks) SLK (Pty) Ltd has a nel income from operations before the sale of the capital assets) of R400 000. The company brought forward an assessed capital loss of R540 000 from the previous year of assessment. The company's financial year-end 31 December 2018 . The following information pertains to the disposal of SLK (PtyLid's capital assets Office building SLK (Pty) Ltd sold an office building on 30 December 2018 for R4 500 000 This office building was acquired on 30 December 2005 for R3 200.000. In addition to the acquisition cosi, a transfer cost of R72 200 was paid be the lawyer The following costs were incurred while the company owned the asset Improvements 740 000 interest paid on mortgage bond deducted for normal tax purposes 890 000 Property tax deducted for moral tax purposes) 350 000 1980 000 The buiding did not quality for section 13quin allowance as it was erected before 1 April 2007 R Manufacturing asset SUK (FtyLtd bought a used manufacturing asset on l Odlobet 2000 lo R500 000. The asset qualified for the section 120 allowance at 20%. On 1 November 2016, the company made improvements to the sot at a total cost of R800 000 These marovement quality for their own allowance at 20% in terms of section 120 The asset was sold on 30 September 2018 fox R2 500.000 The total base cost of this act at the time of disposal was R35541 Delivery vehicle During 2018 financiare Sky Lorealed capitalfoon of R350 000 from the disposal of a delivery vehicle Required ne Pforthe current year of sement NIE 910 To The following information pertains to the disposal of SLK (Ply Lid's capital assets Office building SLK (Pty) Lld sold an office building on 30 December 2018 for R4 500 000 This office building was acquired on 30 December 2005 for R3 200 000. In addition to the acquisition cost, a transfer cost of R12 000 was paid to the lawyer. The following costs were incurred while the company cwned the asset R Improvements 740.000 Interest paid on mortgage bond (deducted for normal tax purposes) 890 000 Property tax (deducted for nomal tax purposes) 350 000 1 980 000 The building did not quality for section 13quin allowance as it was erected before 1 April 2007 Adobe part of Manufacturing asset SLK (Pty) Lid bought a used manufacturing asset on October 2000 for R500 000. The asset qualified for the section 120 allowance at 20% On 1 November 2016, the company made improvements to the assalala fatal cost of R800 000. These improvements quality for their own pillowance at 20% in terms of section 12C The asset was gold on 30 September 2018 for R2508).000. The total sase cost of this set at the time of disposal was R315 541 Delivery vehicle During the 2018 financial Meal SLK (Pty) Ltd retilised a capital 1913 of 350 000 from the disposal at a lativery welche Required Calculate taxable income of SLK (Pty) Ltd for the cuttenyeron VAT implications for this question must be ignored NE Adobe Acrobat Reader DC ap FINMAN Tax 9 / 10 75% QUESTIONS (20 Marks) SLK (Pty) Ltd has a nel income from operations before the sale of the capital assets) of R400 000. The company brought forward an assessed capital loss of R540 000 from the previous year of assessment. The company's financial year-end 31 December 2018 . The following information pertains to the disposal of SLK (PtyLid's capital assets Office building SLK (Pty) Ltd sold an office building on 30 December 2018 for R4 500 000 This office building was acquired on 30 December 2005 for R3 200.000. In addition to the acquisition cosi, a transfer cost of R72 200 was paid be the lawyer The following costs were incurred while the company owned the asset Improvements 740 000 interest paid on mortgage bond deducted for normal tax purposes 890 000 Property tax deducted for moral tax purposes) 350 000 1980 000 The buiding did not quality for section 13quin allowance as it was erected before 1 April 2007 R Manufacturing asset SUK (FtyLtd bought a used manufacturing asset on l Odlobet 2000 lo R500 000. The asset qualified for the section 120 allowance at 20%. On 1 November 2016, the company made improvements to the sot at a total cost of R800 000 These marovement quality for their own allowance at 20% in terms of section 120 The asset was sold on 30 September 2018 fox R2 500.000 The total base cost of this act at the time of disposal was R35541 Delivery vehicle During 2018 financiare Sky Lorealed capitalfoon of R350 000 from the disposal of a delivery vehicle Required ne Pforthe current year of sement NIE 910 To The following information pertains to the disposal of SLK (Ply Lid's capital assets Office building SLK (Pty) Lld sold an office building on 30 December 2018 for R4 500 000 This office building was acquired on 30 December 2005 for R3 200 000. In addition to the acquisition cost, a transfer cost of R12 000 was paid to the lawyer. The following costs were incurred while the company cwned the asset R Improvements 740.000 Interest paid on mortgage bond (deducted for normal tax purposes) 890 000 Property tax (deducted for nomal tax purposes) 350 000 1 980 000 The building did not quality for section 13quin allowance as it was erected before 1 April 2007 Adobe part of Manufacturing asset SLK (Pty) Lid bought a used manufacturing asset on October 2000 for R500 000. The asset qualified for the section 120 allowance at 20% On 1 November 2016, the company made improvements to the assalala fatal cost of R800 000. These improvements quality for their own pillowance at 20% in terms of section 12C The asset was gold on 30 September 2018 for R2508).000. The total sase cost of this set at the time of disposal was R315 541 Delivery vehicle During the 2018 financial Meal SLK (Pty) Ltd retilised a capital 1913 of 350 000 from the disposal at a lativery welche Required Calculate taxable income of SLK (Pty) Ltd for the cuttenyeron VAT implications for this question must be ignored NE

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts